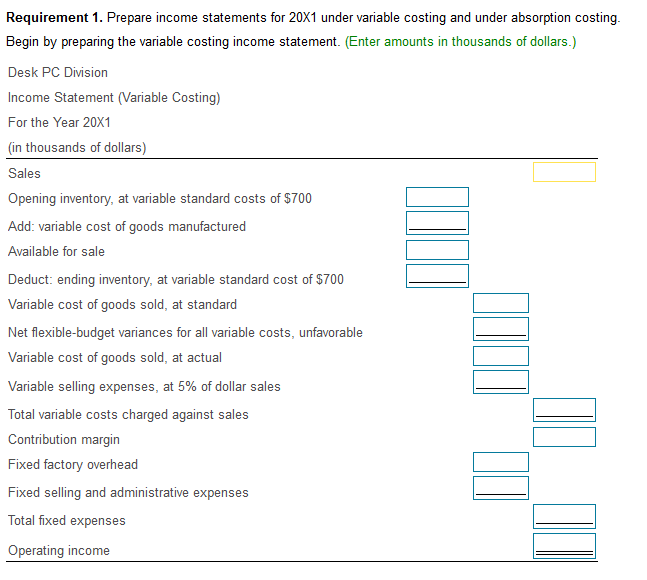

There are two requirements for this question

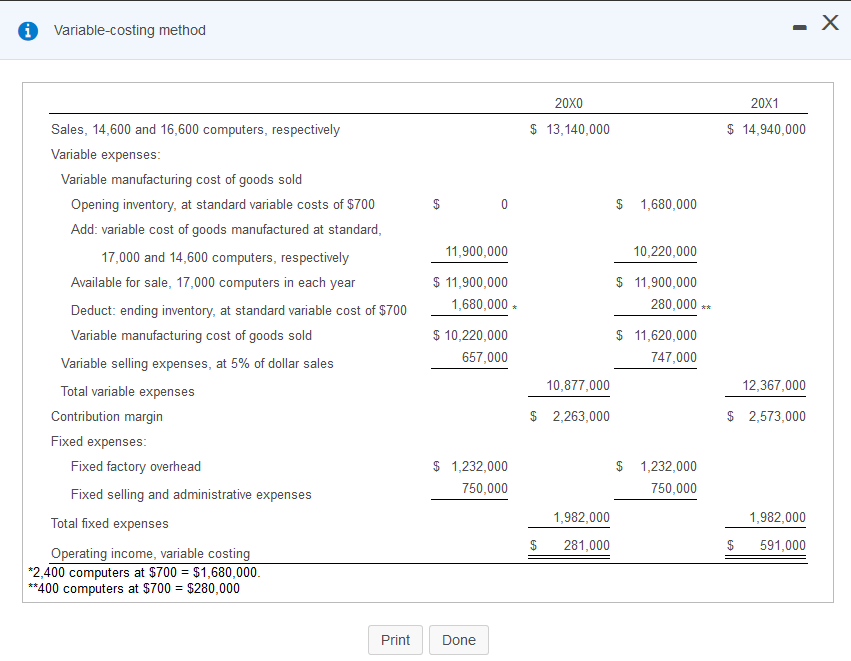

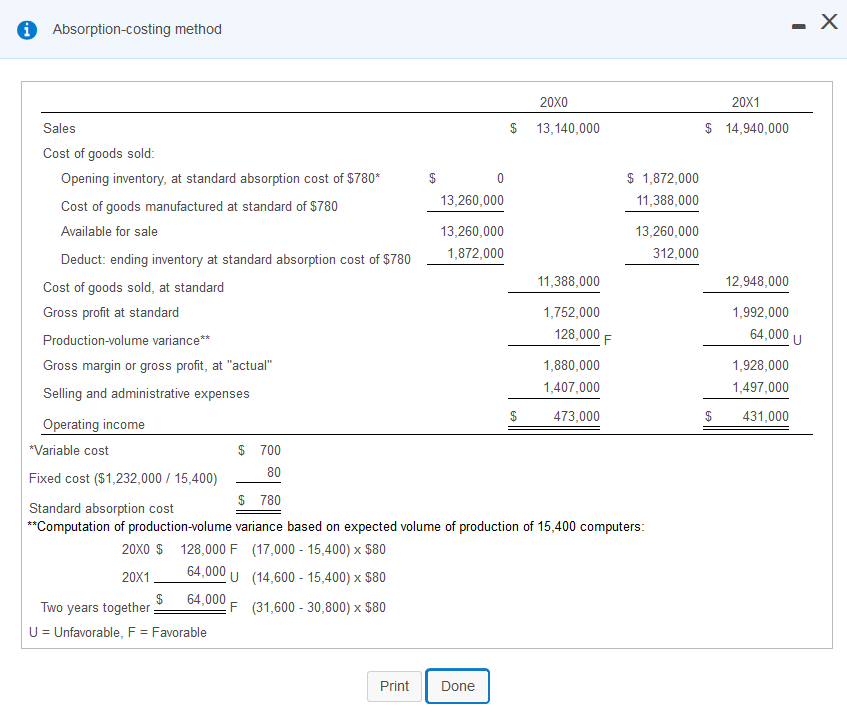

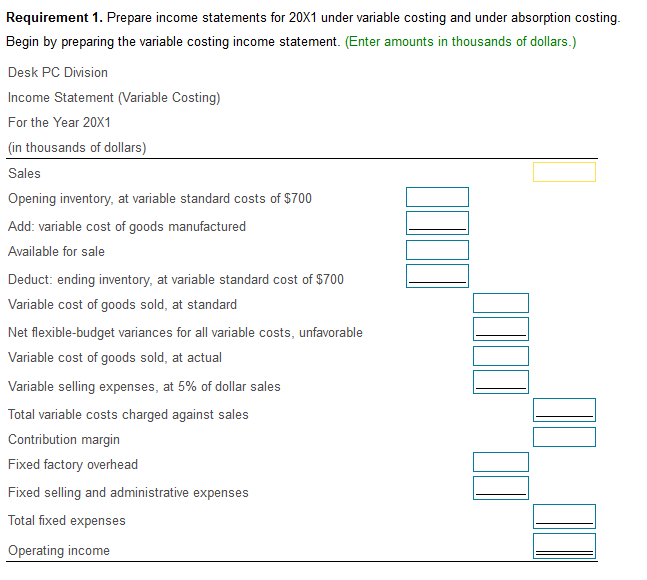

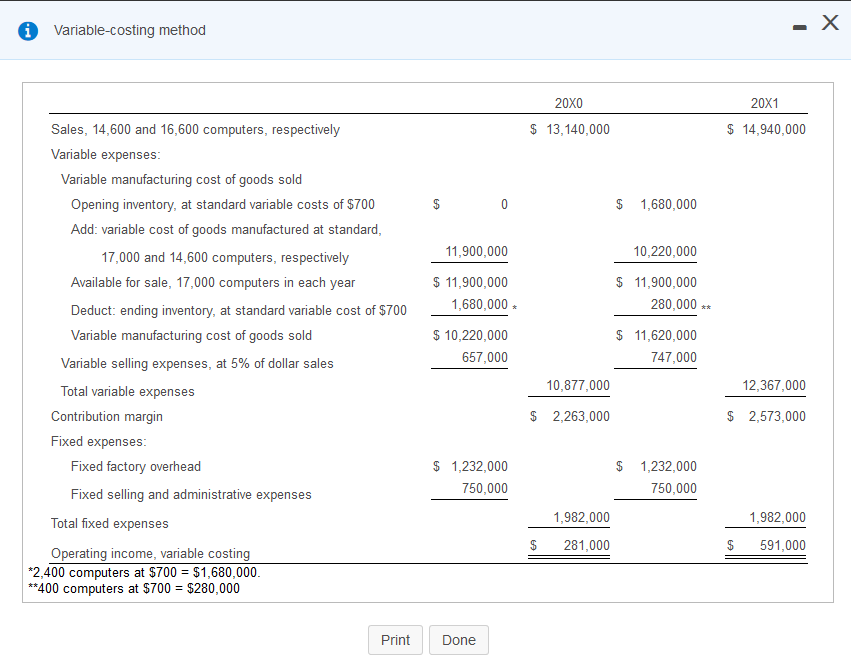

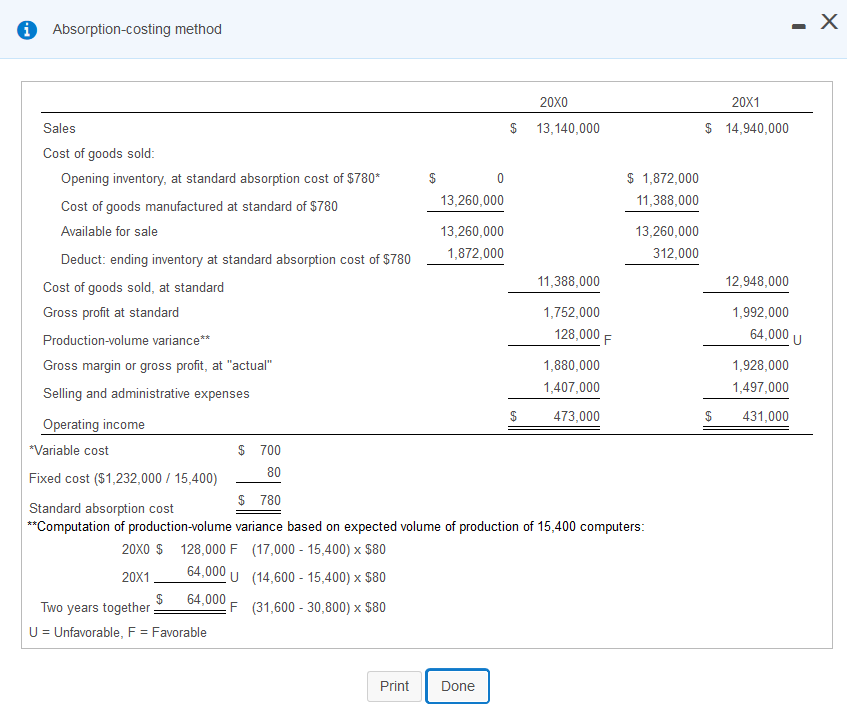

i Requirements X 1. Prepare income statements for 20X1 under variable costing and under absorption costing- 2. Explain why operating income was different under variable costing and absorption costing. Show your calculations. Print DoneThe Desk PC Division has prepared comparative income statements using the variable-costing and absorption-costing methods. Suppose that in 20X1 production was 16,200 computers instead of 14,600 computers, and sales were 15,400 computers. Also assume that the net variances for (Click the icon to view the comparative variable costing income statement.) all variable manufacturing costs were $19,000, unfavorable. Also assume that actual fixed manufacturing costs were $1,292,000. (Click the icon to view the comparative absorption costing income statement.) Read the requirements.i Variable-costing method - X 20X0 20X1 Sales, 14,600 and 16,600 computers, respectively $ 13, 140,000 $ 14,940,000 Variable expenses: Variable manufacturing cost of goods sold Opening inventory, at standard variable