Question

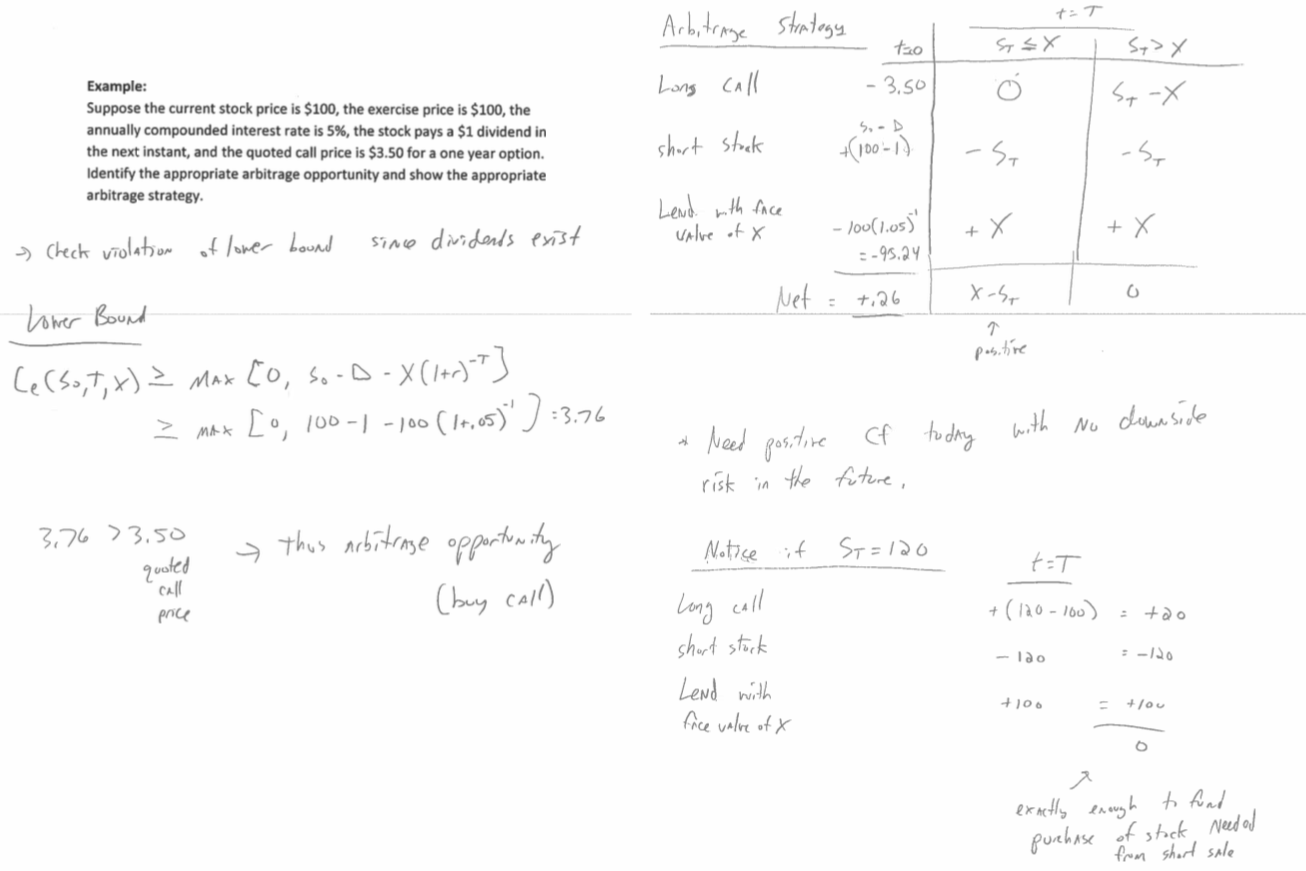

The stock price is $100. There are two European options that expire in 1 year with an exercise price of $110. The call option premium

- The stock price is $100. There are two European options that expire in 1 year with an exercise price of $110. The call option premium is $3 and the put option premium is $12.5. The risk free rate is 6% compounded annually. Is Put-Call Parity violated? If so, you must show the appropriate strategy to capture that profit. You must show a full arbitrage table with payoffs today and in the future. Round to 4 decimal

SHOW YOUR WORK TO GET CREDIT FOR ANY CALCULATIONS

I want an answer for number 1. I have added picture of the example problem below in a way I want my answer to be using those formulas from the picture.

Because that's how the professor wants his answers to be and make sure to add a table looking like from the example problem.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Handbook Of Sovereign Wealth Funds

Authors: Douglas J. Cumming, Geoffrey Wood, Igor Filatotchev, Juliane Reinecke

1st Edition

0198754809, 978-0198754800