Question

This is about synergy value allocation to the specific items in post-merger phase. Background: Acquiring firm has identified the $10m of cost synergy (they did

This is about synergy value allocation to the specific items in post-merger phase.

Background:

- Acquiring firm has identified the $10m of cost synergy (they did not quantify nor measure the revenue synergy) (In the Scheme Booklet).

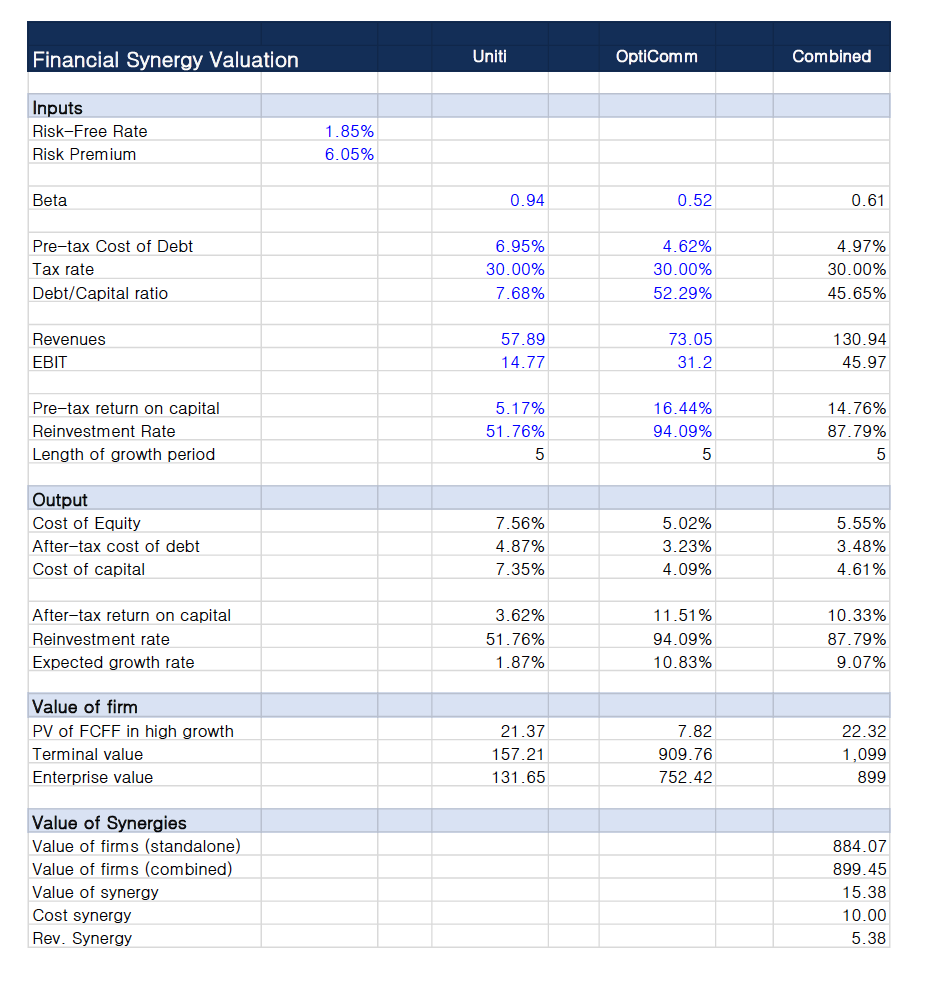

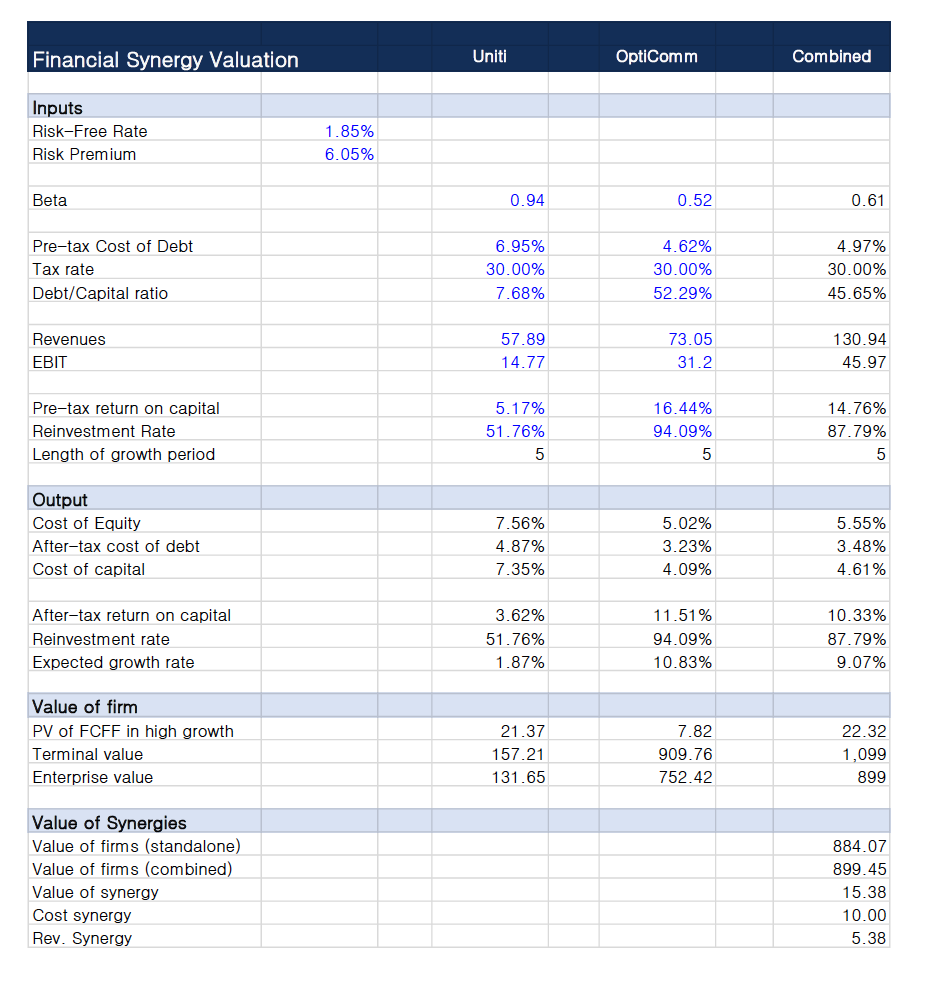

- I have identified the specific items that could get impacted by such realisable synergies as well as total synergy value of $15m, which is different from the Scheme Booklet ($5m gap)

- I want to know how to break down this total cost synergy into specific items that listed below.

The break down of specific items of cost synergy are listed following:

- Redundancy Savings - Elimination of duplicate costs including facilities, premises and administrative services

- Efficiency savings - Elimination of duplicate assets, network supply and backhaul costs

- Corporate cost rationalization - Scale efficiencies through a leaner cost structure and more flexible commercial model to improve market competitiveness

- Economies of scope - Combined group's technology capability

The break down of specific items of revenue synergy are listed following:

- Increased market share - Increased market share in the Greenfield FTTP construction market

- Cross-selling - Expand into adjacent FTTP build markets including retirement living, lifestyle communities, commercial and industrial precincts

- Leveraging marketing resources and capabilities - Ability to challenge dominant fibre players in Brownfields opportunities and consumer markets for Australia

Non of academic literatures shows how to allocate the specific cost & revenue synergy into the break-down components (e.g. Redundancy Savings, Efficiency savings, Cross-selling, etc).

I would like to know how to determine the proportional allocation of such synergies and possible calculation process flow.

(My Synergy Calculation)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantitative Investment Analysis

Authors: Richard A. DeFusco, Dennis W. McLeavey, Jerald E. Pinto, David E. Runkle

3rd edition

111910422X, 978-1119104544, 1119104548, 978-1119104223