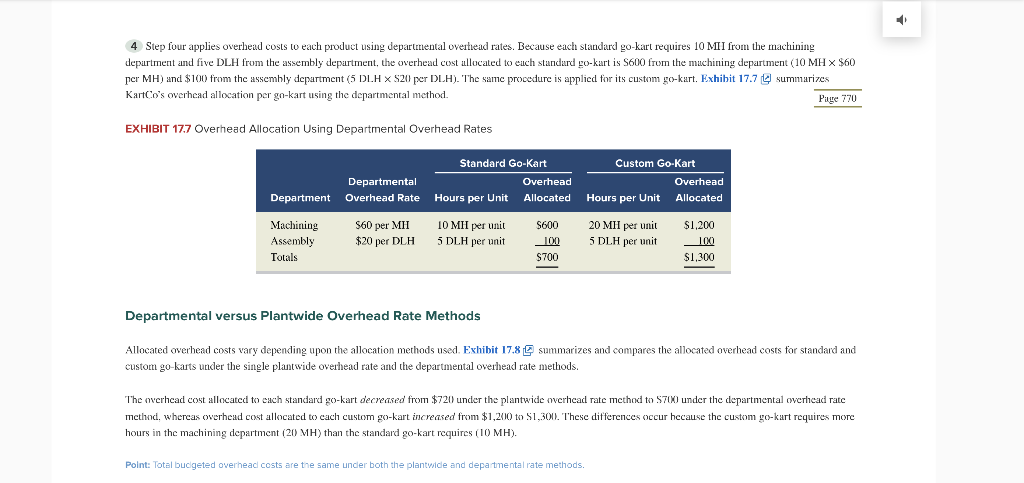

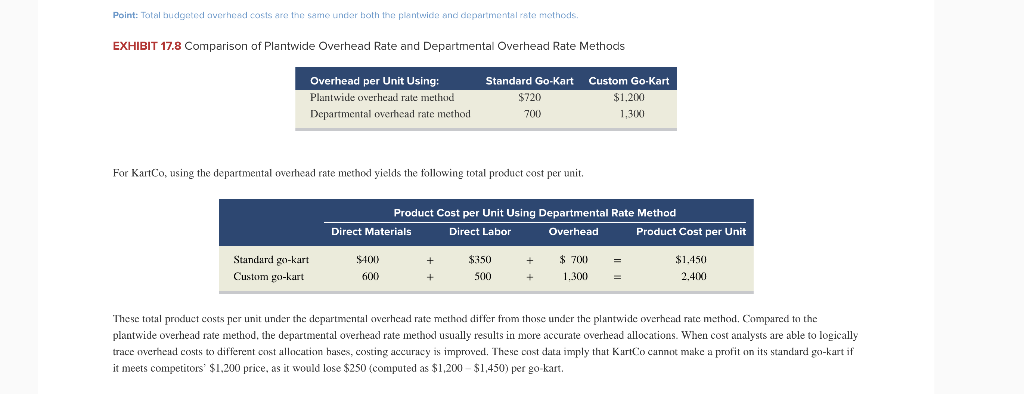

The spreadsheet assignment. Prepare a spreadsheet (Google Sheets or Excel) that calculates and presents the answer to the Exercise 17-7 and 17-8. The spreadsheet needs to have the correct numbers (10 points), Formulas (20 points) and formatting (20 points), to look presentable in a business context. Each student must submit a speadsheet via Canvas. 4 Step four applies overhead costs to each product using departmental overtiead rates. Because each standard go-kart requires 10 MII from the machining department and five DLH from the assembly department, the overhead cost allocated to each standard go-kart is S600 from the machining department (10 MH X $60 per MH) and $100 from the assembly department (5 DLH X 5201 per DLH). The same procedure is applied for its custom go-kart. Exhibit 17.7 summarizes KartCo's overhead allocation per go-kart using the departmental method Page 770 EXHIBIT 17.7 Overhead Allocation Using Departmental Overhead Rates Departmental Department Overhead Rate Standard Go-Kart Overhead Hours per Unit Allocated Custom Go-Kart Overhead Hours per Unit Allocated Machining Assembly Totals S60 per MH $20 per DLH 10 MII per unit 5 DLH per unit $600 100 $700 20 MII per unit 5 DLH per unit $1,200 100 $1,300 Departmental versus Plantwide Overhead Rate Methods Allocated overhead costs vary depending upon the allocation methods used. Exhibit 17.8 summarizes and compares the allocated overhead costs for standard and custom go-karts under the single plantvide overhead rate and the departmental overhead rate methods. The overhcad cost allocated to each standard go-kart decreased from $721) under the plantwide overhead rate method to 5700) under the departmental overhead rate mcthund, whereas overhead cost allocated to cach custom go-kart increased from $1,2010 to $1,300. These differences occur hecause the custom go-kart requires more hours in the machining department (20) MH) than the standard go-kart requires (10 MH). Point: Total budgeted overhead costs are the same under both the plantwide and departmental rate methods. Point: Total budgeted overhead costs are the same under both the plantwide and departmental rete methods EXHIBIT 17.8 Comparison of Plantwide Overhead Rate and Departmental Overhead Rate Methods Overhead per Unit Using: Plantwide overhead rate method Departmental overhead rate method Standard Go-Kart $720 700 Custom Go-Kart $1.200 1,300 For KartCo, using the departmental overhead rate method yields the following total product cost per unit Product Cost per Unit Using Departmental Rate Method Direct Materials Direct Labor Overhead Product Cost per Unit $100 $350 - = $1.450 Standard go-kart Custom go-kart $ 700 1.300 600 500 + 2.400 These total product costs per unit under the departmental overhead rate method differ from those under the plantwide overhead rate method. Compared to the plantwide overhead rate method, the departmental overhead rate method usually results in more accurate overhead allocations. When cost analysts are able to logically trace overhead costs to different onst allocation bases, costing accuracy is improved. These cost data imply that KartCo cannot make a profit on its standard go-kart if it meets competitors $1,200 price, as it would lose $250 (computed as $1,200 $1,450) per go kart. The spreadsheet assignment. Prepare a spreadsheet (Google Sheets or Excel) that calculates and presents the answer to the Exercise 17-7 and 17-8. The spreadsheet needs to have the correct numbers (10 points), Formulas (20 points) and formatting (20 points), to look presentable in a business context. Each student must submit a speadsheet via Canvas. 