THIS IS ONE QUESTION WITH MULTIPLE PARTS- IT IS NOT MULTIPLE QUESTIONS ON THE SAME POST. PLEASE ANSWER ALL PARTS CORRECTLY. THANK YOU!!! :)

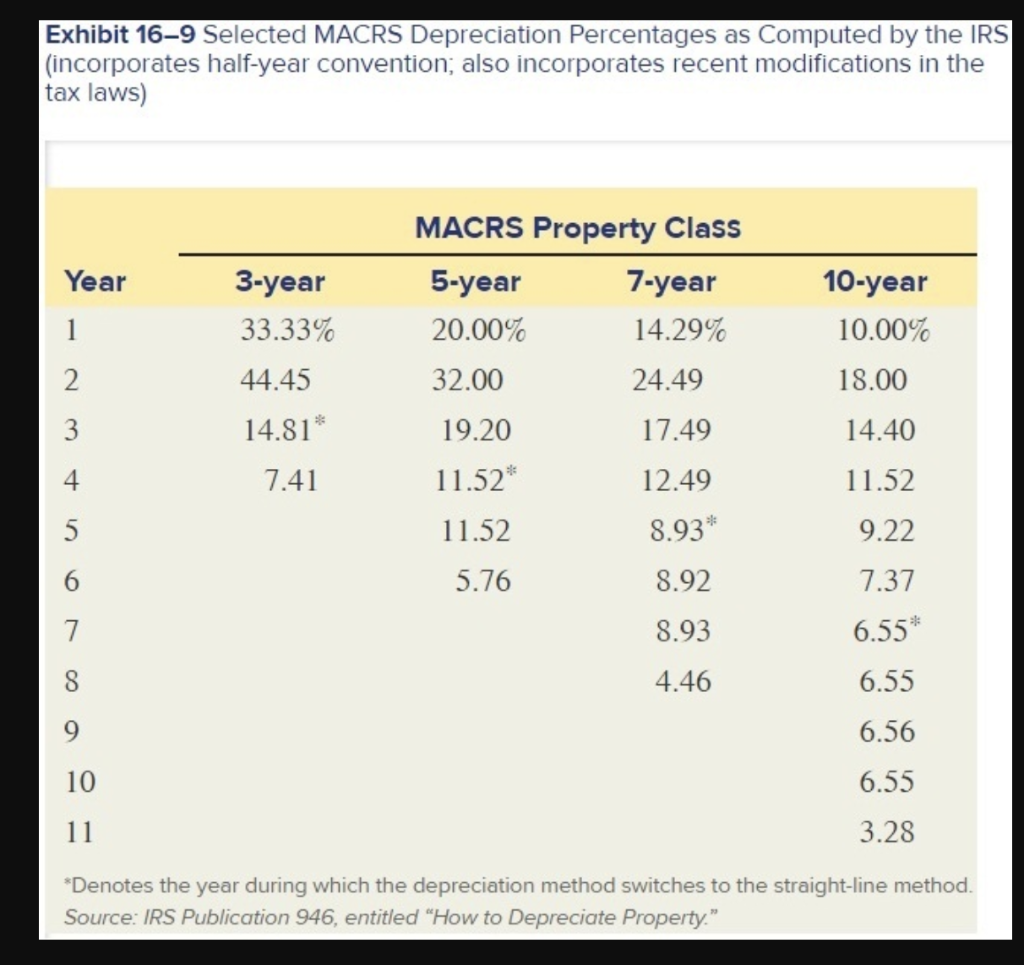

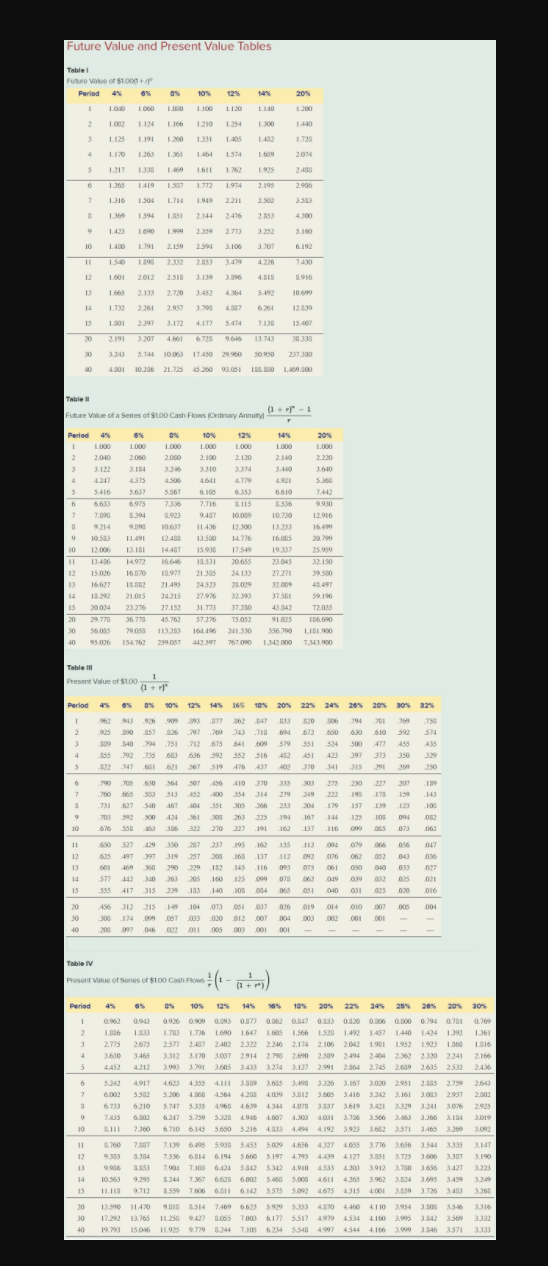

Problem 16-52 Net Present Value; Internal Rate of Return; Payback; Sensitivity Analysis; Taxes (Sections 2, 3) (LO 16-3, 16-4, 16-6, 16-8) The management of Tri-County Air Taxi, Inc., is considering the replacement of an old machine used in its helicopter repair facility. It is fully depreciated but it can be used by the corporation through 20x5. If management decides to replace the old machine, James Transportation Company has offered to purchase it for $74,000 on the replacement date. The old machine would have no salvage value in 20x5. If the replacement occurs, a new machine would be acquired from Hillcrest Industries on December 31, 20x1. The purchase price of $1,300,000 for the new machine would be paid in cash at the time of replacement. Due to the increased efficiency of the new machine, estimated annual cash savings of $420,000 would be generated through 20x5, the end of its expected useful life. The new machine is not expected to have any salvage value at the end of 205. Tri-County's management requires all investments to earn a 14 percent after-tax return. The company's tax rate is 30 percent. The new machine would be classified as three-year property for MACRS purposes. Use Appendix A and Exhibit 16-9. for your reference. (Use appropriate factor(s) from the tables provided.) Required: 1. Compute the net present value of the machine replacement investment. 3. Compute the payback period for the replacement of the machine. 4. How much would the salvage value of the new machine have to be on December 31, 20x5, in order to turn the machine replacement into an acceptable investment? Complete this question by entering your answers in the tabs below. Required 1 Required 3 Required 4 Compute the net present value of the machine replacement investment. (Negative amount should be indicated by a minus sign. Round your intermediate calculations and final answer to the nearest whole dollar.) Net present value Required 1 Required 3 Required 4 Compute the payback period for the replacement of the machine. (Round your answer to 