Question

This is an Excel homework on options. Very important: You must label your x-axis and y-axis. You must provide info on the graph, which means

This is an Excel homework on options.

Very important:

You must label your x-axis and y-axis.

You must provide info on the graph, which means what the graph shows, title of the graph.

If there are more than one line on the table, you must separate them either with color or solid versus broken line, as in my lecture notes.

Appendix-2:

Some Problems to Work on Option

NOTE: For each problem on options on stocks, one option contract is equal to 100 shares of underlying stock, e.g. 1 option = 100 share.

For example, if one buys and sell 3 option contract, this amounts to 3x100=300 of shares.

This feature of options on stocks also applies to the premium of options.

For example, if one buys 5 option contract on IBM stocks @ $6.75 for each option, then it means that long position pays total of $3,375 (= $6.75 x 100 x 5)

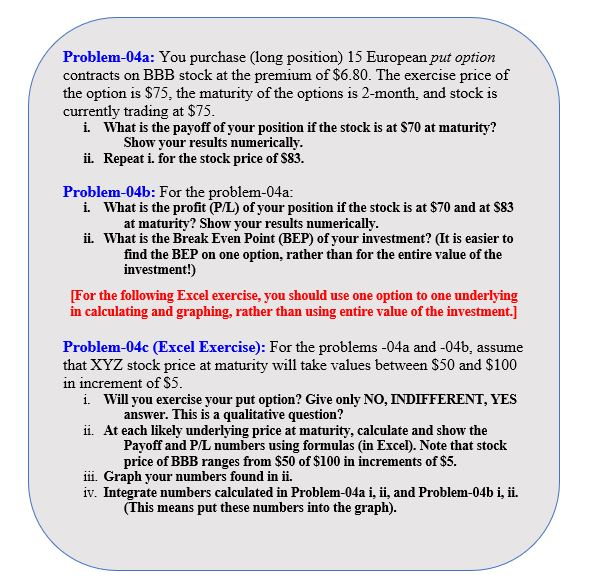

Problem-04a: You purchase (long position) 15 European put option contracts on BBB stock at the premium of $6.80. The exercise price of the option is $75, the maturity of the options is 2-month, and stock is currently trading at $75 i. What is the payoff of your position if the stock is at S70 at maturity? Show your results numerically ii. Repeat i. for the stock price of S83 Problem-04b: For the problem-04a: i. What is the profit (P/L) of your position if the stock is at $70 and at S83 at maturity? Show your results numerically ii. What is the Break Even Point (BEP) of your investment? (It is easier to find the BEP on one option, rather than for the entire value of the investment!) For the following Excel exercise, you should use one option to one underlying in calculating and graphing, rather than using entire value of the investment.] Problem-04c (Excel Exercise): For the problems-04a and -04b, assume that XYZ stock price at maturity will take values between S50 and $100 i. Will you exercise your put option? Give only NO, INDIFFERENT, YES At each likely underlying price at maturity, calculate and show the in increment of S5 answer. This is a qualitative question? ii. Payoff and P/L numbers using formulas (in Excel). Note that stock price of BBB ranges from $50 of $100 in increments of $5 iii. Graph your numbers found in ii. iv. Integrate numbers calculated in Problem-04a i, ii, and Problem-04b i, ii. (This means put these numbers into the graph)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started