Question

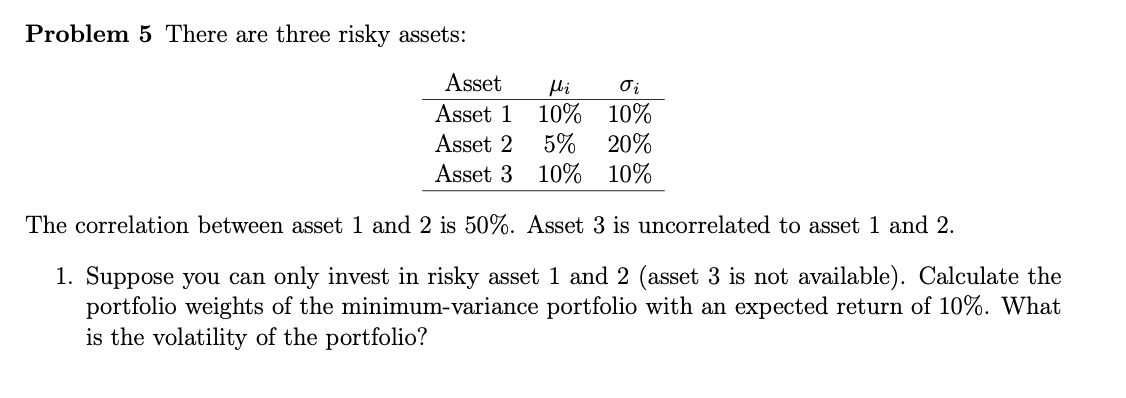

There are three risky assets: Asset Asset 1 Asset 2 Asset 3 i i 10% 10% 5% 20% 10% 10% The correlation between asset 1

There are three risky assets:

Asset Asset 1 Asset 2 Asset 3

i i 10% 10% 5% 20% 10% 10%

The correlation between asset 1 and 2 is 50%. Asset 3 is uncorrelated to asset 1 and 2.

1. Suppose you can only invest in risky asset 1 and 2 (asset 3 is not available). Calculate the portfolio weights of the minimum-variance portfolio with an expected return of 10%. What is the volatility of the portfolio?

-

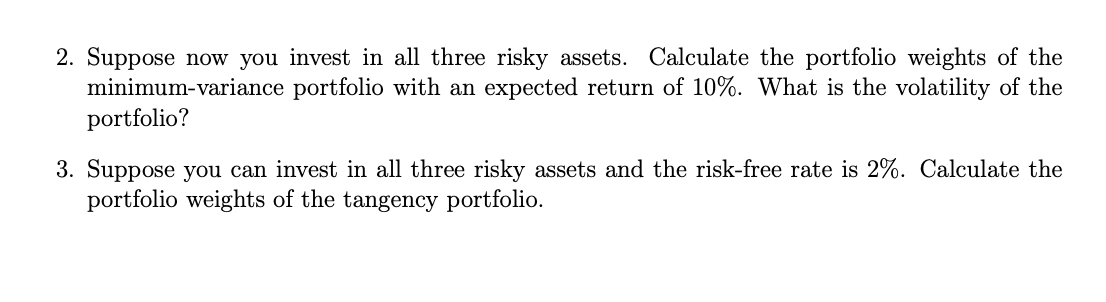

Suppose now you invest in all three risky assets. Calculate the portfolio weights of the minimum-variance portfolio with an expected return of 10%. What is the volatility of the portfolio?

-

Suppose you can invest in all three risky assets and the risk-free rate is 2%. Calculate the portfolio weights of the tangency portfolio.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Wealth Inequality Asset Redistribution And Risk Sharing Islamic Finance

Authors: Tarik Akin , Abbas Mirakhor

1st Edition

3110583739, 3110583887, 9783110583885