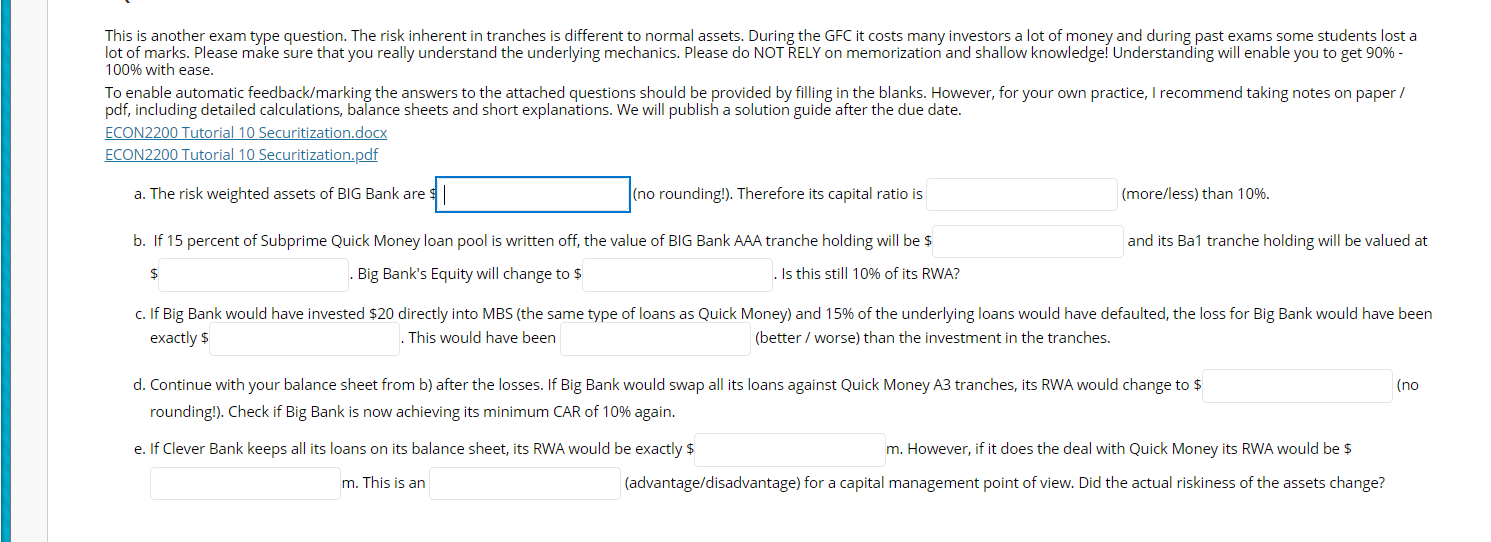

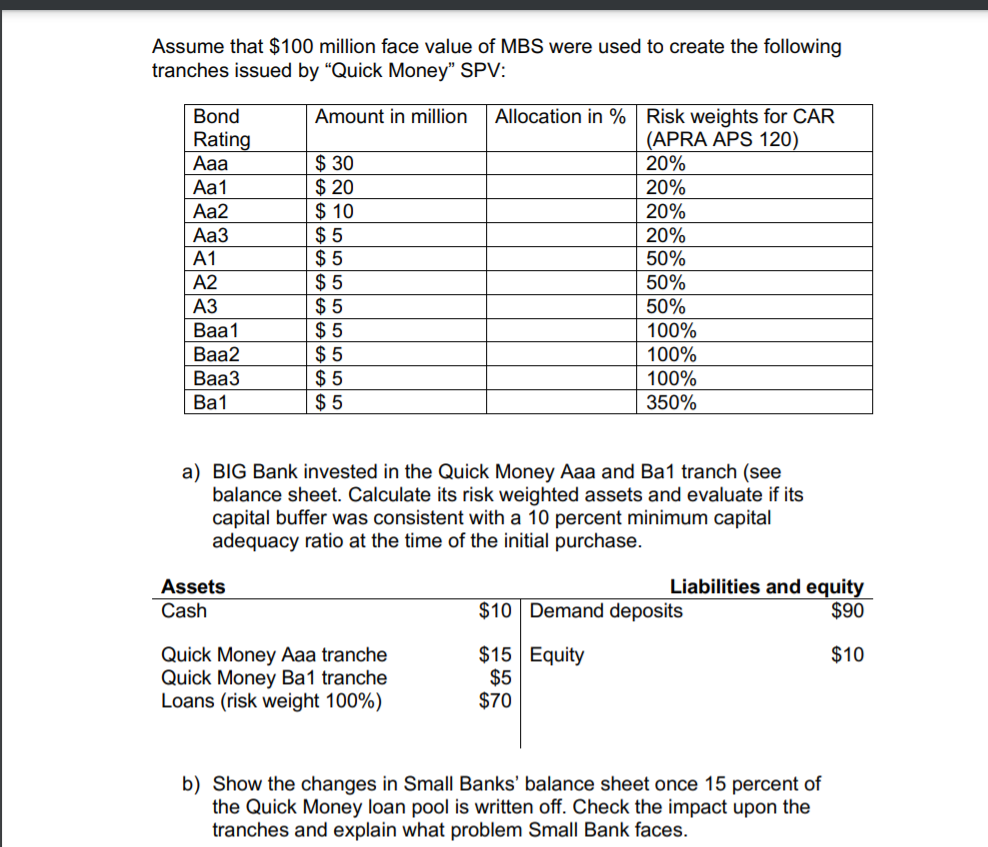

This is another exam type question. The risk inherent in tranches is different to normal assets. During the GFC it costs many investors a lot of money and during past exams some students lost a lot of marks. Please make sure that you really understand the underlying mechanics. Please do NOT RELY on memorization and shallow knowledge! Understanding will enable you to get 90% - 100% with ease. To enable automatic feedback/marking the answers to the attached questions should be provided by filling in the blanks. However, for your own practice, I recommend taking notes on paper / pdf, including detailed calculations, balance sheets and short explanations. We will publish a solution guide after the due date. ECON2200 Tutorial 10 Securitization.docx ECON2200 Tutorial 10 Securitization.pdf a. The risk weighted assets of BIG Bank are (no rounding!). Therefore its capital ratio is (more/less) than 10%. and its Bal tranche holding will be valued at b. If 15 percent of Subprime Quick Money loan pool is written off, the value of BIG Bank AAA tranche holding will be $ . Big Bank's Equity will change to $ . Is this still 10% of its RWA? c. If Big Bank would have invested $20 directly into MBS (the same type of loans as Quick Money) and 15% of the underlying loans would have defaulted, the loss for Big Bank would have been exactly $ . This would have been (better / worse) than the investment in the tranches. (no d. Continue with your balance sheet from b) after the losses. If Big Bank would swap all its loans against Quick Money A3 tranches, its RWA would change to $ rounding!). Check if Big Bank is now achieving its minimum CAR of 10% again. e. If Clever Bank keeps all its loans on its balance sheet, its RWA would be exactly $ m. However, if it does the deal with Quick Money its RWA would be $ m. This is an (advantage/disadvantage) for a capital management point of view. Did the actual riskiness of the assets change? Assume that $100 million face value of MBS were used to create the following tranches issued by Quick Money" SPV: Amount in million Bond Rating Aa1 Aa2 A1 A2 A3 Baa1 Baa2 Baa3 Ba1 $ 30 $ 20 $ 10 $ 5 $ 5 $ 5 $ 5 $ 5 $ 5 $ 5 $ 5 Allocation in % Risk weights for CAR (APRA APS 120) 20% 20% 20% 20% 50% 50% 50% 100% 100% 100% 