Answered step by step

Verified Expert Solution

Question

1 Approved Answer

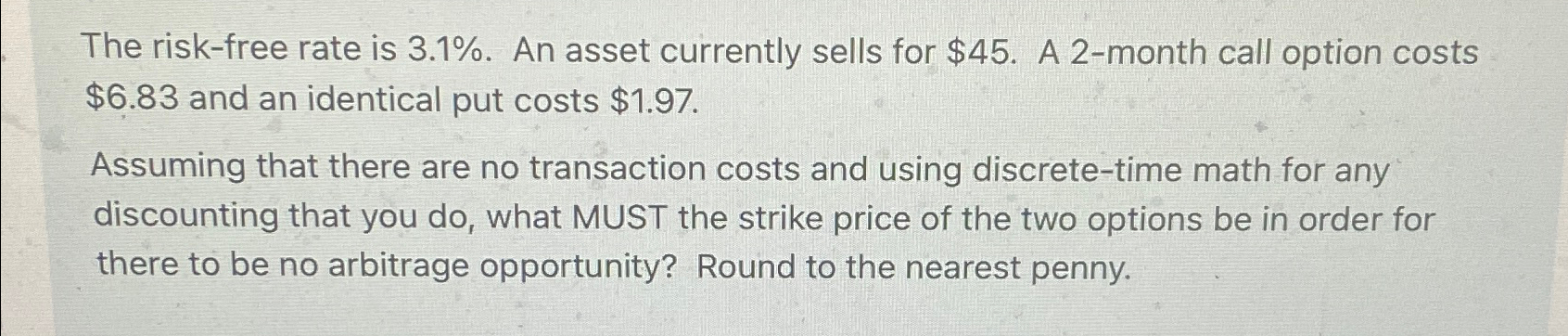

The risk - free rate is 3 . 1 % . An asset currently sells for $ 4 5 . A 2 - month call

The riskfree rate is An asset currently sells for $ A month call option costs $ and an identical put costs $

Assuming that there are no transaction costs and using discretetime math for any discounting that you do what MUST the strike price of the two options be in order for there to be no arbitrage opportunity? Round to the nearest penny.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational Financial Management

Authors: Alan C. Shapiro

7th Edition

0471395307, 9780471395300