Question

The topic is continuous, it is difficult to ask questions separately, you can take it as I asked 9 questions, the first two questions I

The topic is continuous, it is difficult to ask questions separately, you can take it as I asked 9 questions, the first two questions I finished, the back will not do, I put my answer also po up

Corporate Finance

Assignment Aims

The assignment aims to enable you to apply some of what you will learn from Topics 1 & 2 - in particular, return and risk, and the future value of a lump sum investment. However, the assignment also aims to get you to think ahead about some of the things that you will learn from Topics 5 & 6 - in particular, portfolio investment.

Assignment Setup

Imagine that you are back at the end of the fourth quarter of 1999 (Q4 1999). You are 45 years of age and have a good job but no children to think about. You have just been gifted 10,000 and will invest all of the money for the next 20 years. You have the following five portfolios in mind:

UK large market capitalisation stocks (from various industries);

UK small market capitalisation stocks (from various industries);

UK 3 months Government bills;

UK 10+ years Government bonds; and

UK 10+ years investment grade corporate bonds (from various industries).

You can only invest in one of the five portfolios, and once invested the money will need to remain in your chosen portfolio for the next 20 years. In other words, you cannot spread the 10,000 across multiple portfolios, nor move between portfolios during the investment period.

Assignment Tasks

1. without the need any computations, rank the five portfolios from likely greatest to likely least risk. Explain your reasoning behind this ranking.

UK small market capitalisation stocks(from various industries)UK large market capitalisation stocks(from various industries)UK 10+ years investment grade corporate bonds (from various industries)UK 10+ years Government bondsUK 3 months Government bills

Equity claims on limited liability firms represent the share or stock value of a stake in a firm. Value is returned to the investor by the payment of dividends and by capital appreciation driven by future dividends, both of which are uncertain, therefore equity returns are risky. Compared with large companies, small companies have a smaller capital volume, so they have weaker risk tolerance but stronger growth and therefore higher risks.

Bonds/long-term fixed rate investment accounts are all long lived investments which despite having a known long-term rate of interest, can fluctuate in value due to shorter term changes in interest rates. With regards to corporate bonds, government bonds are backed by the government's credibility which means expected repayment is more reliable and punctual so it is less risky.

Short-term bills whose rate of return is known at the beginning of the investment, as long as the issuer does not default, the rates of return can be perceived as risk free for the period of investment. Thus, UK3 months Government bills involve the least risk.

2. Which of the five portfolios will you choose to invest in? Explain your reasoning for selecting this portfolio.

I would choose the UK small market capitalisation stocks to invest.

UK smaller company stocks have returned six times the amount of large companies and yet may still be good value for investors.

Because of their size, "small caps" have the potential to grow more quickly.The quicker a company can grow its earnings in a sustainable way the more attractive it is to investors.

Once a small cap company starts to deliver you could potentially get a double whammy effect of growth and rerating. A small cap stock might go from a P/E of 10 to 20 times once it starts to grow and get discovered.That is much more difficult to achieve with larger companies.

I am 45 years old and have a good job but no children, which means I have a sustainable income but no household expenditures and considerations. Since the 10,000 came at no cost, I would take it to bet a higher return in the next 20 years.

The accompanying Excel file under Assignments on the module's Canvas site contains three sheets of data.

The first sheet (Large stocks) contains information and quarterly data for the UK large market capitalisation stocks. The portfolio constituents are listed first, together with each stock's industry. Return index data for each stock (which accounts for the reinvestment of all dividends) is then provided for Q4 1999-Q2 2020, followed by market capitalisation data for each stock (in million) for the same period.

The second sheet (Small stocks) contains information and quarterly data for the UK small market capitalisation stocks. The portfolio constituents are listed first, together with each stock's industry. Return index data for each stock (which accounts for the reinvestment of all dividends) is then provided for Q4 1999-Q2 2020, followed by market capitalisation data for each stock (in million) for the same period.