350% a) BIG Bank invested in the Quick Money Aaa and Ba1 tranch (see balance sheet. Calculate its risk weighted assets and evaluate if its capital buffer was consistent with a 10 percent minimum capital adequacy ratio at the time of the initial purchase. Assets Cash Liabilities and equity $10 Demand deposits $90 $10 Quick Money Aaa tranche Quick Money Ba1 tranche Loans (risk weight 100%) $15 Equity $5 $70 b) Show the changes in Small Banks' balance sheet once 15 percent of the Quick Money loan pool written off. Check the impact upon the tranches and explain what problem Small Bank faces. e) Recall that loans have a regulatory risk weight of 100%. Imagine the "Clever Bank" has $100m loans, which it could sell to its own SPV Quick Money. Quick Money can structure the cash flows from the $100m loans to create the following tranches: 20% Bond Amount in million Risk weights RWA in $m for the Rating for CAR bank buying the (APRA APS whole tranche 120) $ 30 20% Aa1 $ 20 20% Aa2 $ 10 20% $ 5 A1 $ 5 50% A2 $ 5 50% A3 $ 5 50% Baa 1 $ 5 100% Baa2 $ 5 100% Baa3 $ 5 100% Ba1 $ 5 350% Total Comment if it is worth for Clever Bank to sell its loans to Quick Money and then buy all tranches that Quick Money created. This is another exam type question. The risk inherent in tranches is different to normal assets. During the GFC it costs many investors a lot of money and during past exams some students lost a lot of marks. Please make sure that you really understand the underlying mechanics. Please do NOT RELY on memorization and shallow knowledge! Understanding will enable you to get 90% - 100% with ease. To enable automatic feedback/marking the answers to the attached questions should be provided by filling in the blanks. However, for your own practice, I recommend taking notes on paper / pdf, including detailed calculations, balance sheets and short explanations. We will publish a solution guide after the due date. ECON2200 Tutorial 10 Securitization.docx ECON2200 Tutorial 10 Securitization.pdf a. The risk weighted assets of BIG Bank are (no rounding!). Therefore its capital ratio is (more/less) than 10%. and its Bal tranche holding will be valued at b. If 15 percent of Subprime Quick Money loan pool is written off, the value of BIG Bank AAA tranche holding will be $ . Big Bank's Equity will change to $ . Is this still 10% of