1 decimal place.) Payback period years Exhibit 16-9 Selected MACRS Depreciation Percentages as Computed by the IRS (incorporates half-year convention; also incorporates recent modifications in the tax laws) Year 3-year 33.33% 10-year 10.00% 2 44.45 18.00 MACRS Property Class 5-year 7-year 20.00% 14.29% 32.00 24.49 19.20 17.49 11.52* 12.49 11.52 8.93* 5.76 8.92 3 14.81* 14.40 7.41 11.52 5 9.22 7.37 7 8.93 6.55 8 4.46 6.55 6.56 6.55 10 11 3.28 *Denotes the year during which the depreciation method switches to the straight-line method. Source: IRS Publication 946, entitled "How to Depreciate Property." Future Value and Present Value Tables Table Future Value of $1.000 Period 49 0% 101 149 20% . 100 1.000 1.080 ICO 1.100 1.200 2 1 O 1.166 1210 1.254 0 1440 1125 1.191 1.40 1.-305 12 4 LIO 1.363 1861 1.574 1.609 2014 5 5 1211 1.338 1611 1.762 1.925 6 1419 1.772 1.974 2.195 2.936 1.56 1.714 7 1310 1.50: 1919 2211 2.502 3.583 8 136 1.851 2.476 2.353 2.144 2359 1423 1.690 1.999 2.773 3.100 9 10 1430 1.191 2.150 20 3.100 3.702 1.596 2853 3.479 4.226 OF 2.332 2.518 12 2012 3.396 4.IS 3.916 13 2.133 2.720 4164 5:492 10 61 14 1.732 2031 3700 LT 6.261 12.50 2.36 297 15 1.50 ULIE 3414 7.135 15.07 20 1612 3.307 4. 67 9.646 13.743 333 3.744 10.063 11450 10.236 21.725 45.200 93.051 50.950 237.330 151.530 1.109.300 4.301 Table (1- Future Value of a series of $100 Cash Flows Ordinary Annuity a +1 F Period 4% 0% 10% 12% 20 1 1.000 1.000 1.000 1.000 2 2010 2.000 2.000 2.100 2.120 2.140 2.230 3.122 3310 30 360 4 4.247 4375 1506 4.6.11 4.779 5.364 5 3 5.410 561 5.561 6.100 6.353 6.610 7:42 6 661 6975 7.3.36 7.716 3.115 3.5.36 200 7.590 5.239 8.92 9.437 10.000 10.7.30 12.910 8 9 10601 14 12.00 1323 16. 9 9 10.5 11.491 12483 13.500 14.76 16.065 20790 10 1200 13.151 14487 15.95 17.540 19337 35.00 11 13:40 14972 1666 18531 20655 21045 32.150 12 15.00 16870 13.97 21 24.13 27271 13 167 15 21.49 34523 73.009 32.009 48.497 14 210 27.976 3756 51 15 20.034 2017 27.157 31.773 37.330 4342 72035 20 29.770 45.70 57.276 75.052 91005 156.00 30 7005 11330 161496 2010 356700 116000 40 95.026 154.72 299057 442 597 767090 1,342 000 7.343.900 Fico TI Tabla 1 Present Value of $100 (1+ 0% 10% 12% 14% 14% 16% 10% 20% 22% 24% 201 20 362 333 520 00 .000 2 3 10 477 455 000 435 4 5 20 250 790 10 