THIS IS RELATED TO PDIC LAW note: the problem here is whether or not the respondents has an outstanding deposit subject to insurance by the

THIS IS RELATED TO PDIC LAW

note: the problem here is whether or not the respondents has an outstanding deposit subject to insurance by the PDIC

G.R. No. 219909 (PDIC v. Dizon & Uy):

https://sc.judiciary.gov.ph/13368/

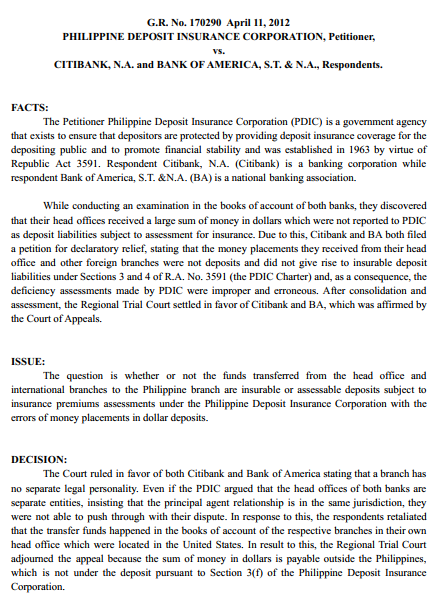

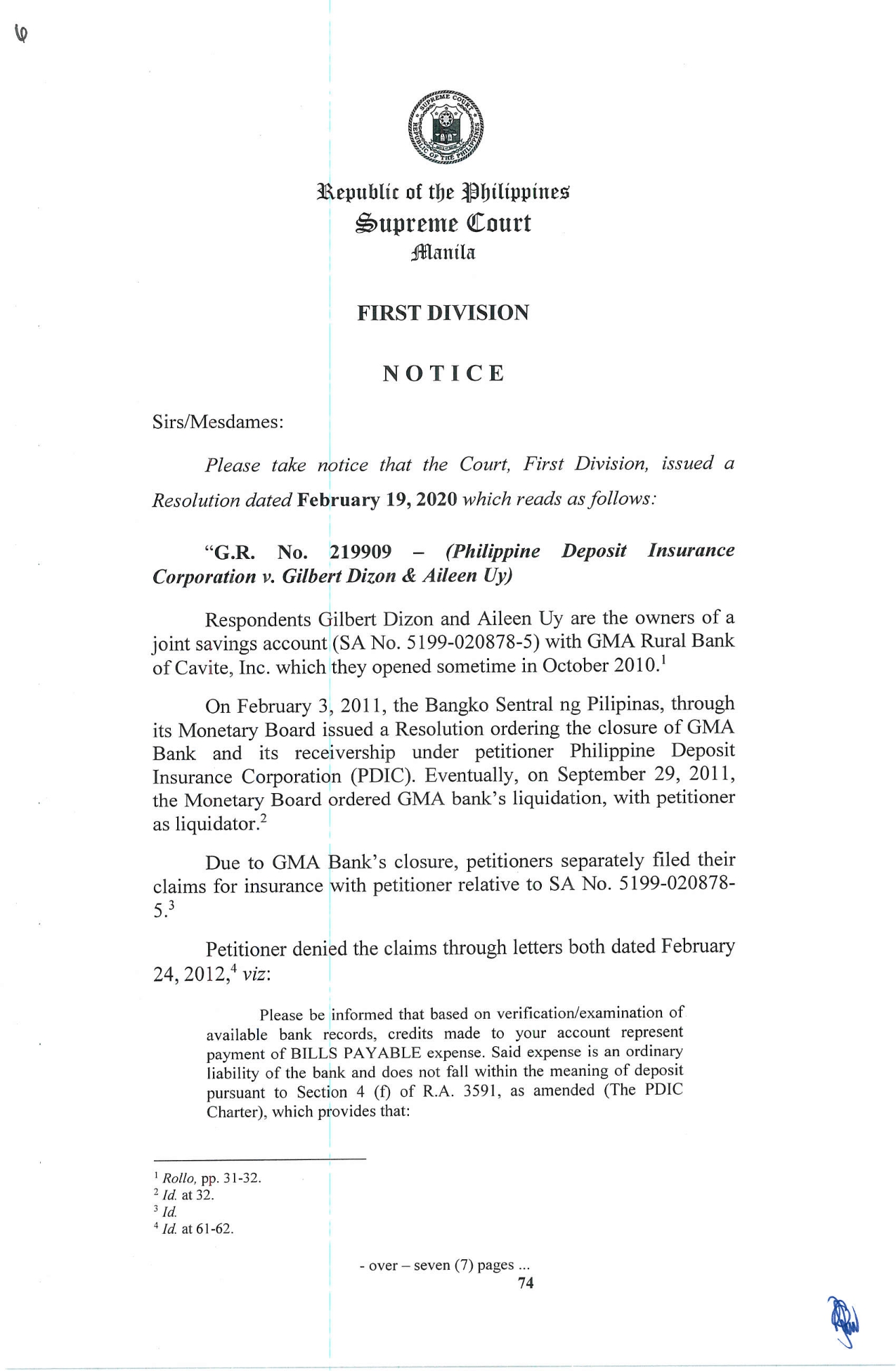

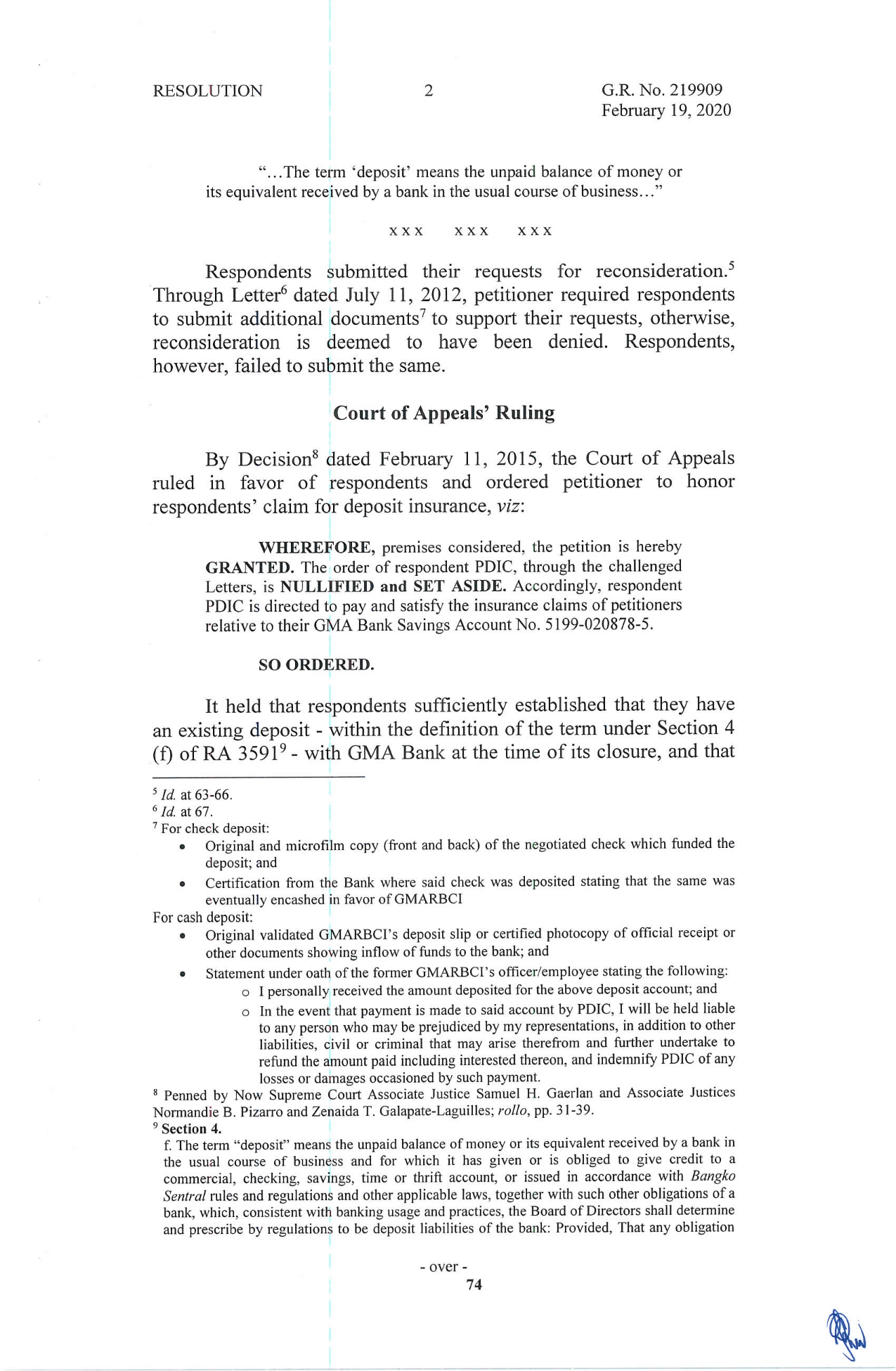

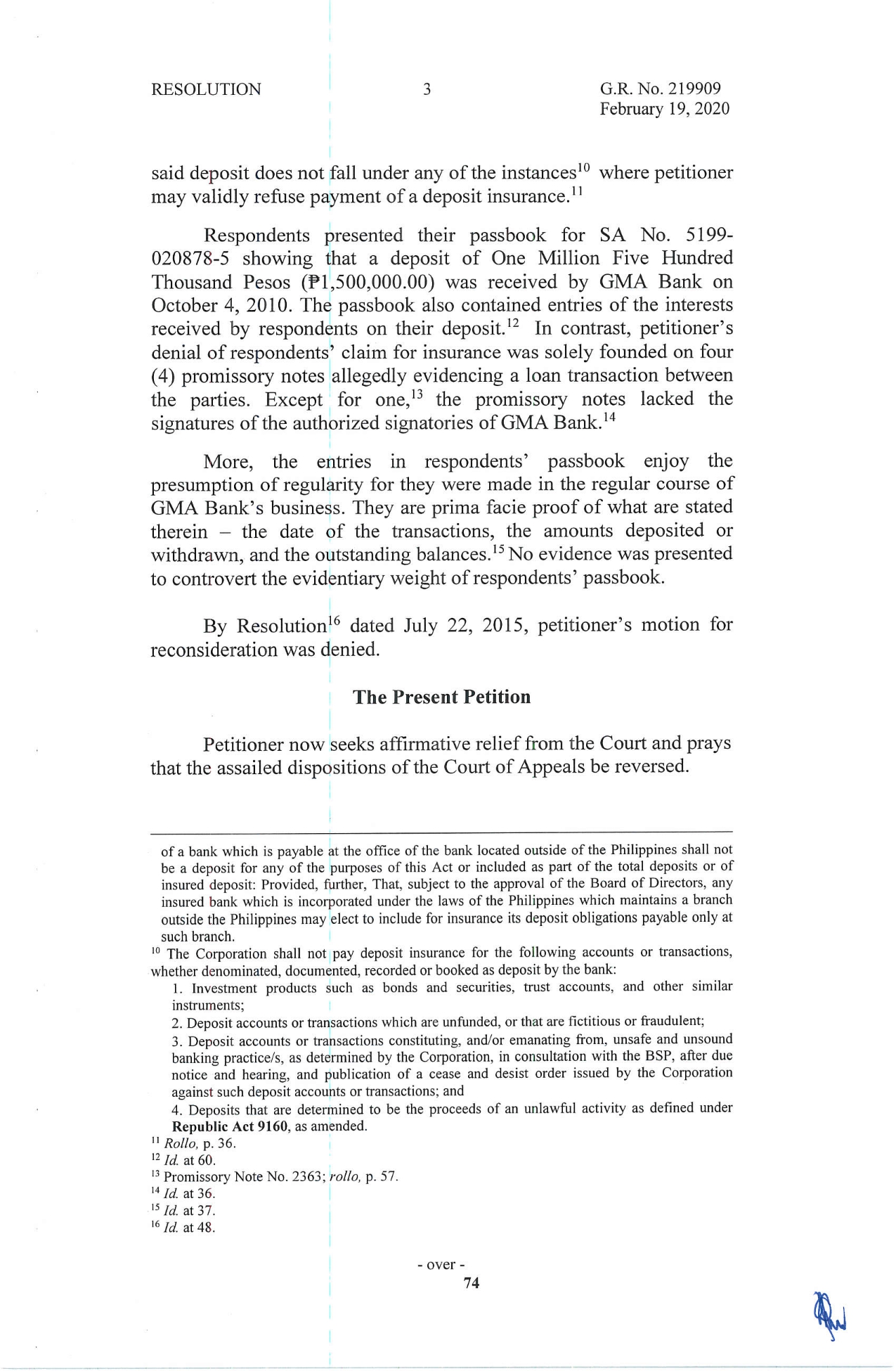

G.R. No. 170290 April 11, 2012 PHILIPPINE DEPOSIT INSURANCE CORPORATION, Petitioner, VS. CITIBANK, N.A. and BANK OF AMERICA, S.T. & N.A., Respondents. FACTS: The Petitioner Philippine Deposit Insurance Corporation (PDIC) is a government agency that exists to ensure that depositors are protected by providing deposit insurance coverage for the depositing public and to promote financial stability and was established in 1963 by virtue of Republic Act 3591. Respondent Citibank, N.A. (Citibank) is a banking corporation while respondent Bank of America, S.T. &N.A. (BA) is a national banking association. While conducting an examination in the books of account of both banks, they discovered that their head offices received a large sum of money in dollars which were not reported to PDIC as deposit liabilities subject to assessment for insurance. Due to this, Citibank and BA both filed a petition for declaratory relief, stating that the money placements they received from their head office and other foreign branches were not deposits and did not give rise to insurable deposit liabilities under Sections 3 and 4 of R.A. No. 3591 (the PDIC Charter) and, as a consequence, the deficiency assessments made by FDIC were improper and erroneous. After consolidation and assessment, the Regional Trial Court settled in favor of Citibank and BA, which was affirmed by the Court of Appeals. ISSUE: The question is whether or not the funds transferred from the head office and international branches to the Philippine branch are insurable or assessable deposits subject to insurance premiums assessments under the Philippine Deposit Insurance Corporation with the errors of money placements in dollar deposits. DECISION: The Court ruled in favor of both Citibank and Bank of America stating that a branch has no separate legal personality. Even if the PDIC argued that the head offices of both banks are separate entities, insisting that the principal agent relationship is in the same jurisdiction, they were not