THIS IS A CASE STUDY

PLEASE HELP

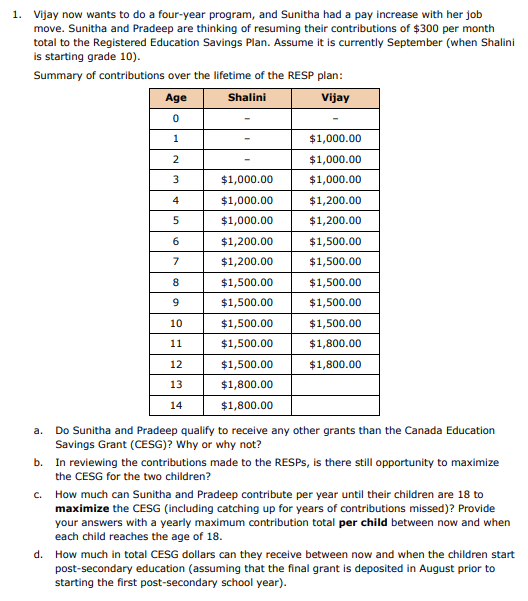

QUESTIONS

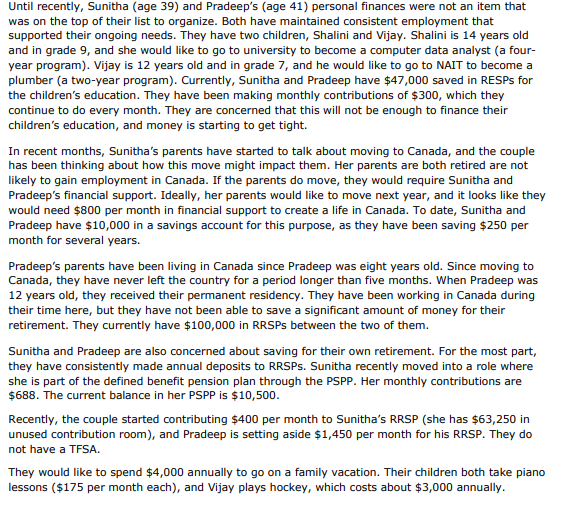

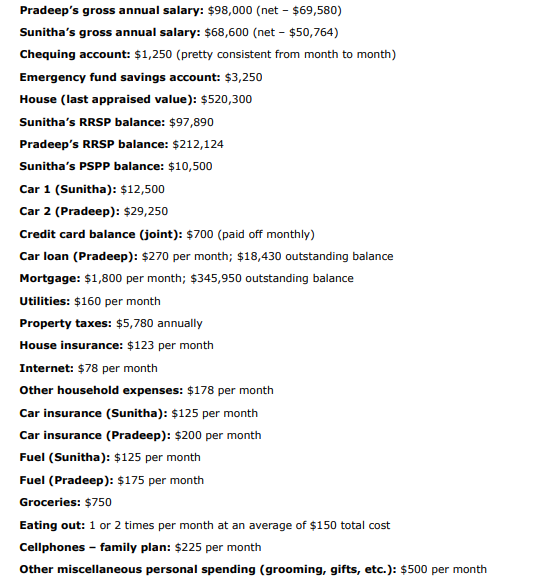

Until recently, Sunitha (age 39) and Pradeep's (age 41) personal finances were not an item that was on the top of their list to organize. Both have maintained consistent employment that supported their ongoing needs. They have two children, Shalini and Vijay. Shalini is 14 years old and in grade 9, and she would like to go to university to become a computer data analyst (a four- year program). Vijay is 12 years old and in grade 7, and he would like to go to NAIT to become a plumber (a two-year program). Currently, Sunitha and Pradeep have $47,000 saved in RESPs for the children's education. They have been making monthly contributions of $300, which they continue to do every month. They are concerned that this will not be enough to finance their children's education, and money is starting to get tight. In recent months, Sunitha's parents have started to talk about moving to Canada, and the couple has been thinking about how this move might impact them. Her parents are both retired are not likely to gain employment in Canada. If the parents do move, they would require Sunitha and Pradeep's financial support. Ideally, her parents would like to move next year, and it looks like they would need $800 per month in financial support to create a life in Canada. To date, Sunitha and Pradeep have $10,000 in a savings account for this purpose, as they have been saving $250 per month for several years. Pradeep's parents have been living in Canada since Pradeep was eight years old. Since moving to Canada, they have never left the country for a period longer than five months. When Pradeep was 12 years old, they received their permanent residency. They have been working in Canada during their time here, but they have not been able to save a significant amount of money for their retirement. They currently have $100,000 in RRSPs between the two of them. Sunitha and Pradeep are also concerned about saving for their own retirement. For the most part, they have consistently made annual deposits to RRSPs. Sunitha recently moved into a role where she is part of the defined benefit pension plan through the PSPP. Her monthly contributions are $688. The current balance in her PSPP is $10,500. Recently, the couple started contributing $400 per month to Sunitha's RRSP (she has $63,250 in unused contribution room), and Pradeep is setting aside $1,450 per month for his RRSP. They do not have a TFSA. They would like to spend $4,000 annually to go on a family vacation. Their children both take piano lessons ($175 per month each), and Vijay plays hockey, which costs about $3,000 annually. Pradeep's gross annual salary: $98,000 (net - $69,580) Sunitha's gross annual salary: $68,600 (net - $50,764) Chequing account: $1,250 (pretty consistent from month to month) Emergency fund savings account: $3,250 House (last appraised value): $520,300 Sunitha's RRSP balance: $97,890 Pradeep's RRSP balance: $212,124 Sunitha's PSPP balance: $10,500 Car 1 (Sunitha): $12,500 Car 2 (Pradeep): $29,250 Credit card balance (joint): $700 (paid off monthly) Car loan (Pradeep): $270 per month; $18,430 outstanding balance Mortgage: $1,800 per month; $345,950 outstanding balance Utilities: $160 per month Property taxes: $5,780 annually House insurance: $123 per