its RWA? c. If Big Bank would have invested $20 directly into MBS (the same type of loans as Quick Money) and 15% of the underlying loans would have defaulted, the loss for Big Bank would have been exactly $ . This would have been (better / worse) than the investment in the tranches. (no d. Continue with your balance sheet from b) after the losses. If Big Bank would swap all its loans against Quick Money A3 tranches, its RWA would change to $ rounding!). Check if Big Bank is now achieving its minimum CAR of 10% again. e. If Clever Bank keeps all its loans on its balance sheet, its RWA would be exactly $ m. However, if it does the deal with Quick Money its RWA would be $ m. This is an (advantage/disadvantage) for a capital management point of view. Did the actual riskiness of the assets change? Assume that $100 million face value of MBS were used to create the following tranches issued by Quick Money" SPV: Amount in million Bond Rating Aa1 Aa2 A1 A2 A3 Baa1 Baa2 Baa3 Ba1 $ 30 $ 20 $ 10 $ 5 $ 5 $ 5 $ 5 $ 5 $ 5 $ 5 $ 5 Allocation in % Risk weights for CAR (APRA APS 120) 20% 20% 20% 20% 50% 50% 50% 100% 100% 100% 350% a) BIG Bank invested in the Quick Money Aaa and Ba1 tranch (see balance sheet. Calculate its risk weighted assets and evaluate if its capital buffer was consistent with a 10 percent minimum capital adequacy ratio at the time of the initial purchase. Assets Cash Liabilities and equity $10 Demand deposits $90 $10 Quick Money Aaa tranche Quick Money Ba1 tranche Loans (risk weight 100%) $15 Equity $5 $70 b) Show the changes in Small Banks' balance sheet once 15 percent of the Quick Money loan pool written off. Check the impact upon the tranches and explain what problem Small Bank faces. e) Recall that loans have a regulatory risk weight of 100%. Imagine the "Clever Bank" has $100m loans, which it could sell to its own SPV Quick Money. Quick Money can structure the cash flows from the $100m loans to create the following tranches: 20% Bond Amount in million Risk weights RWA in $m for the Rating for CAR bank buying the (APRA APS whole tranche 120) $ 30 20% Aa1 $ 20 20% Aa2 $ 10 20% $ 5 A1 $ 5 50% A2 $ 5 50% A3 $ 5 50% Baa 1 $ 5 100% Baa2 $ 5 100% Baa3 $ 5 100% Ba1 $ 5 350% Total Comment if it is worth for Clever Bank to sell its loans to Quick Money and then buy all tranches that Quick Money created