able to push through with their dispute. In response to this, the respondents retaliated that the transfer funds happened in the books of account of the respective branches in their own head office which were located in the United States. In result to this, the Regional Trial Court adjourned the appeal because the sum of money in dollars is payable outside the Philippines, which is not under the deposit pursuant to Section 3(f) of the Philippine Deposit Insurance Corporation.Republic of the Philippines Supreme Court Manila FIRST DIVISION NOTICE Sirs/Mesdames: Please take notice that the Court, First Division, issued a Resolution dated February 19, 2020 which reads as follows: "G.R. No. 219909 - (Philippine Deposit Insurance Corporation v. Gilbert Dizon & Aileen Uy) Respondents Gilbert Dizon and Aileen Uy are the owners of a joint savings account (SA No. 5199-020878-5) with GMA Rural Bank of Cavite, Inc. which they opened sometime in October 2010.' On February 3, 2011, the Bangko Sentral ng Pilipinas, through its Monetary Board issued a Resolution ordering the closure of GMA Bank and its receivership under petitioner Philippine Deposit Insurance Corporation (PDIC). Eventually, on September 29, 2011, the Monetary Board ordered GMA bank's liquidation, with petitioner as liquidator. Due to GMA Bank's closure, petitioners separately filed their claims for insurance with petitioner relative to SA No. 5199-020878- 5 . Petitioner denied the claims through letters both dated February 24, 2012,* viz: Please be informed that based on verification/examination of available bank records, credits made to your account represent payment of BILLS PAYABLE expense. Said expense is an ordinary liability of the bank and does not fall within the meaning of deposit pursuant to Section 4 (f) of R.A. 3591, as amended (The PDIC Charter), which provides that: Rollo, pp. 31-32. 2 Id. at 32. 3 Id. 4 Id. at 61-62. - over - seven (7) pages ... 74RESOLUTION 2 G.R. No. 219909 February 19, 2020 \"...The term 'deposit' means the unpaid balance of money or its equivalent received by a bank in the usual course of business. . .\" XXX XXX XXX Respondents submitted their requests for reconsideration.5 Through Letter6 dated July 11, 2012, petitioner required respondents to submit additional documents7 to support their requests, otherwise, reconsideration is deemed to have been denied. Respondents, however, failed to submit the same. Court of Appeals' Ruling By Decision8 dated February 11, 2015, the Court of Appeals ruled in favor of