Answered step by step

Verified Expert Solution

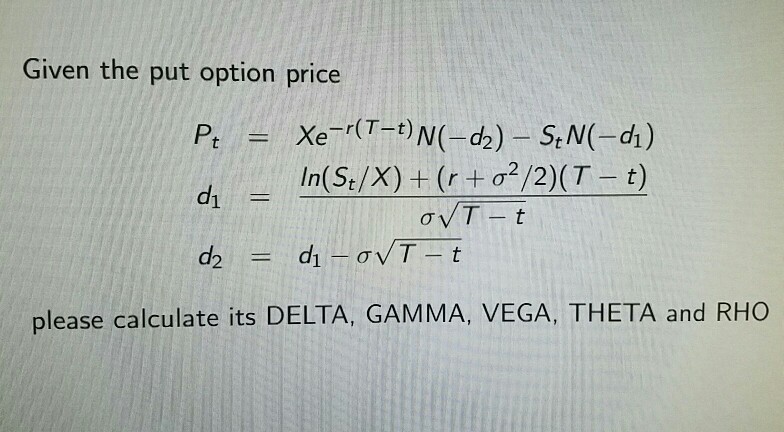

Question

1 Approved Answer

This is a financial risk management question. Calculate the Delta, Gamma, Vega, Theta and Rheo risks. Answer is in symbols. No numerical numbers provided. Given

This is a financial risk management question. Calculate the Delta, Gamma, Vega, Theta and Rheo risks. Answer is in symbols. No numerical numbers provided.

Given the put option price In(St/X) + (r + 2/2)(T-t) d1 = please calculate it s DELTA, GAMMA, VEGA, THETA and RHOStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance In Theory And Practice

Authors: Holley Ulbrich

2nd Edition

041558597X, 978-0415585972