Question

This case is about a partner (Justin Rose) in a small apparel company who is considering selling his 50% stake in the firm and attempting

This case is about a partner (Justin Rose) in a small apparel company who is considering selling his 50% stake in the firm and attempting to determine a fair value for the business. There are a number of different approaches to valuing a small, unlisted company and in this case, we'll be considering three of these approaches: 1) liquidation value; 2) the comparables approach; and 3) free cash flow to equity. Some of the analysis you will be performing here is based on the work you have done in previous cases. We will be augmenting this with some new material.

The liquidation approach to valuing a company is based around the assumption that the firm is only worth somewhere around its net asset value (assets minus liabilities). This might be the case when a company is no longer profitable and its future business prospects are bleak. Under such a scenario, a potential buyer would look to purchase the firm for net asset value less an allowance for the risk that the assets are overstated on the company's balance sheet. For example, while a company may have $1,000,000 in receivables, not all of this may be collectable. The potential buyer will take this into account by making an offer that reflects, amongst other items, a reduction in the book value of the receivables by some reasonable percentage.

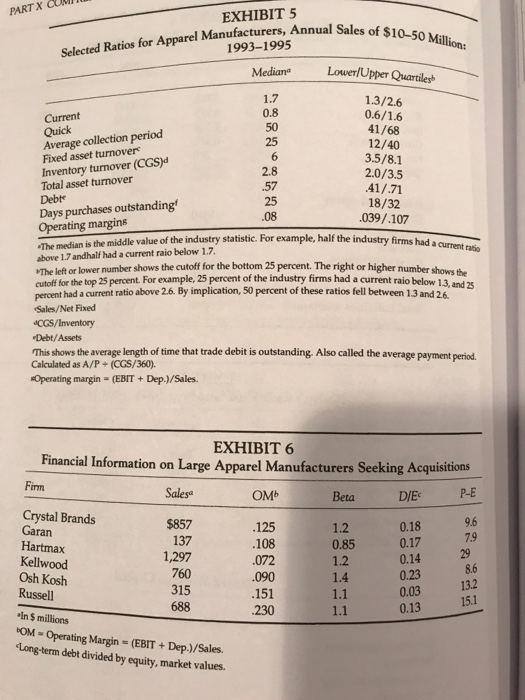

The comparables approach to valuing a company involves estimating the market value of a company by comparing its financial performance via the use of ratios with that of similar companies in the same industry (recall Case 6, Holly Fashions). This can be tricky because there are many factors which might be included in such an analysis including size, operating performance, market position, the growth rate of sales or earnings, capital structure, etc. No two firms are exactly alike so one must be careful to compare 'apples with apples'. Still, the comparables approach is a popular way of assessing the value of a company, particularly when it is not traded on the stock market.

The third approach to valuing a small company is via the use of discounted cash flow analysis. As we have done in past cases, we can forecast a stream of future cash flows and discount these back to the present time to value the equity of the company. In the case of an unlisted company (one that is not traded on the stock market), we typically don't have dividends to discount so we must use an alternative metric. The metric we will use in this week's case is called Free Cash Flow to Equity. It involves utilizing the company's income statement, balance sheet, and/or statement of cash flows to calculate the expected annual free cash flow next year (FCF1). This figure is then inserted as the numerator in the Constant Growth Dividend Valuation Model you employed in Case 3. The denominator remains the cost of equity (Ke) minus the expected constant growth rate (of free cash flow) (g).

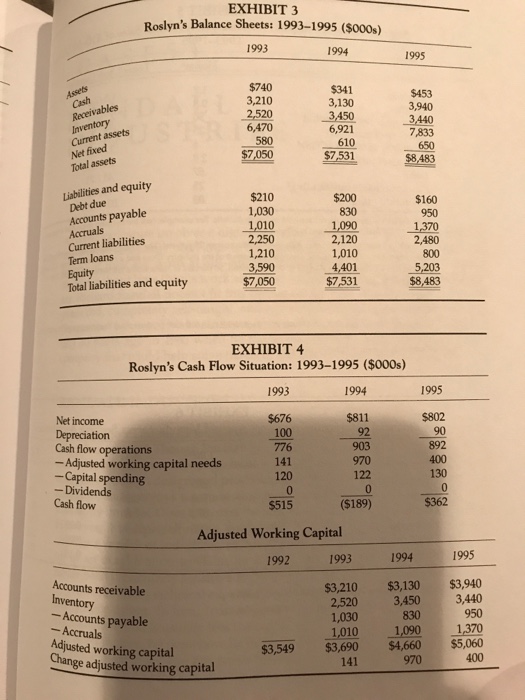

Your assignment this week is to estimate fair value for Roslyn Manufacturing employing each of the three approaches discussed above. The financial data needed to perform these valuations appears in the EXHIBITS for the case; however, you will need to be a very good financial detective and analyst to identify, extract, and correctly apply this data to arrive at a fair estimate for the company's value. I would also suggest you do some supplemental reading on the above valuation methods before tackling this case. Keep in mind, that you will arrive at three different estimates of Roslyn's value based on the three valuation approaches applied.