respondents and ordered petitioner to honor respondents' claim for deposit insurance, viz: WHEREFORE, premises considered, the petition is hereby GRANTED. The order of respondent PDIC, through the challenged Letters, is NULLIFIED and SET ASIDE. Accordingly, respondent PDlC is directed to pay and satisfy the insurance claims of petitioners relative to their GMA Bank Savings Account No. 5199n020878-5. SO ORDERED. It held that respondents sufficiently established that they have an existing deposit - within the denition of the term under Section 4 (f) of RA 35919 with GMA Bank at the time of its closure, and that 5 Id. at 63 -66. '5 Id. at 67. 7 For check deposit: - Original and microlm copy (from and back) of the negotiated check which funded the deposit; and I Certication from the Bank where said check was deposited stating that the same was eventually encashed in favor of GMARBCI For cash deposit: I Original validated GMARBCI'S deposit slip or certied photocopy of ofcial receipt or other documents showing inow of funds to the bank; and I Statement under oath of the former GMARBCl's ofcen'employee stating the following: o I personally received the amount deposited for the above deposit account; and o In the event that payment is made to said account by FDIC, I will be held liable to any person who may be prejudiced by my representations, in addition to other liabilities, civil or criminal that may arise there'om and further undertake to refund the amount paid including interested thereon, and indemnify PDIC of any losses or damages occasioned by such payment. " Penned by Now Supreme Court Associate Justice Samuel H. Gaerlan and Associate Justices Norrnandie B. Pizarro and Zenaida T. Galapate-Laguilles; roilo, pp. 31-39. 9 Section 4. f. The term \"deposit\" means the unpaid balance of money or its equivalent received by a bank in the usual course of business and for which it has given or is obliged to give credit to a commercial, checking, savings, time or thri account, or issued in accordance with Bangko Sean-at rules and regulations and other applicable laws, together with such other obligations of a bank. which, consistent with banking usage and practices, the Board of Directors shall determine and prescribe by regulations to be deposit liabilities of the bank: Provided, That any obligation - over - 74 RESOLUTION 3 GR. No. 219909 February 19, 2020 said deposit does not fall under any of the instances10 where petitioner may validly refuse payment of a deposit insurance. \" Respondents presented