Answered step by step

Verified Expert Solution

Question

1 Approved Answer

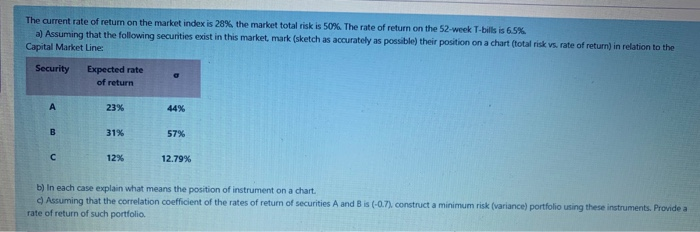

this is all the data The current rate of return on the market index is 28% the market total risk is 50% The rate of

this is all the data

The current rate of return on the market index is 28% the market total risk is 50% The rate of return on the 52-week T-bills is 65% a) Assuming that the following securities exist in this market, mark (sketch as accurately as possible) their position on a chart (total risk vs. rate of return) in relation to the Capital Market Line: Security Expected rate of return 23% 44% B 31% 57% 12% 12.79% b) In each case explain what means the position of instrument on a chart. Assuming that the correlation coefficient of the rates of return of securities A and B is (-0.7), construct a minimum risk (variance) portfolio using these instruments. Provide a rate of return of such portfolio Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance Principles And Practice

Authors: Denzil Watson, Tony Head

1st Edition

0273630083, 978-0273630081