Here are some additional 'tips' to assist with your analysis:

1) When employing the comparables method, you will be focused on use of the Price-to-Earnings ratio (P/E) of other firms in the same industry. This ratio gives you the multiple of annual earnings (net income) equity investors are prepared to pay for a company. The P/E will vary from one company to another depending on a variety of factors like the growth rate of sales and/or earnings and the amount of debt in the company's capital structure. For example, all else equal, a company's earnings growth rate is positively associated with its P/E; that is, the faster a company is growing its earnings, the higher its P/E. Conversely, all else equal, a higher debt to equity ratio is negatively associated with P/E; that is, the more debt on a company's balance sheet, the lower its P/E. You should consider these relationships when working to determine a fair comparable value (P/E) for Roslyn.

2) When employing the free cash flow to equity method, the net change in term loans between last year and the current year must be added or subtracted from free cash flow in the current year. This is because the change in term loans represents either additional financing cash flow for the firm (in the event term loans have increased) or less financing cash flow (in the event term loans have decreased).

Secondly, to obtain expected free cash flow for the coming year (FCF1) in the numerator of the Constant Growth Model, you must grow free cash flow from last year by the company's growth rate (1+g). In other words, you want next year's free cash flow rather than that from last year.

To arrive at an estimate of Ke in the denominator of the Constant Growth Model, you will use the Capital Asset Pricing Model (CAPM) and will therefore need a value for Roslyn's Beta as well as proxy values for the risk-free asset (rf) and the market portfolio (rm). Beta is heavily influenced by the amount of debt a company has in its capital structure (all else equal, the more debt, the higher the Beta). Thus, try to determine an appropriate Beta for Roslyn by comparing its capital structure to that of other firms in the same industry. You can use the annual return on a 10-year T-Bond as a proxy for the return on the risk-free asset and the annual return on small capitalization stocks as a proxy for the return on the market portfolio. (Both can be obtained from the EXHIBITS in Case 30).

OSL Billion-dollar apparel companies such as Calvin Klein and are unusual in the garment industry, which consists primarily of dozens of ch smaller apparel makers. One such firm is Roslyn Manufacturing, a pro- mul ducer of women's apparel, located in Bedford, New York. The firm was nearly 25 years of experience with a major garment manufacturer. And the partnership initially very and introspective, is creative with a real flair for merchandising and trend Mainly as a result of his genius, the Roslyn label is synonymous with quality and "in" fashions. lynn, outgoing and forceful, has contributed important merchandising and marketing ideas, but has mainly assumed the duties of the firm's chief operating officer. THOUGHTS ON SELLING OUT Rose, however, is seriously considering the sale of his 50 percent interest. Though he still enjoys the creative side of the business, he is tired of the cash crunches that the firm has faced over the years. Periodically the retailers Roslyn deals with have encountered financial difficulties and havestrung out their pay- ments. For example, at one point nearly 40 percent of Roslyn's receivables were more 90 days And in situations like this, companies that receivables would cut back credit advance to the more unstable retailers. A firm like Rosyln faced a unpleasant choice: Either ship to these retailers (which often meant mad scramble k losing sales. Fearful of the second possibility, at would continue to supply all but the most unreason able orders. And quick to point out that, despite this decision, the com pany's average collection period of days is not terribly different from the in dustry of 50 day confi Another reason that Rose wants to sell his interest is that he is losing that uence in managerial expertise. When the firm was small Rose felt nn's OSL Billion-dollar apparel companies such as Calvin Klein and are unusual in the garment industry, which consists primarily of dozens of ch smaller apparel makers. One such firm is Roslyn Manufacturing, a pro- mul ducer of women's apparel, located in Bedford, New York. The firm was nearly 25 years of experience with a major garment manufacturer. And the partnership initially very and introspective, is creative with a real flair for merchandising and trend Mainly as a result of his genius, the Roslyn label is synonymous with quality and "in" fashions. lynn, outgoing and forceful, has contributed important merchandising and marketing ideas, but has mainly assumed the duties of the firm's chief operating officer. THOUGHTS ON SELLING OUT Rose, however, is seriously considering the sale of his 50 percent interest. Though he still enjoys the creative side of the business, he is tired of the cash crunches that the firm has faced over the years. Periodically the retailers Roslyn deals with have encountered financial difficulties and havestrung out their pay- ments. For example, at one point nearly 40 percent of Roslyn's receivables were more 90 days And in situations like this, companies that receivables would cut back credit advance to the more unstable retailers. A firm like Rosyln faced a unpleasant choice: Either ship to these retailers (which often meant mad scramble k losing sales. Fearful of the second possibility, at would continue to supply all but the most unreason able orders. And quick to point out that, despite this decision, the com pany's average collection period of days is not terribly different from the in dustry of 50 day confi Another reason that Rose wants to sell his interest is that he is losing that uence in managerial expertise. When the firm was small Rose felt nn's

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance For Dummies

Authors: Eric Tyson

9th Edition

1119517893, 978-1119517894