month Internet: $78 per month Other household expenses: $178 per month Car insurance (Sunitha): $125 per month Car insurance (Pradeep): $200 per month Fuel (Sunitha): $125 per month Fuel (Pradeep): $175 per month Groceries: $750 Eating out: 1 or 2 times per month at an average of $150 total cost Cellphones - family plan: $225 per month Other miscellaneous personal spending (grooming, gifts, etc.): $500 per month 1. Vijay now wants to do a four-year program, and Sunitha had a pay increase with her job move. Sunitha and Pradeep are thinking of resuming their contributions of $300 per month total to the Registered Education Savings Plan. Assume it is currently September (when Shalini is starting grade 10). Summary of contributions over the lifetime of the RESP plan: Age Shalini Vijay $1,000.00 $1,000.00 $1,000.00 $1,000.00 $1,200.00 $1,200.00 $1,500.00 $1,500.00 $1,500.00 $1,000.00 $1,000.00 $1,200.00 $1,200.00 $1,500.00 $1,500.00 $1,500.00 $1,500.00 $1,500.00 $1,800.00 $1,800.00 $1,500.00 $1,500.00 $1,800.00 $1,800.00 12 13 14 a. Do Sunitha and Pradeep qualify to receive any other grants than the Canada Education Savings Grant (CESG)? Why or why not? b. In reviewing the contributions made to the RESPs, is there still opportunity to maximize the CESG for the two children? c. How much can Sunitha and Pradeep contribute per year until their children are 18 to maximize the CESG (including catching up for years of contributions missed)? Provide your answers with a yearly maximum contribution total per child between now and when each child reaches the age of 18. d. How much in total CESG dollars can they receive between now and when the children start post-secondary education (assuming that the final grant is deposited in August prior to starting the first post-secondary school year). Until recently, Sunitha (age 39) and Pradeep's (age 41) personal finances were not an item that was on the top of their list to organize. Both have maintained consistent employment that supported their ongoing needs. They have two children, Shalini and Vijay. Shalini is 14 years old and in grade 9, and she would like to go to university to become a computer data analyst (a four- year program). Vijay is 12 years old and in grade 7, and he would like to go to NAIT to become a plumber (a two-year program). Currently, Sunitha and Pradeep have $47,000 saved in RESPs for the children's education. They have been making monthly contributions of $300, which they continue to do every month. They are concerned that this will not be enough to finance their children's education, and money is starting to get tight. In recent months, Sunitha's parents have started to talk about moving to Canada, and the couple has been thinking about how this move might impact them. Her parents are both retired are not likely to gain employment in Canada. If the parents do move, they would require Sunitha and Pradeep's financial support. Ideally, her parents would like to move next year, and it looks like they would need $800 per month in financial support to create a life in Canada. To date, Sunitha and Pradeep have $10,000 in a savings account for this purpose, as they have been saving $250 per month for several years. Pradeep's parents have been living in Canada since Pradeep was eight years old. Since moving to Canada, they have never left the country for a period longer than five months. When Pradeep was 12 years old, they received