Answered step by step

Verified Expert Solution

Question

1 Approved Answer

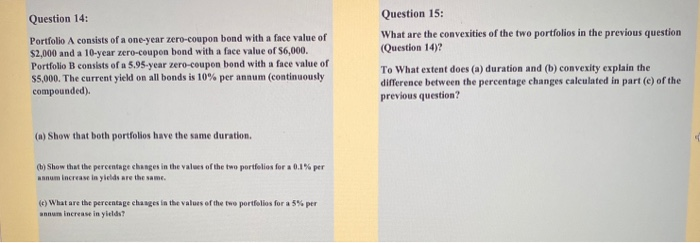

these 2 questions go together so they must be solved together... Please could you use excel and calculations to answer this question? Also please show

these 2 questions go together so they must be solved together...

Please could you use excel and calculations to answer this question? Also please show all the workings... Thanks in advance!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Political Economy Of Chinese Finance

Authors: J. Jay Choi , Michael R. Powers , Xiaotian Tina Zhang

1st Edition

1785609580,1785609572