their passbook for SA No. 5199- 020878-5 showing that a deposit of One Million Five Hundred Thousand Pesos (151,500,00000) was received by GMA Bank on October 4, 2010. The passbook also contained entries of the interests received by respondents on their deposit.12 In contrast, petitioner's denial of respondents' claim for insurance was solely founded on four (4) promissory notes allegedly evidencing a loan transaction between the parties. Except for one,13 the promissory notes lacked the signatures of the authorized signatories of GMA Bank.l4 More, the entries in respondents' passbook enjoy the presumption of regularity for they were made in the regular course of GMA Bank's business. They are prima facie proof of what are stated therein the date of the transactions, the amounts deposited or withdrawn, and the outstanding balances.\" No evidence was presented to controvert the evidentiary weight of respondents' passbook. By Resolution\"5 dated July 22, 2015, petitioner's motion for reconsideration was denied. The Present Petition Petitioner now seeks afnnative relief from the Court and prays that the assailed dispositions of the Court of Appeals be reversed. of a bank which is payable at the ofce of the bank located outside of the Philippines shall not be a deposit for any of the purposes of this Act or included as part of the total deposits or of insured deposit: Provided, further, That, subject to the approval of the Board of Directors, any insured bank which is incorporated under the laws of the Philippines which maintains a branch outside the Philippines may elect to include for insurance its deposit obligations payable only at such branch. '0 The Corporation shall not pay deposit insurance for the following accounts or transactions, whether denominated, documented, recorded or booked as deposit by the bank: 1. Investment products such as bonds and securities, trust accounts, and other similar instruments; 2. Deposit accounts or transactions which are unfunded, or that are ctitious or fraudulent; 3. Deposit accounts or transactions constituting, andfor emanating from, unsafe and unsound banking practice/s, as determined by the Corporation, in consultation with the BSP, aer clue notice and hearing, and publication of a cease and desist order issued by the Corporation against such deposit accounts or transactions; and 4. Deposits that are determined to be the proceeds of an uniawil activity as dened under Republic Act 9160, as amended. \" Rollo, p. 36. '2 Id. at 60. '3 Promissory Note No. 2363; rails, 13. 