Question

There are two assets: i and j with the following characteristics: Expected returns: i = 12% and j = 18%. Risk: i = 30% and

There are two assets: i and j with the following characteristics:

Expected returns: i = 12% and j = 18%.

Risk: i = 30% and j = 40%. ij = 0.5

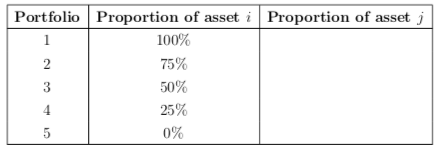

Consider forming a portfolio of assets i and j. Choose the following weights for your construction of feasible portfolios where no asset shorting is allowed:

1. Using portfolio numbers, only plot the feasible set as a continuous curve.

2. Using portfolio numbers, identify the efficient set on the same graph.

Please show all work and upvotes will be given for correct answer!

Portfolio Proportion of asset i Proportion of asset ; 1 100% 2 75% 50% 25% 5 0% 3 4Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management For Technology Start Ups

Authors: Alnoor Bhimani

2nd Edition

1398603082, 978-1398603080