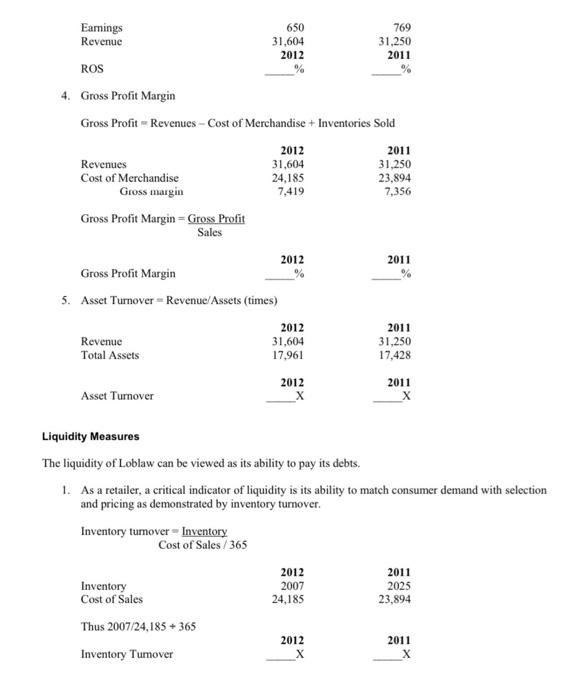

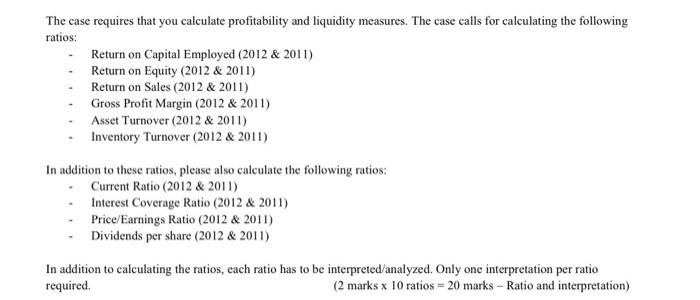

This case, based upon public sources, is designed to provide a framework and a set of skills and concepts to systematically analyze an annual report of a public company, Loblaw Companies Limited. The objective is to understand the company rather than evaluating whether it is a desirable investment opportunity. However, where appropriate, analysis of performance will be undertaken, but this is performance over time rather than comparing Loblaw to other food retailers in Canada. Loblaw is Canada's largest food retailer, focused on supermarkets, superstores and the like. Thus, in various provinces the following retail names are employed: Loblaw's, Valu-Mart, Provigo, Zehrs Markets, No Frills, Save Easy, Atlantic Superstore, T&T Supermarkets, Club Entrept and Maxi, among others. In Canada and elsewhere, public listed companies issue an Annual Report. The objective of the Annual Report is "to provide information about the financial position, performance and changes in financial position of an enterprise that is useful to a wide range of users in making economic decisions." Pages 2 and 3 of the Annual Report present the Financial Highlights. There are certain terms that may require explanation: Operating income: earnings (profit and revenues less normal expenses). EBITDA: earnings before interest, taxes, depreciation (the allocation of the cost of an asset over its useful life) and amortization (the allocated costs expensed for an intangible asset). Gross Profit: sales (revenue) less the costs of the inventory sold to realize that sale. For other unfamiliar terms, go to page 103 of the Financial Review section of the Annual Report. The letter to the shareholders (pages 4 and 5) outlines the five critical elements for achievement of the company's strategy. The first is customer satisfaction, which is measured by the ratio of customers who are strong supporters-score 9, 10 and 11-versus those who are detractors-score 1, 2, 3, 4, 5 and 6. The four other critical elements are best in food, efficiency, growth and employee satisfaction. Pages 16 to 18 outline the governance practices and list the non-executive directors of the Loblaw company. Page 19 outlines the executive officers of the corporation. The financial elements of the Annual Report are contained in the Financial Review. Note particularly the key financial performance indicators on page 5. What are the general conclusions that you can draw? Specifically examine the EBITDA margin, operating margin, free cash flow and return on shareholders' equity (review pages 5 to 10.) Turn to pages 41 to 47. (Except where indicated, you do not need to examine the notes, pages 48 to 99). Prepare an analysis of profitability as follows: 1. Return on capital employed (ROCE)= Net Income Shareholders' Equity + Long-term Debt This measure indicates the profitability of the company relative to the book value of the total funds invested in the company 2011 Earnings (p. 43) 2012 650 769 Liabilities: - Current Liabilities = Term Liabilities 11,544 11,421 -5.396 -4.718 6,148 6,703 + Shareholders' Equity 6.417 6.007 12,565 12,710 ROCE= 2. Return on Equity (ROE) - Net Income Shareholders' Equity 2012 ROE 3. Return on Sales (ROS)- Earnings Revenue 2012 be 2011 2011 769 Earnings Revenue 650 31,604 31,250 2012 2011 ROS % 4. Gross Profit Margin Gross Profit - Revenues-Cost of Merchandise + Inventories Sold 2012 2011 Revenues 31,604 31,250 Cost of Merchandise 24,185 23,894 Gross margin 7,419 7,356 Gross Profit Margin- Gross Profit Sales 2012 2011 Gross Profit Margin % 0% 5. Asset Turnover - Revenue/Assets (times) 2012 2011 Revenue 31,604 31,250 Total Assets 17,961 17,428 2012 2011 Asset Turnover _X X Liquidity Measures The liquidity of Loblaw can be viewed as its ability to pay its debts. 