143 7 8 123 10 Period 4% 30% 32% 943 50983377 753 390151 3:26.2.200 343 718 094 .612 546 24751 712.615 541 609 579 551 524 500 .792.335.683 636 592 552 516 482 451 347 661 621 567 519 476 437 402370 341 315 700641364 456 410 370 385 205 215 220 221 2017 700 668 58313 402 400354 384 299 249 222 193 173 731 427 56 407 40 351 395 386 233 20 179157139 703 92 300 424 361 36263 223 194 167 146 123 105 5583 396 322270 227 191.162.127.116 085 073 527 49 350.27 237 195 162 135 12 084 079066056 011 497 397 319.257 206 168 137 112092076 062052943 469 290 229 182 145 116 093 075 100 940 112 340 26 05 160 125 099 073 062 09009 417 315 299 185 140 105 04 06 05 040 001 312 215 14 104 .073061.037 036 019 .001.003020012002 2060 9 09 052 10 676 02 11 TO 12 13 690 625 501 577 555 19 036 027 021 016 14 020 025 020 ON Ons 15 456 010 00 005 004 20 30 40 014 02 174 03 000 100 004 DI 06 001011 005 003 001 Table IV Proson value of Sories of $100 Cash Flow - atm) SOE 0.70 1.361 1.316 2.166 2.4.6 Period 4% 6% 0% 10% 12 18% 101 20% 22% 24% 25% 20% 1 0.962 0.93 0.926 0.00 0.9930377 0.362 034 0.3.200.06 0.300 0.7940.731 2 2 1.330 1.783 1736 1600 1690 164 1.566 1.528 149 1457 1.440 1.424 1.392 3 2.775 2623 2577 2 2.402 2.40223222246 2.174 2.246 2.114 2.106 2042 1951 1952 1.923 1360 4 3.6.30 3.465 3.312 3.170 3.037 2914 2798 2.6790 2.599 2494 2.404 252 2320 2341 5 412 30 3.191 3.605 3433 3.27 2.122 2.364 2.745 2.09 2015 2532 6 49 4. 4.11 3655 3.326 3.167 $167 3.020 2.951 2355 2.75 7 002 5.58 50 4.366 4.561 435500 3.812 3.00 3.416 32 32423.161 3.063 2.937 3 6.733 6210 3.747 3.35 4.965 4659 454 4078 5619 3.21 3.241 3.07 7.435 0302 3.750 5.325 4946 100 20 4.03 3.7363 3.366 2.184 10 S.111 7.360 6710 6.145 5.6505216 4.333 4.94 39233652 3.652 3.571 3.465 3.269 11 5.760 7.387 7.139 6.195 6.09 5.935 5453 5.000 4.327 4035 3.776 3656 3.5443335 12 7.536 6.314 6.194 5600 519 5.1974.193 4.439 4127 4 127 851 3.725 3.6063357 13 06 7001 7.100 6.43 53 532 2010 4.533 3012730 36563427 14 10.563 7.7 6.625 600 5. 3.000 4 265 3962 3.524 15 11.118 5507606 6.12 5575 5.092 4673 4315 4001 3.650 3.75 20 13.0 11470 9.818 514 7.460 6623 66239 59295.353 48104460 4.4504110 4110 3.954 30 30 17.292 13.00 11.250 9. 3.065 7.003 6.177 5.517 4.979 4.534 4160 3.995 3.500 40 19.793 15.046 11.925 9.7793.244 7.105 6.234 5.548 4997 4544 4.166 3.990 3.546 3.571 260 2.302 2.925 3. 