4 Step four applies overhead costs to each product using departmental overtiead rates. Because each standard go-kart requires 10 MII from the machining department and five DLH from the assembly department, the overhead cost allocated to each standard go-kart is S600 from the machining department (10 MH X $60 per MH) and $100 from the assembly department (5 DLH X 5201 per DLH). The same procedure is applied for its custom go-kart. Exhibit 17.7 summarizes KartCo's overhead allocation per go-kart using the departmental method Page 770 EXHIBIT 17.7 Overhead Allocation Using Departmental Overhead Rates Departmental Department Overhead Rate Standard Go-Kart Overhead Hours per Unit Allocated Custom Go-Kart Overhead Hours per Unit Allocated Machining Assembly Totals S60 per MH $20 per DLH 10 MII per unit 5 DLH per unit $600 100 $700 20 MII per unit 5 DLH per unit $1,200 100 $1,300 Departmental versus Plantwide Overhead Rate Methods Allocated overhead costs vary depending upon the allocation methods used. Exhibit 17.8 summarizes and compares the allocated overhead costs for standard and custom go-karts under the single plantvide overhead rate and the departmental overhead rate methods. The overhcad cost allocated to each standard go-kart decreased from $721) under the plantwide overhead rate method to 5700) under the departmental overhead rate mcthund, whereas overhead cost allocated to cach custom go-kart increased from $1,2010 to $1,300. These differences occur hecause the custom go-kart requires more hours in the machining department (20) MH) than the standard go-kart requires (10 MH). Point: Total budgeted overhead costs are the same under both the plantwide and departmental rate methods. Point: Total budgeted overhead costs are the same under both the plantwide and departmental rete methods EXHIBIT 17.8 Comparison of Plantwide Overhead Rate and Departmental Overhead Rate Methods Overhead per Unit Using: Plantwide overhead rate method Departmental overhead rate method Standard Go-Kart $720 700 Custom Go-Kart $1.200 1,300 For KartCo, using the departmental overhead rate method yields the following total product cost per unit Product Cost per Unit Using Departmental Rate Method Direct Materials Direct Labor Overhead Product Cost per Unit $100 $350 - = $1.450 Standard go-kart Custom go-kart $ 700 1.300 600 500 + 2.400 These total product costs per unit under the departmental overhead rate method differ from those under the plantwide overhead rate method. Compared to the plantwide overhead rate method, the departmental overhead rate method usually results in more accurate overhead allocations. When cost analysts are able to logically trace overhead costs to different onst allocation bases, costing accuracy is improved. These cost data imply that KartCo cannot make a profit on its standard go-kart if it meets competitors $1,200 price, as it would lose $250 (computed as $1,200 $1,450) per go kart