Answered step by step

Verified Expert Solution

Question

1 Approved Answer

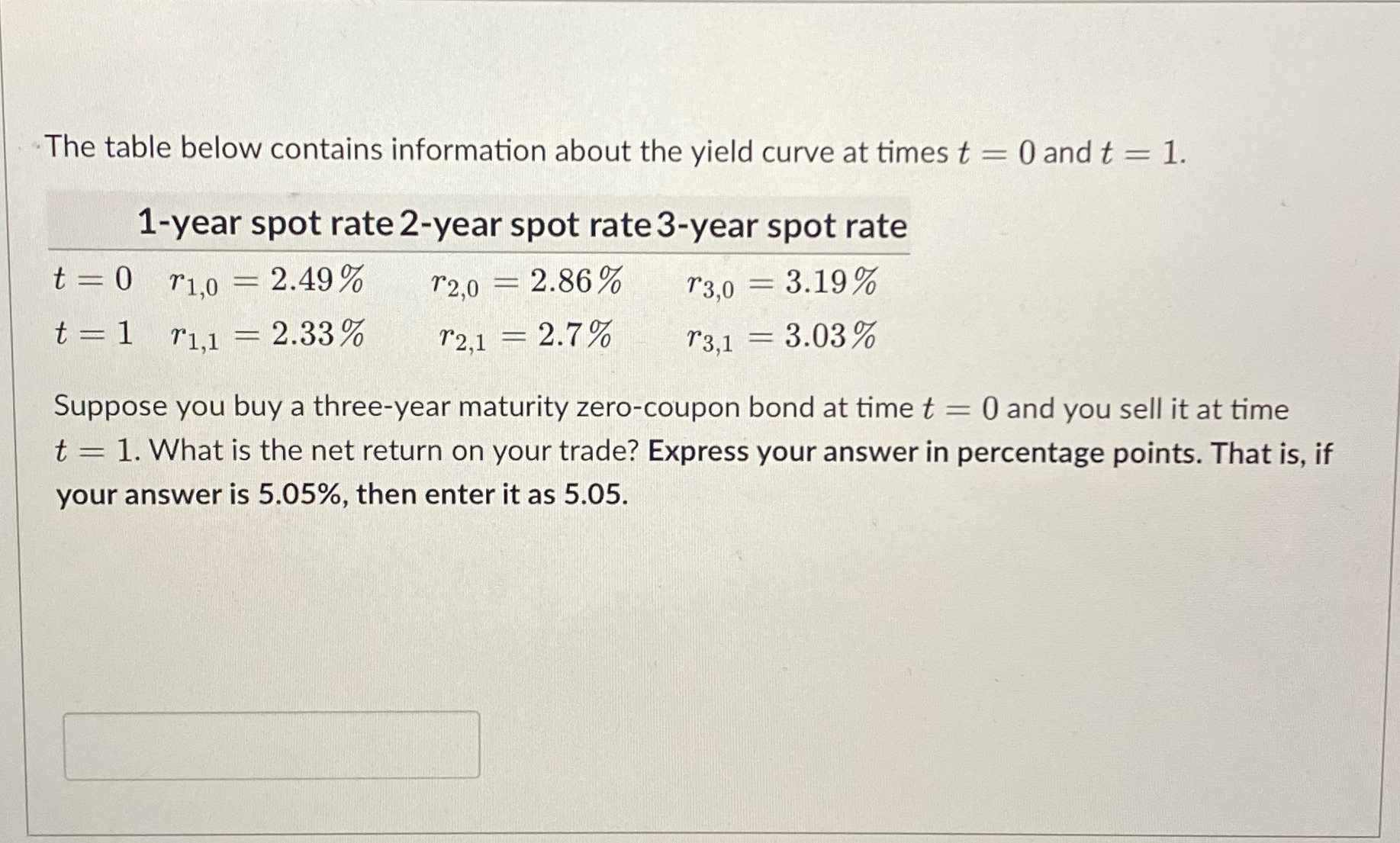

The table below contains information about the yield curve at times t = 0 and t = 1. 1-year spot rate 2-year spot rate

The table below contains information about the yield curve at times t = 0 and t = 1. 1-year spot rate 2-year spot rate 3-year spot rate t=0 r1,0 r1,0 = 2.49% T2,0 = 2.86% - r3,0 = 3.19% t=1 r1,1 = 2.33% 12,1 = 2.7% T3,1 = 3.03% Suppose you buy a three-year maturity zero-coupon bond at time t = 0 and you sell it at time t = 1. What is the net return on your trade? Express your answer in percentage points. That is, if your answer is 5.05%, then enter it as 5.05.

Step by Step Solution

★★★★★

3.49 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

calculate the net return on your trade Price Paid at t0 Purchase Price Since the bond is a zerocoupo...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics Data Analysis And Decision Modeling

Authors: James R. Evans

5th Edition

132744287, 978-0132744287