Question

The two key words for Operating Cash Flows re Operating and Cash. When we use the Indirect Method, we start with Net Income (which includes

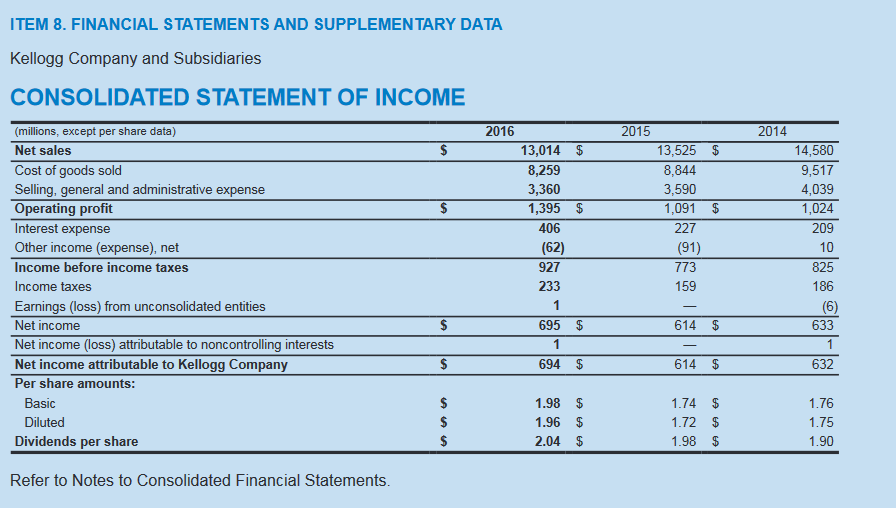

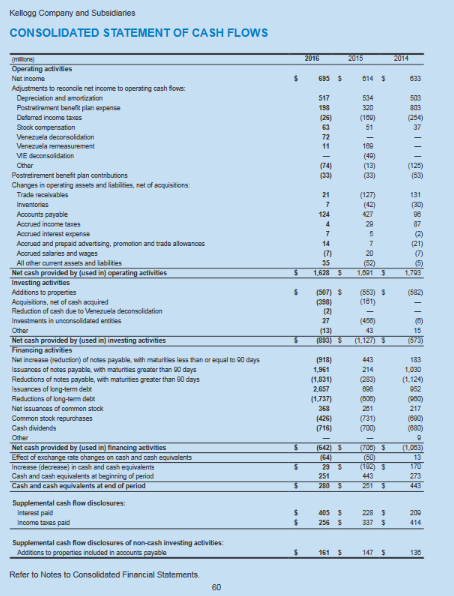

The two key words for Operating Cash Flows re Operating and Cash. When we use the Indirect Method, we start with Net Income (which includes accruals) and adjust for accruals - items that are not fully cash in the Income Statement. When we start with Net Income of $695 in 2016 (first line of OCF), we start with the assumption that we had $695 of net cash inflow from operations in 2016. Implicitly, starting with the Net Income number assumes that every individual line item on the Income Statement is an operating item and is exactly equal to cash received/paid for that item in 2016. All revenue items are inflows of cash and expenses are outflows of cash. We can replace the one line Net Income number ($695) with all the lines on the Income Statement Net Sales inflow of cash, $13,014; Cost of Goods Sold outflow of cash, $8,259, etc. The net inflow of all these items put together will be $695. But, each of these line items are not fully cash (and some may not even be operating). Every adjustment in the Indirect Method relates to one or more line items on the Income Statement for the noncash or non-operating component. For example, in Kelloggs 2016 OCF on page 60, there is an adjustment of $21 for Trade Receivables (TR). What line item on the Income Statement does this adjustment relate to? Trade Receivables are customer accounts therefore it relates to Net Sales. The adjustment of $21 for TR is because we received $21 more from customers than what we sold during the year. So Cash Collected from Customers equals Net Sales plus the adjustment = $13,014 + $21 = $13,035. The Direct Method is not a reconciliation from the Net Income number to Operating Cash Flows. Instead we directly describe all inflows and outflows of cash. For example, the first line in the Direct Method will be Cash received from Customers = $13,035. Similarly, we need to adjust every line item on the Income Statement using the adjustments in the OCF. If you are not clear about which line item an adjustment relates to, make some reasonable assumption and allocate the adjustment if necessary. For example, Kellogg adjusts Depreciation and Amortization (D&A) of $517 in their 2016 OCF. Which line item on the Income Statement does D&A relate to? Could be COGS or SG&A. Why? Allocate proportionately to both COGS and SG&A on some reasonable basis.

12. Use the Income Statement and the operating section of Kellogg's cash flow statement and prepare Kellogg's OCF for 2016 using the Direct Method. Neatly show calculations.

Kellogg's OCF for 2016 (Direct Method)

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA Kellogg Company and Subsidiaries CONSOLIDATED STATEMENT OF INCOME 2016 2015 2014 (millions, except per share data) Net sales Cost of goods sold Selling, general and administrative expense Operating profit Interest expense Other income (expense), net Income before income taxes Income taxes Earnings (loss) from unconsolidated entities Net income Net income (loss) attributable to noncontrolling interests Net income attributable to Kellogg Company Per share amounts: 14,580 9,517 4,039 1,024 209 10 825 186 13,014 $ 13,525 $ 8,259 3,360 8,844 3,590 1,091 $ 1,395 $ 406 (62) 927 233 227 (91) 773 159 695 $ 614 $ 633 694 $ 614 $ 632 1.98 $ 1.96 $ 2.04 $ 1.74 $ 1.72 $ 1.98 $ 1.76 1.75 1.90 Basic Diluted Dividends per share Refer to Notes to Consolidated Financial StatementsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Environmental Auditing Fundamentals And Techniques

Authors: J. Ladd Greeno

2nd Edition

091509410X, 978-0915094103