Question

The U.S. Treasury note yield curve data is given as follows: a) Compute the yield to maturity x of a zero-coupon bond that matures

The U.S. Treasury note yield curve data is given as follows:

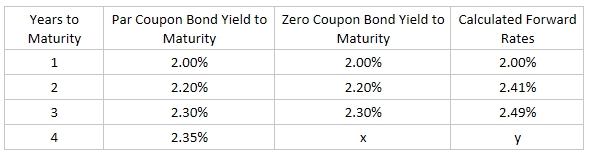

a) Compute the yield to maturity x of a zero-coupon bond that matures in 4 years. The value of x is (rounded to 4 decimal places) 1.

b) If the expectations theory of the yield curve is rounded, what is the forward rate y in year 4? The value of y is (rounded to 4 decimal places) 2.

The Treasury plans to issue a 3-year maturity coupon bond, paying coupons once per year with a coupon rate of 2.25% per annum. The face value of the bond is $100.

c) What will the price of the bond be? The price of the bond is (rounded to 2 decimal places) 3.

d) What will the yield to maturity of the bond be? The yield to maturity of the bond is (rounded to 4 decimal places) 4.

e) If the expectations theory of the yield curve is correct, what is the expected bond price next year? The expected bond price next year is (rounded to 2 decimal places) 5.

Years to Par Coupon Bond Yield to Zero Coupon Bond Yield to Calculated Forward Maturity Maturity Maturity Rates 1 2.00% 2.00% 2.00% 2 2.20% 2.20% 2.41% 3 2.30% 2.30% 2.49% st 4 2.35% X y

Step by Step Solution

3.39 Rating (149 Votes )

There are 3 Steps involved in it

Step: 1

a To compute the yield to maturity x of a zerocoupon bond that matures in 4 years we can use the zer...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Calculus Early Transcendentals

Authors: James Stewart, Daniel K. Clegg, Saleem Watson, Lothar Redlin

9th Edition

1337613924, 978-1337613927