their permanent residency. They have been working in Canada during their time here, but they have not been able to save a significant amount of money for their retirement. They currently have $100,000 in RRSPs between the two of them. Sunitha and Pradeep are also concerned about saving for their own retirement. For the most part, they have consistently made annual deposits to RRSPs. Sunitha recently moved into a role where she is part of the defined benefit pension plan through the PSPP. Her monthly contributions are $688. The current balance in her PSPP is $10,500. Recently, the couple started contributing $400 per month to Sunitha's RRSP (she has $63,250 in unused contribution room), and Pradeep is setting aside $1,450 per month for his RRSP. They do not have a TFSA. They would like to spend $4,000 annually to go on a family vacation. Their children both take piano lessons ($175 per month each), and Vijay plays hockey, which costs about $3,000 annually. Pradeep's gross annual salary: $98,000 (net - $69,580) Sunitha's gross annual salary: $68,600 (net - $50,764) Chequing account: $1,250 (pretty consistent from month to month) Emergency fund savings account: $3,250 House (last appraised value): $520,300 Sunitha's RRSP balance: $97,890 Pradeep's RRSP balance: $212,124 Sunitha's PSPP balance: $10,500 Car 1 (Sunitha): $12,500 Car 2 (Pradeep): $29,250 Credit card balance (joint): $700 (paid off monthly) Car loan (Pradeep): $270 per month; $18,430 outstanding balance Mortgage: $1,800 per month; $345,950 outstanding balance Utilities: $160 per month Property taxes: $5,780 annually House insurance: $123 per month Internet: $78 per month Other household expenses: $178 per month Car insurance (Sunitha): $125 per month Car insurance (Pradeep): $200 per month Fuel (Sunitha): $125 per month Fuel (Pradeep): $175 per month Groceries: $750 Eating out: 1 or 2 times per month at an average of $150 total cost Cellphones - family plan: $225 per month Other miscellaneous personal spending (grooming, gifts, etc.): $500 per month 1. Vijay now wants to do a four-year program, and Sunitha had a pay increase with her job move. Sunitha and Pradeep are thinking of resuming their contributions of $300 per month total to the Registered Education Savings Plan. Assume it is currently September (when Shalini is starting grade 10). Summary of contributions over the lifetime of the RESP plan: Age Shalini Vijay $1,000.00 $1,000.00 $1,000.00 $1,000.00 $1,200.00 $1,200.00 $1,500.00 $1,500.00 $1,500.00 $1,000.00 $1,000.00 $1,200.00 $1,200.00 $1,500.00 $1,500.00 $1,500.00 $1,500.00 $1,500.00 $1,800.00 $1,800.00 $1,500.00 $1,500.00 $1,800.00 $1,800.00 12 13 14 a. Do Sunitha and Pradeep qualify to receive any other grants than the Canada Education Savings Grant (CESG)? Why or why not? b. In reviewing the contributions made to the RESPs, is there still opportunity to maximize the CESG for the two children? c. How much can Sunitha and Pradeep contribute per year until their children are 18 to maximize the CESG (including catching up for years of contributions missed)? Provide your answers with a yearly maximum contribution total per child between now and when each child reaches the age of 18. d. How much in total CESG dollars can they receive between now and when the children start post-secondary education (assuming that the final grant is deposited in August prior to starting the first post-secondary school year)