3.092 RO 3.190 3.23 ESSE 3.365 3.316 3.32 3.330 Problem 16-52 Net Present Value; Internal Rate of Return; Payback; Sensitivity Analysis; Taxes (Sections 2, 3) (LO 16-3, 16-4, 16-6, 16-8) The management of Tri-County Air Taxi, Inc., is considering the replacement of an old machine used in its helicopter repair facility. It is fully depreciated but it can be used by the corporation through 20x5. If management decides to replace the old machine, James Transportation Company has offered to purchase it for $74,000 on the replacement date. The old machine would have no salvage value in 20x5. If the replacement occurs, a new machine would be acquired from Hillcrest Industries on December 31, 20x1. The purchase price of $1,300,000 for the new machine would be paid in cash at the time of replacement. Due to the increased efficiency of the new machine, estimated annual cash savings of $420,000 would be generated through 20x5, the end of its expected useful life. The new machine is not expected to have any salvage value at the end of 205. Tri-County's management requires all investments to earn a 14 percent after-tax return. The company's tax rate is 30 percent. The new machine would be classified as three-year property for MACRS purposes. Use Appendix A and Exhibit 16-9. for your reference. (Use appropriate factor(s) from the tables provided.) Required: 1. Compute the net present value of the machine replacement investment. 3. Compute the payback period for the replacement of the machine. 4. How much would the salvage value of the new machine have to be on December 31, 20x5, in order to turn the machine replacement into an acceptable investment? Complete this question by entering your answers in the tabs below. Required 1 Required 3 Required 4 Compute the net present value of the machine replacement investment. (Negative amount should be indicated by a minus sign. Round your intermediate calculations and final answer to the nearest whole dollar.) Net present value Required 1 Required 3 Required 4 Compute the payback period for the replacement of the machine. (Round your answer to 1 decimal place.) Payback period years Exhibit 16-9 Selected MACRS Depreciation Percentages as Computed by the