costs of $700 69 0 $ 1,680,000 Add: variable cost of goods manufactured at standard, 17,000 and 14,600 computers, respectively 11,900,000 10,220,000 Available for sale, 17,000 computers in each year $ 11,900,000 $ 11,900,000 Deduct: ending inventory, at standard variable cost of $700 1,680,000 280,000 ** Variable manufacturing cost of goods sold $ 10,220,000 $ 11,620,000 Variable selling expenses, at 5% of dollar sales 657,000 747,000 Total variable expenses 10,877,000 12,367,000 Contribution margin $ 2,263,000 $ 2,573,000 Fixed expenses: Fixed factory overhead $ 1,232,000 $ 1,232,000 Fixed selling and administrative expenses 750,000 750,000 Total fixed expenses 1,982,000 1,982,000 Operating income, variable costing $ 281,000 $ 591,000 2,400 computers at $700 = $1,680,000. **400 computers at $700 = $280,000 Print Doneo Absorption{osting method Operating income 20310 20x1 Sales 13,140,000 $ 14,940,000 Cost of goods sold: Opening inventory, at standard absorption cost of $?80* $ 0 $ 1,872,000 Cost of goods manufactured at standard of 357'80 13'250'000 11'388'000 Available for sale 13,280,000 13,280,000 Deduct: ending inventory at standard absorption cost of $T80 1,872,000 312'000 Cost ofgoods sold, at standard 11,388,000 12'948'000 Gross prot at standard 1,?52,000 1,992,000 Production-volume variance" 