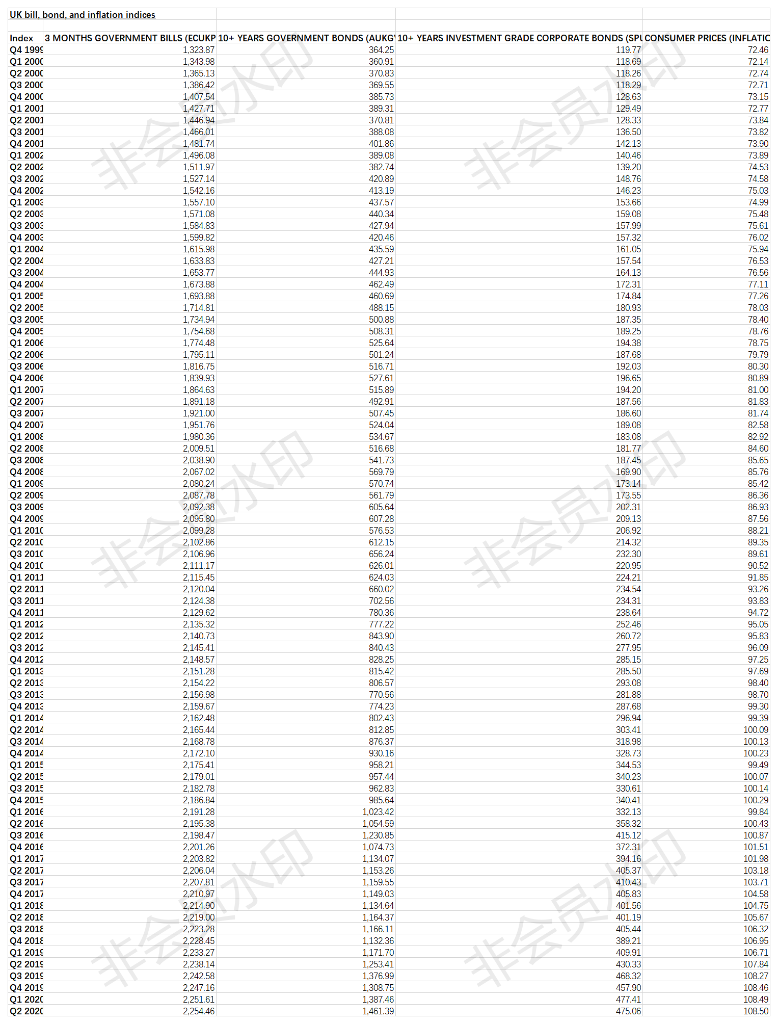

The third sheet (Bills, bonds, and inflation) contains quarterly data for the UK 3 months Government bills, 10+ years Government bonds, and UK 10+ years investment grade corporate bonds. Return index data for each portfolio (which accounts for the reinvestment of all interest) is provided for Q4 1999-Q2 2020. This sheet also contains quarterly data for the UK consumer price (inflation) index for the same period.

Note: While the bills and the bonds are provided in portfolio (combined) form this is not the case for the large stocks and the small stocks. It will therefore be necessary for you to do what is required below by constructing the portfolio containing all of the large stocks and the portfolio containing all of the small stocks. Both of these portfolios should be market capitalization weighted. Also, the data that you are provided with for each of the five portfolios is in quarterly return index form and not therefore in quarterly return form.

Required:

3. You invest the gift money at the end of Q4 1999. Based on the portfolio that you have chosen in part 2, what is the future value of your 10,000 lump sum investment by the end of Q2 2020? (Show all of your workings.)

4. Were you to have instead chosen to invest in one of the other (four) portfolios, what would the future value of your 10,000 lump sum investment have been by the end of Q2 2020 for each of these portfolios? (Show all of your workings.)

5. Graph the quarterly movements in the future values for each of the five portfolios over the entire investment period. Do you regret having chosen the portfolio that you did in part 2? Explain.

6. Construct and chart a quarterly return frequency distribution for each of the five portfolios over the entire investment period. Do these distributions resemble a normal distribution? Explain.

7. Compute the arithmetic mean and the standard deviation of the quarterly returns for each of the five portfolios over the entire investment period. (Show all of your workings.) Tabulate and graph your results. How do these results compare to your ranking based on risk in part 1? What do you conclude about return and risk?

8. Graph the quarterly returns for each of the five portfolios over the entire investment period. What do you conclude about risk? Using Library online databases and/or the World Wide Web, identify and reference some macroeconomic news that likely accounts for the three largest peaks/troughs in the quarterly returns history for the large stocks portfolio only.

9. You have so far not taken inflation into consideration. Using the data provided for the consumer price index, compute the average quarterly inflation rate over the entire investment period. (Show all of your workings.) Based on the arithmetic means of the nominal quarterly returns that you have computed in part 7, did all five of the portfolios earn on average a real quarterly return that exceeded inflation? What do you conclude?

10. Assuming that the least risky of the five portfolios, based on what you have found in part 7, can for all intents and purposes be regarded as a risk-free investment, and ignoring inflation, compute and tabulate the arithmetic mean of the quarterly risk premium (return in excess of the risk-free return) for each of the other (four) portfolios. (Show all of your workings.) What do these results tell you?

11. Perhaps by utilising some of what you have found from the above historical and quarterly analysis, and again ignoring inflation, provide an estimate of the expected and annualised risk premium from the end of Q2 2020 until the end of Q2 2021 for each of the five portfolios. (Show all of your workings, and state all of the assumptions that you make.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations Of Financial Management

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen

17th Edition

126001391X, 978-1260013917