Answered step by step

Verified Expert Solution

Question

1 Approved Answer

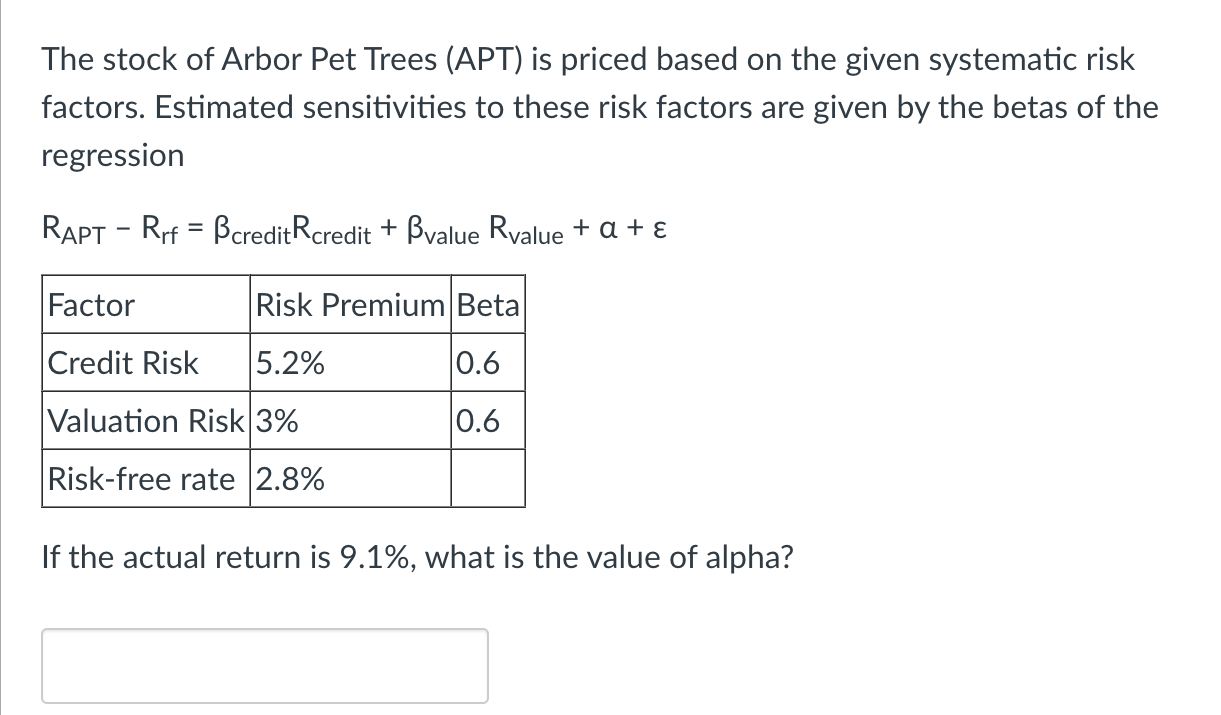

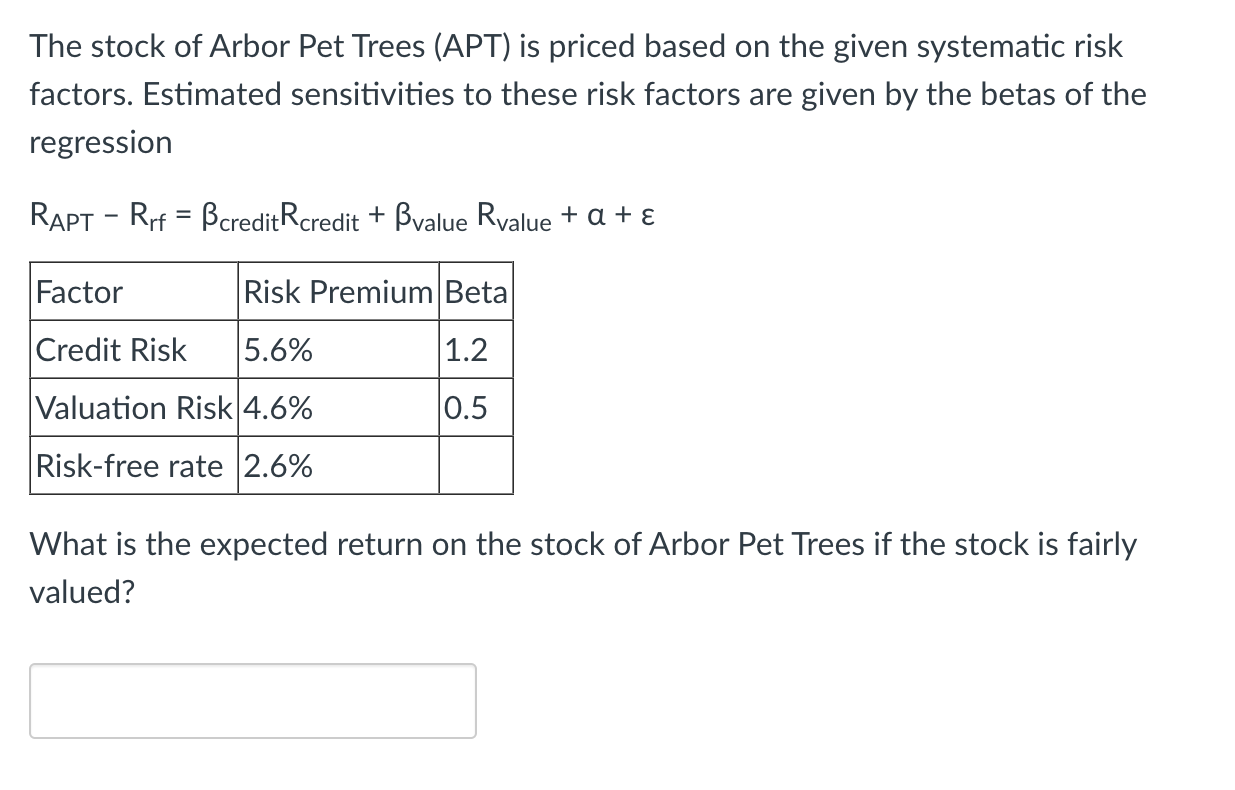

The stock of Arbor Pet Trees (APT) is priced based on the given systematic risk factors. Estimated sensitivities to these risk factors are given by

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Nft Guide Learn How To Buy Sell Collect And Mint Non Fungible Tokens

Authors: Thomas Jase

1st Edition