Answered step by step

Verified Expert Solution

Question

1 Approved Answer

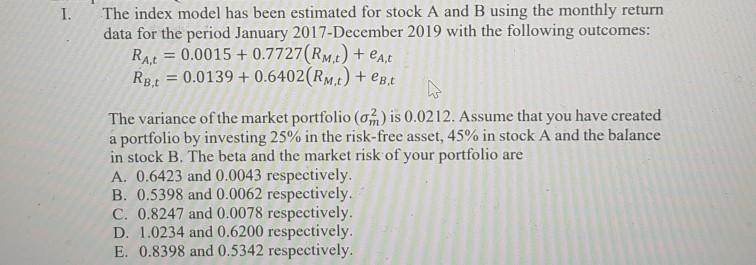

this is a mcq question 1. The index model has been estimated for stock A and B using the monthly return data for the period

this is a mcq question

1. The index model has been estimated for stock A and B using the monthly return data for the period January 2017 December 2019 with the following outcomes: Rat = 0.0015 + 0.7727(Rmt) + est Rp.t = 0.0139 +0.6402(Rmt) + B.t The variance of the market portfolio (om) is 0.0212. Assume that you have created a portfolio by investing 25% in the risk-free asset, 45% in stock A and the balance in stock B. The beta and the market risk of your portfolio are A. 0.6423 and 0.0043 respectively. B. 0.5398 and 0.0062 respectively. C. 0.8247 and 0.0078 respectively. D. 1.0234 and 0.6200 respectively. E. 0.8398 and 0.5342 respectivelyStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Growth And Inequality

Authors: Louis-Philippe Rochon, Virginie Monvoisin

1st Edition

1788973682, 978-1788973687