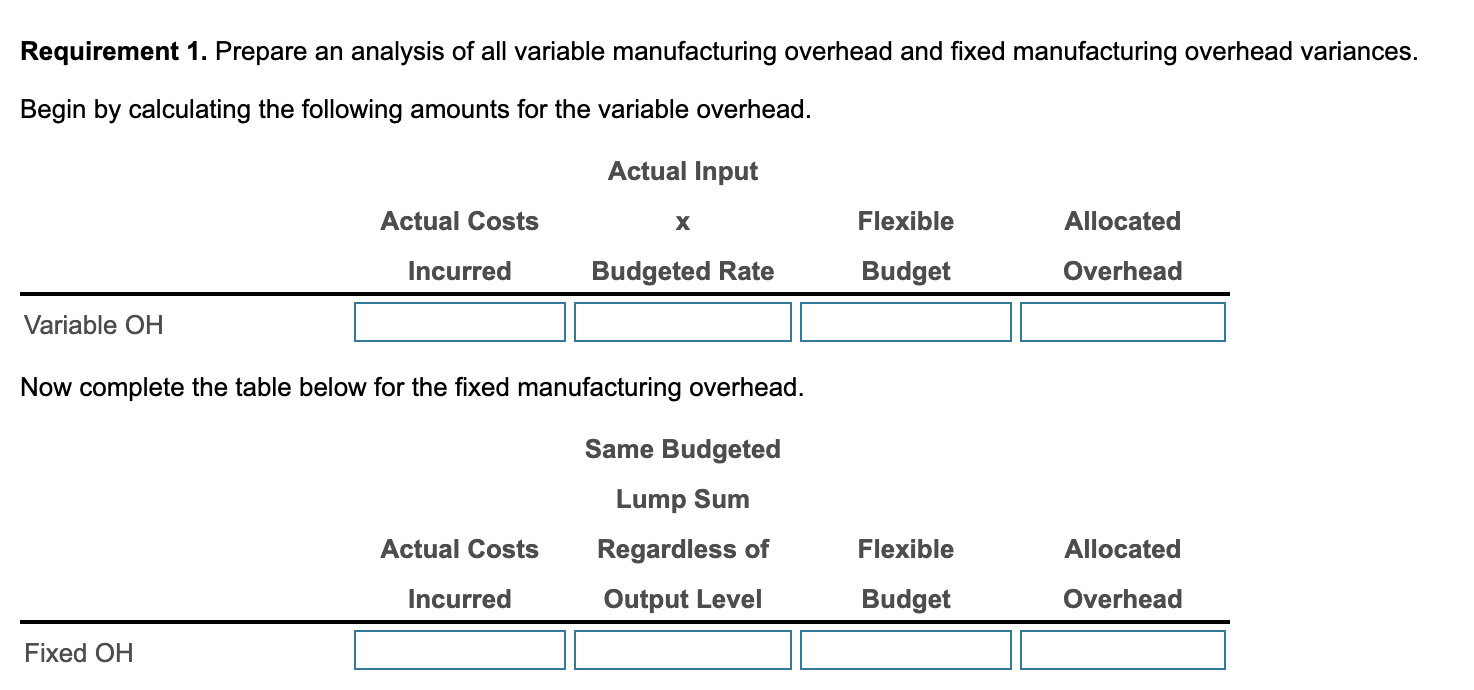

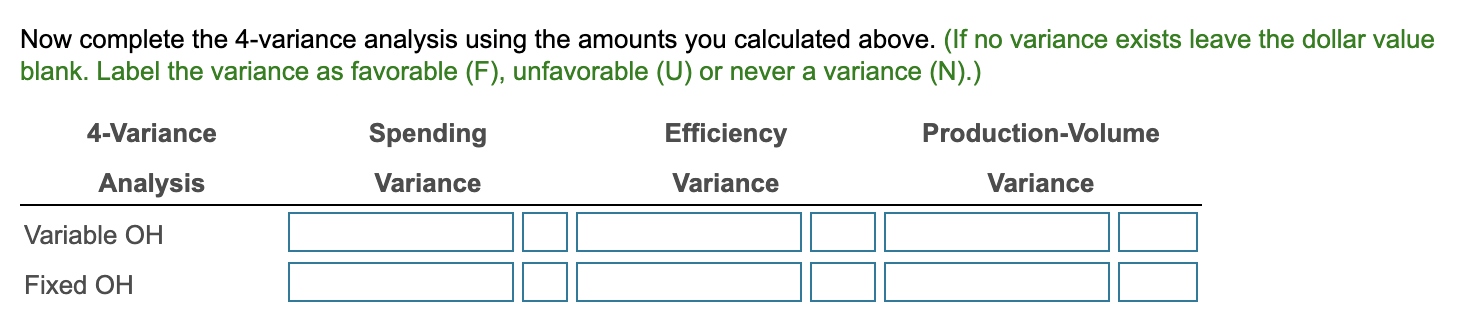

Question

The Tolerances Corporation is a manufacturer of centrifuges. Fixed and variable manufacturing overheads are allocated to each centrifuge using budgeted assembly-hours. Budgeted assembly time is

The Tolerances Corporation is a manufacturer of centrifuges. Fixed and variable manufacturing overheads are allocated to each centrifuge using budgeted assembly-hours. Budgeted assembly time is 2 hours per unit. The following table shows the budgeted amounts and actual results related to overhead for June 2017.

Data Table

| Actual | Static | |

| The Tolerances Corporation (June 2017) | Results | Budget |

| Number of centrifuges assembled and sold | 240 | 130 |

| Hours of assembly time | 264 |

|

