Answered step by step

Verified Expert Solution

Question

1 Approved Answer

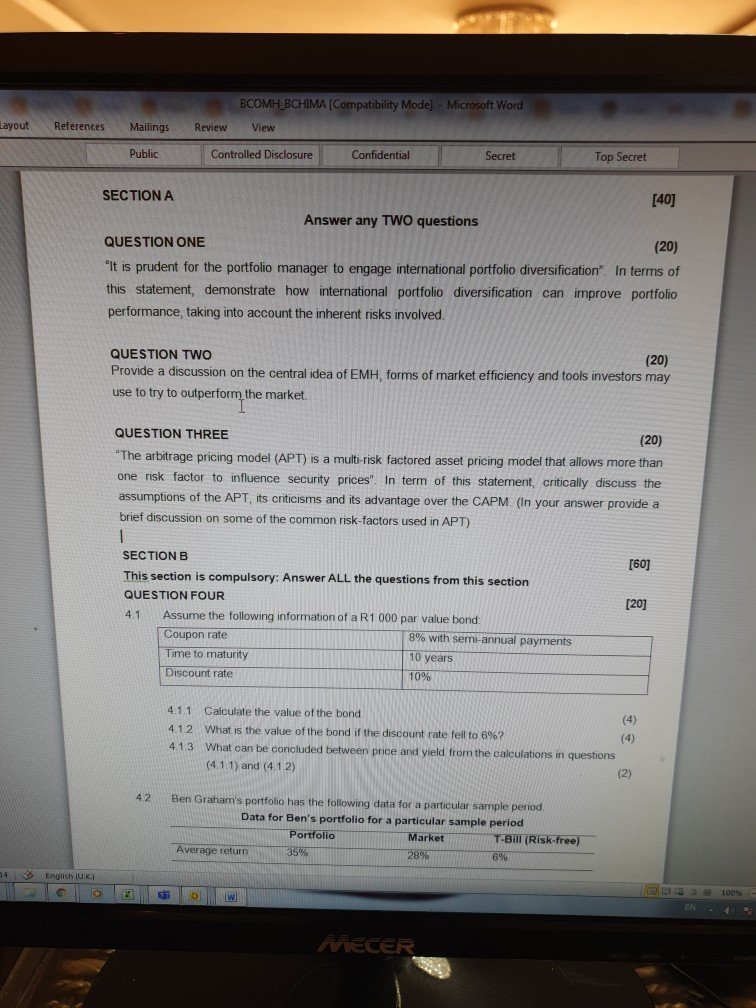

this is investment subject BCOMH_BCHIMA [Compatibility Mode] - Microsoft Word Layout References Mailings Review View Public Controlled Disclosure Confidential Secret Top Secret SECTION A [40]

this is investment subject

BCOMH_BCHIMA [Compatibility Mode] - Microsoft Word Layout References Mailings Review View Public Controlled Disclosure Confidential Secret Top Secret SECTION A [40] Answer any TWO questions QUESTION ONE (20) "It is prudent for the portfolio manager to engage international portfolio diversification". In terms of this statement, demonstrate how international portfolio diversification can improve portfolio performance, taking into account the inherent risks involved QUESTION TWO (20) Provide a discussion on the central idea of EMH, forms of market efficiency and tools investors may use to try to outperform the market. QUESTION THREE (20) "The arbitrage pricing model (APT) is a multi-risk factored asset pricing model that allows more than one risk factor to influence security prices". In term of this statement, critically discuss the assumptions of the APT, its criticisms and its advantage over the CAPM. (In your answer provide a brief discussion on some of the common risk-factors used in APT) - [60] [20] SECTION B This section is compulsory: Answer ALL the questions from this section QUESTION FOUR 4.1 Assume the following information of a R1 000 par value bond: Coupon rate 8% with semi-annual payments Time to maturity 10 years Discount rate 10% 4.1.1 Calculate the value of the bond (4) 4.12 What is the value of the bond if the discount rate fell to 6%? (4) 4.13 What can be concluded between price and yield from the calculations in questions (4.1.1) and (4.1.2) (2) 4.2 Ben Graham's portfolio has the following data for a particular sample period Data for Ben's portfolio for a particular sample period Portfolio Market T-Bill (Risk-free) Average return 35% 28% 6% 24 English (UK) Y 0 w 100% EN METER BCOMH_BCHIMA [Compatibility Mode] - Microsoft Word Layout References Mailings Review View Public Controlled Disclosure Confidential Secret Top Secret SECTION A [40] Answer any TWO questions QUESTION ONE (20) "It is prudent for the portfolio manager to engage international portfolio diversification". In terms of this statement, demonstrate how international portfolio diversification can improve portfolio performance, taking into account the inherent risks involved QUESTION TWO (20) Provide a discussion on the central idea of EMH, forms of market efficiency and tools investors may use to try to outperform the market. QUESTION THREE (20) "The arbitrage pricing model (APT) is a multi-risk factored asset pricing model that allows more than one risk factor to influence security prices". In term of this statement, critically discuss the assumptions of the APT, its criticisms and its advantage over the CAPM. (In your answer provide a brief discussion on some of the common risk-factors used in APT) - [60] [20] SECTION B This section is compulsory: Answer ALL the questions from this section QUESTION FOUR 4.1 Assume the following information of a R1 000 par value bond: Coupon rate 8% with semi-annual payments Time to maturity 10 years Discount rate 10% 4.1.1 Calculate the value of the bond (4) 4.12 What is the value of the bond if the discount rate fell to 6%? (4) 4.13 What can be concluded between price and yield from the calculations in questions (4.1.1) and (4.1.2) (2) 4.2 Ben Graham's portfolio has the following data for a particular sample period Data for Ben's portfolio for a particular sample period Portfolio Market T-Bill (Risk-free) Average return 35% 28% 6% 24 English (UK) Y 0 w 100% EN METERStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Risk Manager Handbook

Authors: Philippe Jorion, Global Association Of Risk Professionals

5th Edition

0470479612, 978-0470479612