IRS (incorporates half-year convention; also incorporates recent modifications in the tax laws) Year 3-year 33.33% 10-year 10.00% 2 44.45 18.00 MACRS Property Class 5-year 7-year 20.00% 14.29% 32.00 24.49 19.20 17.49 11.52* 12.49 11.52 8.93* 5.76 8.92 3 14.81* 14.40 7.41 11.52 5 9.22 7.37 7 8.93 6.55 8 4.46 6.55 6.56 6.55 10 11 3.28 *Denotes the year during which the depreciation method switches to the straight-line method. Source: IRS Publication 946, entitled "How to Depreciate Property." Future Value and Present Value Tables Table Future Value of $1.000 Period 49 0% 101 149 20% . 100 1.000 1.080 ICO 1.100 1.200 2 1 O 1.166 1210 1.254 0 1440 1125 1.191 1.40 1.-305 12 4 LIO 1.363 1861 1.574 1.609 2014 5 5 1211 1.338 1611 1.762 1.925 6 1419 1.772 1.974 2.195 2.936 1.56 1.714 7 1310 1.50: 1919 2211 2.502 3.583 8 136 1.851 2.476 2.353 2.144 2359 1423 1.690 1.999 2.773 3.100 9 10 1430 1.191 2.150 20 3.100 3.702 1.596 2853 3.479 4.226 OF 2.332 2.518 12 2012 3.396 4.IS 3.916 13 2.133 2.720 4164 5:492 10 61 14 1.732 2031 3700 LT 6.261 12.50 2.36 297 15 1.50 ULIE 3414 7.135 15.07 20 1612 3.307 4. 67 9.646 13.743 333 3.744 10.063 11450 10.236 21.725 45.200 93.051 50.950 237.330 151.530 1.109.300 4.301 Table (1- Future Value of a series of $100 Cash Flows Ordinary Annuity a +1 F Period 4% 0% 10% 12% 20 1 1.000 1.000 1.000 1.000 2 2010 2.000 2.000 2.100 2.120 2.140 2.230 3.122 3310 30 360 4 4.247 4375 1506 4.6.11 4.779 5.364 5 3 5.410 561 5.561 6.100 6.353 6.610 7:42 6 661 6975 7.3.36 7.716 3.115 3.5.36 200 7.590 5.239 8.92 9.437 10.000 10.7.30 12.910 8 9 10601 14 12.00 1323 16. 9 9 10.5 11.491 12483 13.500 14.76 16.065 20790 10 1200 13.151 14487 15.95 17.540 19337 35.00 11 13:40 14972 1666 18531 20655 21045 32.150 12 15.00 16870 13.97 21 24.13 27271 13 167 15 21.49 34523 73.009 32.009 48.497 14 210 27.976 3756 51 15 20.034 2017 27.157 31.773 37.330 4342 72035 20 29.770 45.70 57.276 75.052 91005 156.00 30 7005 11330 161496 2010 356700 116000 40 95.026 154.72 299057 442 597 767090 1,342 000 7.343.900 Fico TI Tabla 1 Present Value of $100 (1+ 0% 10% 12% 14% 14% 16% 10% 20% 22% 24% 201 20 362 333 520 00 .000 2 3 10 477 455 000 435 4 5 20 250 790 10 143 7 8 123 10 Period 4% 30% 32% 943 50983377 753 390151 3:26.2.200 343 718 094 .612 546 24751 712.615 541 609 