1. As a retailer, a critical indicator of liquidity is its ability to match consumer demand with selection and pricing as demonstrated by inventory turnover. Inventory turnover - Inventory Cost of Sales/365 2012 2011 Inventory 2007 2025 Cost of Sales 24,185 23,894 Thus 2007/24,185 +365 2012 2011 Inventory Turnover X X The case requires that you calculate profitability and liquidity measures. The case calls for calculating the following ratios: Return on Capital Employed (2012 & 2011) Return on Equity (2012 & 2011) Return on Sales (2012 & 2011) Gross Profit Margin (2012 & 2011) . Asset Turnover (2012 & 2011) Inventory Turnover (2012 & 2011) In addition to these ratios, please also calculate the following ratios: Current Ratio (2012 & 2011) Interest Coverage Ratio (2012 & 2011) - Price/Earnings Ratio (2012 & 2011) Dividends per share (2012 & 2011) In addition to calculating the ratios, each ratio has to be interpreted/analyzed. Only one interpretation per ratio required. (2 marks x 10 ratios = 20 marks - Ratio and interpretation) - What is the purpose of the Statement of Comprehensive Income? Refer to Note 15 and explain this item. How much did Loblaw spend on fixed assets this year? What are Earnings per share and Diluted Earnings per share? What is the difference and how is it calculated? What is the significance of Note 24? No need to answer Note 23. Overall, how do you view Loblaw? This case, based upon public sources, is designed to provide a framework and a set of skills and concepts to systematically analyze an annual report of a public company, Loblaw Companies Limited. The objective is to understand the company rather than evaluating whether it is a desirable investment opportunity. However, where appropriate, analysis of performance will be undertaken, but this is performance over time rather than comparing Loblaw to other food retailers in Canada. Loblaw is Canada's largest food retailer, focused on supermarkets, superstores and the like. Thus, in various provinces the following retail names are employed: Loblaw's, Valu-Mart, Provigo, Zehrs Markets, No Frills, Save Easy, Atlantic Superstore, T&T Supermarkets, Club Entrept and Maxi, among others. In Canada and elsewhere, public listed companies issue an Annual Report. The objective of the Annual Report is "to provide information about the financial position, performance and changes in financial position of an enterprise that is useful to a wide range of users in making economic decisions." Pages 2 and 3 of the Annual Report present the Financial Highlights. There are certain terms that may require explanation: Operating income: earnings (profit and revenues less normal expenses). EBITDA: earnings before interest, taxes, depreciation (the allocation of the cost of an asset over its useful life) and amortization (the allocated costs expensed for an intangible asset). Gross Profit: sales (revenue) less the costs of the inventory sold to realize that sale. For other unfamiliar terms, go to page 103 of the Financial Review section of the Annual Report. The letter to the shareholders (pages 4 and 