57. 1\" 1d at 36. '5 1d at 37. \"5 Id. at 48. - over - '74 RESOLUTION 4 GR. No. 219909 February 19, 2020 Petitioner essentially argues that upon examination, it was disc0vered that respondents' joint savings account originated from \"bills payable\" due to petitioners. Thus, it must be considered as an ordinary obligation of the liquidated bank and not a deposit subject to deposit insurance. To entitle a deposit to payment of deposit insurance, the bank should receive money or its equivalent in the usual course of business. Here, GMA Bank borrowed Pl,500,000.00 from respondents which was rolled over several times as evidenced by Promissory Note Nos. 2470, 23 63 and 2467, with maturity dates July 5, 2010, August 4, 2010 and September 3, 2010, respectively. Upon maturity of the last promissory note (Promissory Note No. 4918 with maturity date October 4, 2010), GMA Bank, instead of paying its loan obligation, opened respondents' SA No. 5199-020878-5 with a balance of F1,500,000.00. Therefore, respondents' savings account is not a bank deposit but supposedly GMA Bank's payment of its loan to respondents. BSP Report of Examination shows that as of December 31, 2009 or less than a year prior to opening of SA No. 5199-020878- 5, GMA Bank was already facing serious capital deciency problems. Therefore, at the time SA No. 5199-020878-5 was opened, the same was unfunded.\" On the other hand, respondents basically riposte that on October 4, 2010, they made an initial deposit of Pl,500,000.00 with GMA Bank as evidenced by their passbook for SA No. 5199-020878- 5.18 They opened their deposit with valuable consideration and GMA Bank received the same in the regular course of its business. Whether GMA Bank used respondents' money for other purposes is immaterial to the claim for deposit insurance because respondents never had any knowledge of the inappropriate use of their deposit nor consented to or authorized such inappropriate use. The additional documents PDIC directed them to submit to support their insurance claim were impossible to obtain. Inasmuch as GMA Bank is now under the PDIC's own control, the latter has the documents it needs to determine the legitimacy of respondents' claim. Lastly, PDIC did not reveal the manner by which it purportedly veried respondents' saving account records, the documents examined and the justication for its conclusion that the joint savings account was a bills payable expense of GMA Bank. '7 M at 18. \"Id. at 65. - OVEI' - 74 RESOLUTION 5 GR. No. 219909 