579 551 524 500 .792.335.683 636 592 552 516 482 451 347 661 621 567 519 476 437 402370 341 315 700641364 456 410 370 385 205 215 220 221 2017 700 668 58313 402 400354 384 299 249 222 193 173 731 427 56 407 40 351 395 386 233 20 179157139 703 92 300 424 361 36263 223 194 167 146 123 105 5583 396 322270 227 191.162.127.116 085 073 527 49 350.27 237 195 162 135 12 084 079066056 011 497 397 319.257 206 168 137 112092076 062052943 469 290 229 182 145 116 093 075 100 940 112 340 26 05 160 125 099 073 062 09009 417 315 299 185 140 105 04 06 05 040 001 312 215 14 104 .073061.037 036 019 .001.003020012002 2060 9 09 052 10 676 02 11 TO 12 13 690 625 501 577 555 19 036 027 021 016 14 020 025 020 ON Ons 15 456 010 00 005 004 20 30 40 014 02 174 03 000 100 004 DI 06 001011 005 003 001 Table IV Proson value of Sories of $100 Cash Flow - atm) SOE 0.70 1.361 1.316 2.166 2.4.6 Period 4% 6% 0% 10% 12 18% 101 20% 22% 24% 25% 20% 1 0.962 0.93 0.926 0.00 0.9930377 0.362 034 0.3.200.06 0.300 0.7940.731 2 2 1.330 1.783 1736 1600 1690 164 1.566 1.528 149 1457 1.440 1.424 1.392 3 2.775 2623 2577 2 2.402 2.40223222246 2.174 2.246 2.114 2.106 2042 1951 1952 1.923 1360 4 3.6.30 3.465 3.312 3.170 3.037 2914 2798 2.6790 2.599 2494 2.404 252 2320 2341 5 412 30 3.191 3.605 3433 3.27 2.122 2.364 2.745 2.09 2015 2532 6 49 4. 4.11 3655 3.326 3.167 $167 3.020 2.951 2355 2.75 7 002 5.58 50 4.366 4.561 435500 3.812 3.00 3.416 32 32423.161 3.063 2.937 3 6.733 6210 3.747 3.35 4.965 4659 454 4078 5619 3.21 3.241 3.07 7.435 0302 3.750 5.325 4946 100 20 4.03 3.7363 3.366 2.184 10 S.111 7.360 6710 6.145 5.6505216 4.333 4.94 39233652 3.652 3.571 3.465 3.269 11 5.760 7.387 7.139 6.195 6.09 5.935 5453 5.000 4.327 4035 3.776 3656 3.5443335 12 7.536 6.314 6.194 5600 519 5.1974.193 4.439 4127 4 127 851 3.725 3.6063357 13 06 7001 7.100 6.43 53 532 2010 4.533 3012730 36563427 14 10.563 7.7 6.625 600 5. 3.000 4 265 3962 3.524 15 11.118 5507606 6.12 5575 5.092 4673 4315 4001 3.650 3.75 20 13.0 11470 9.818 514 7.460 6623 66239 59295.353 48104460 4.4504110 4110 3.954 30 30 17.292 13.00 11.250 9. 3.065 7.003 6.177 5.517 4.979 4.534 4160 3.995 3.500 40 19.793 15.046 11.925 9.7793.244 7.105 6.234 5.548 4997 4544 4.166 3.990 3.546 3.571 260 2.302 2.925 3. 3.092 RO 3.190 3.23 ESSE 3.365 3.316 3.32 3.330