5) outlines the five critical elements for achievement of the company's strategy. The first is customer satisfaction, which is measured by the ratio of customers who are strong supporters-score 9, 10 and 11-versus those who are detractors-score 1, 2, 3, 4, 5 and 6. The four other critical elements are best in food, efficiency, growth and employee satisfaction. Pages 16 to 18 outline the governance practices and list the non-executive directors of the Loblaw company. Page 19 outlines the executive officers of the corporation. The financial elements of the Annual Report are contained in the Financial Review. Note particularly the key financial performance indicators on page 5. What are the general conclusions that you can draw? Specifically examine the EBITDA margin, operating margin, free cash flow and return on shareholders' equity (review pages 5 to 10.) Turn to pages 41 to 47. (Except where indicated, you do not need to examine the notes, pages 48 to 99). Prepare an analysis of profitability as follows: 1. Return on capital employed (ROCE)= Net Income Shareholders' Equity + Long-term Debt This measure indicates the profitability of the company relative to the book value of the total funds invested in the company 2011 Earnings (p. 43) 2012 650 769 Liabilities: - Current Liabilities = Term Liabilities 11,544 11,421 -5.396 -4.718 6,148 6,703 + Shareholders' Equity 6.417 6.007 12,565 12,710 ROCE= 2. Return on Equity (ROE) - Net Income Shareholders' Equity 2012 ROE 3. Return on Sales (ROS)- Earnings Revenue 2012 be 2011 2011 769 Earnings Revenue 650 31,604 31,250 2012 2011 ROS % 4. Gross Profit Margin Gross Profit - Revenues-Cost of Merchandise + Inventories Sold 2012 2011 Revenues 31,604 31,250 Cost of Merchandise 24,185 23,894 Gross margin 7,419 7,356 Gross Profit Margin- Gross Profit Sales 2012 2011 Gross Profit Margin % 0% 5. Asset Turnover - Revenue/Assets (times) 2012 2011 Revenue 31,604 31,250 Total Assets 17,961 17,428 2012 2011 Asset Turnover _X X Liquidity Measures The liquidity of Loblaw can be viewed as its ability to pay its debts. 1. As a retailer, a critical indicator of liquidity is its ability to match consumer demand with selection and pricing as demonstrated by inventory turnover. Inventory turnover - Inventory Cost of Sales/365 2012 2011 Inventory 2007 2025 Cost of Sales 24,185 23,894 Thus 2007/24,185 +365 2012 2011 Inventory Turnover X X The case requires that you calculate profitability and liquidity measures. The case calls for calculating the following ratios: Return on Capital Employed (2012 & 2011) Return on Equity (2012 & 2011) Return on Sales (2012 & 2011) Gross Profit Margin (2012 & 2011) . Asset Turnover (2012 & 2011) Inventory Turnover (2012 & 2011) In addition to these ratios, please also calculate the following ratios: Current Ratio (2012 & 2011) Interest Coverage Ratio (2012 & 2011) - Price/Earnings Ratio (2012 & 2011) Dividends per share (2012 & 2011) In addition to calculating the ratios, each ratio has to be interpreted/analyzed. Only one interpretation per ratio required. (2 marks x 10 ratios = 20 marks - Ratio and interpretation) - What is the purpose of the Statement of Comprehensive Income? Refer to Note 15 and explain this item. How much did Loblaw spend on fixed assets this year? What are Earnings per share and Diluted Earnings per share? What is the difference and how is it calculated? What is the significance of Note 24? No need to answer Note 23. Overall, how do you view Loblaw