Question

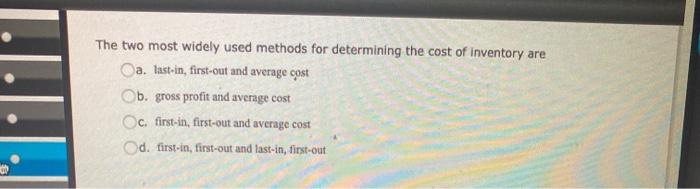

The two most widely used methods for determining the cost of inventory are Oa. last-in, first-out and average cost Ob. gross profit and average cost

The two most widely used methods for determining the cost of inventory are Oa. last-in, first-out and average cost Ob. gross profit and average cost Oc. first-in, first-out and average cost Od. first-in, first-out and last-in, first-out

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Construction Accounting And Financial Management

Authors: Steven J. Peterson

4th Edition

0135232872, 978-0135232873