Answered step by step

Verified Expert Solution

Question

1 Approved Answer

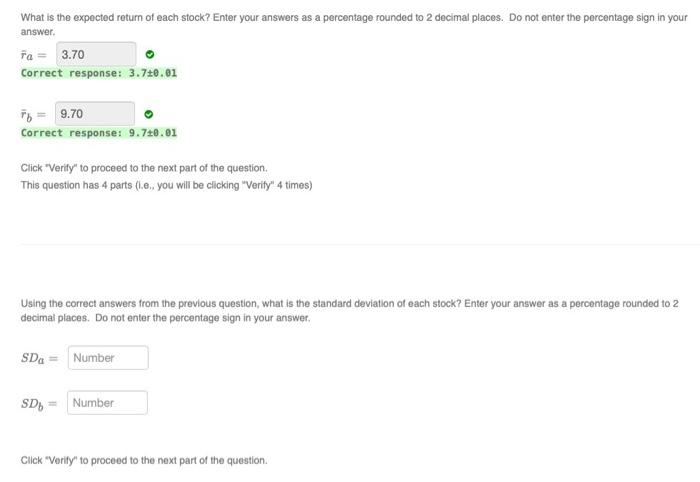

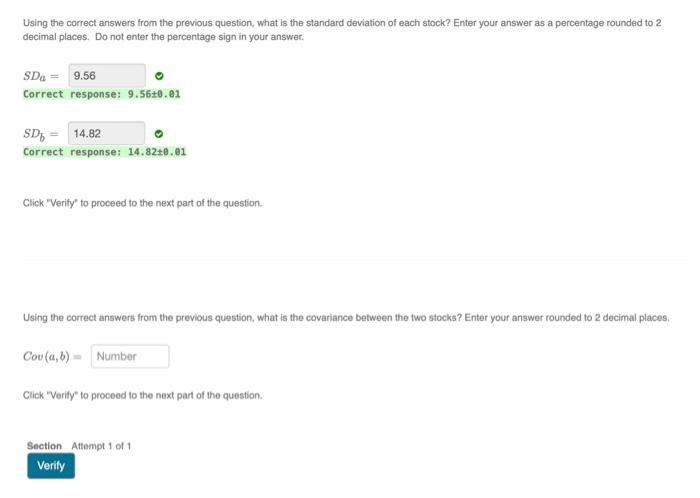

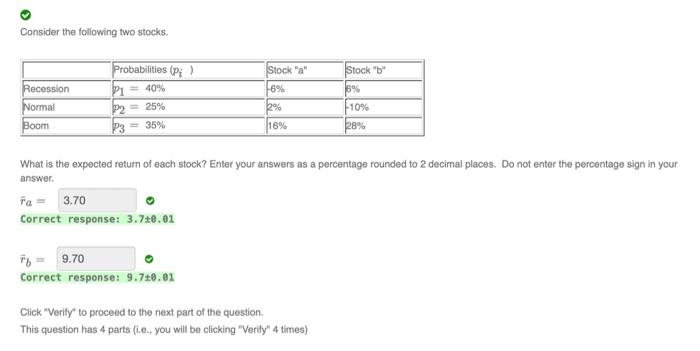

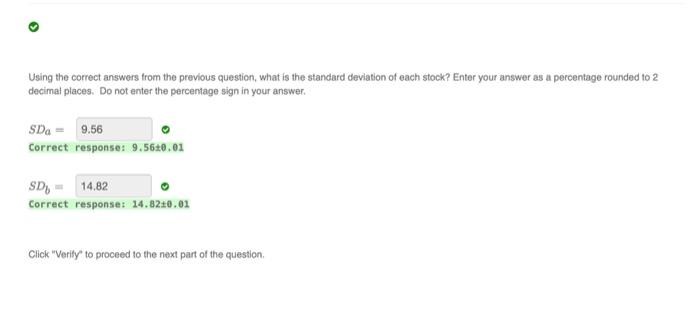

This is one question: Correct response: 3.70.01 rb= Correct response: 9.70.01 Click Verity to proceed to the next part of the question. This question has

This is one question:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Regulation Of Mobile Money Law And Practice In Sub Saharan Africa

Authors: Sunduzwayo Madise

1st Edition

3030138305,3030138313