Answered step by step

Verified Expert Solution

Question

1 Approved Answer

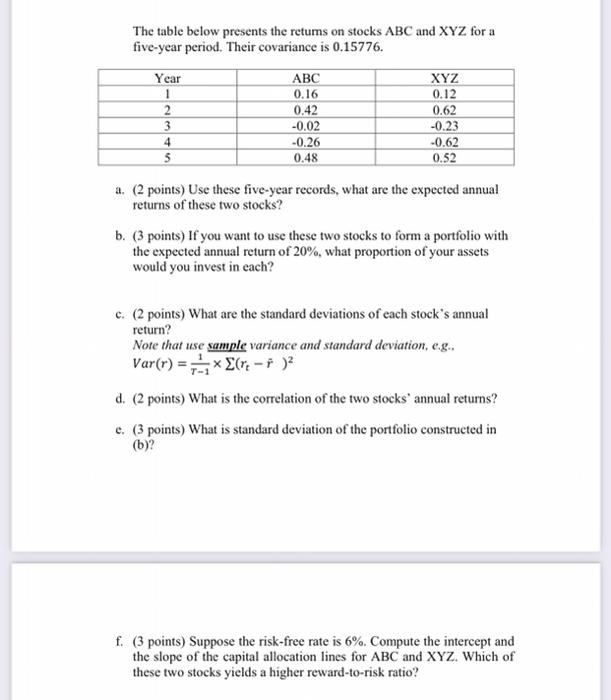

The table below presents the retums on stocks ABC and XYZ for a five-year period. Their covariance is 0.15776. Year 1 2 3 4 5

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Citizens Guide To P3 Projects A Legal Primer For Public Private Partnerships

Authors: Ernest C. Brown , Esq. PE

1st Edition

1532089996,1532090013