| Variable manufacturing overhead cost per hour of assembly time |

| $32.00 |

| Variable manufacturing overhead costs | $8,864 |

|

| Fixed manufacturing overhead costs | $13,860 | $12,480 |

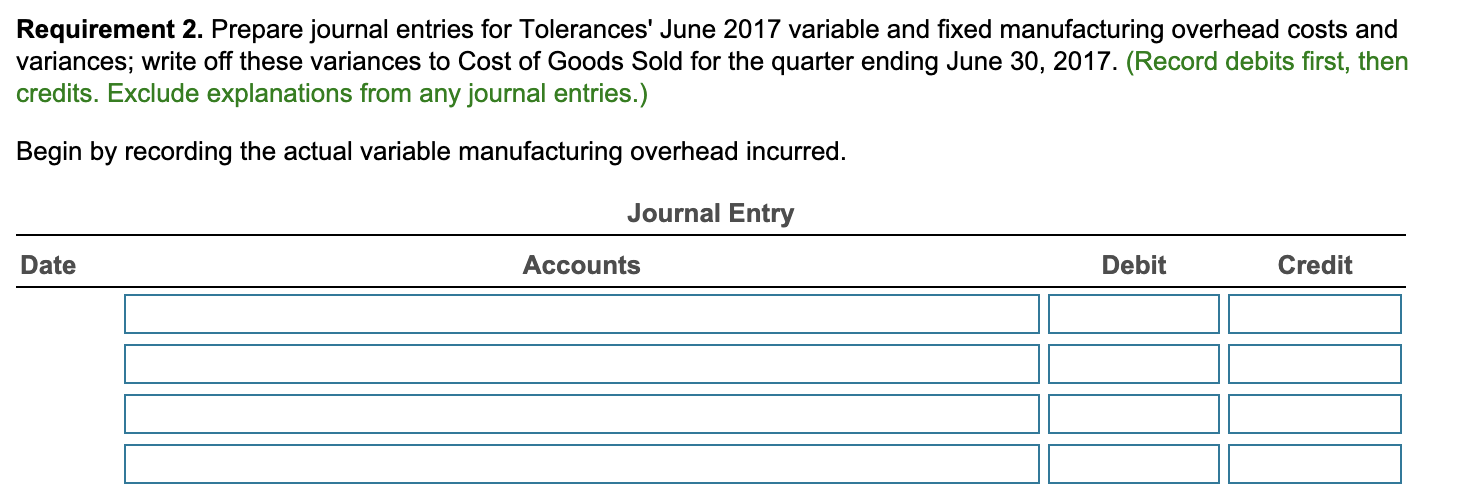

1.Prepare an analysis of all variable manufacturing overhead and fixed manufacturing overhead variances. 2.Prepare journal entries for Tolerances' June 2017 variable and fixed manufacturing overhead costs and variances; write off these variances to Cost of Goods Sold for the quarter ending June 30, 2017. 3.How does the planning and control of variable manufacturing overhead costs differ from the planning and control of fixed manufacturing overhead costs?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing The Risk Management Process

Authors: K. H. Spencer Pickett

1st Edition

0471690538, 978-0471690535