128,000 F 54'000 U Gross margin or gross prot, at "actual" 1,880,000 1,928,000 Selling and administrative expenses lAUFUUU 1,49?,000 4?3,000 $ 431,000 Wariable cost $ ?00 Fixed cost {$1,232,000 r 15,400} 3\" :5 ran Standard absorption cost 2mm 15 128,000 F (1?,000 -15,400}x$80 2mm w u (14,500 15,4001): $30 Two years together m U = Unfavorable, F = Favorable F [31,500 30,800} x $80 \"Computation of production-volume variance based on expected volume of production of 15,400 computers: Requirement 1. Prepare income statements for 20X1 under variable costing and under absorption costing- Begin by preparing the variable costing income statement. (Enter amounts in thousands of dollars.) Desk PC Division Income Statement (Variable Costing) For the Year 20X1 (in thousands of dollars) Sales Opening inventory, at variable standard costs of $700 Add: variable cost of goods manufactured Available for sale Deduct: ending inventory, at variable standard cost of $700 Variable cost of goods sold, at standard Net flexible-budget variances for all variable costs, unfavorable Variable cost of goods sold, at actual Variable selling expenses, at 5% of dollar sales Total variable costs charged against sales Contribution margin Fixed factory overhead Fixed selling and administrative expenses Total fixed expenses Operating income