February 19, 2020 Issue Did the Court of Appeals err in ruling that respondents are entitled to deposit insurance? Ruling We DENY the petition. Section 4 of Republic Act No. 3591, otherwise known as the PDIC Charter, denes deposit as the unpaid balance of money or its equivalent received by a bank in the usual course of business and for which it has given or is obliged to give credit to a commercial, checking, savings, time or thrift account, or issued in accordance with Bangko Sentral rules and regulations and other applicable laws, together with such other obligations of a bank, which, consistent with banking usage and practices, the Board of Directors shall determine and prescribe by regulations to be deposit liabilities of the bank.19 Here, records show that respondents deposited with GMA Bank Fl,500,000.00 under SA No. 5199-020878-5 as evidenced by a passbook which respondents submitted to PDIC in support of their claim for deposit insurance. Land Bank of the Philippines v. Oiitn'e20 enunciates that entries in the passbook are primafacie proof of what are stated therein the dates of the transactions, the amounts deposited or withdrawn, and the outstanding balances. It is therefore, incumbent upon PDIC to prove that the deposit account in issue was irregularly made i. e. the savings account being unfunded or the creation of the savings account was without any consideration. This, PDIC failed to do. In Philippine Deposit Insurance Corporation v. Court of Appeals,\" the Court decreed that the fact that no actual money in bills and/or coins was handed by respondents to the insured bank does not mean that the transactions on the new Golden Time Deposits (GTDs) did not involve money and that there was no consideration therefor. Too, PDIC's failure to overcome the presumption that the GTDs were made in the regular course of business entitled respondents to deposit insurance, thus: For the outstanding balance of respondents' 71 GTDs in Manila Banking Corporation (MBC) prior to May 26, 1987 in the [9 Section 4, RA 359i. 20 724 Phil. 564, 591-592 (2014). 21450 Phil. 233, 241-242 (2003). RESOLUTION 6 GR. No. 219909 February 19, 2020 amount of ?1,115,889.15 as earlier mentioned was re-deposited by respondents under 28 new GTDs. Admittedly, MBC had 132,841,71190 cash on hand more than double the outstanding balance of respondents' 71 GTDs 7 at the start of the banking day on May 25, 1987. Since respondent Jose Abad was at MBC soon after it opened at 9:00 am. of that day, petitioner should not presume that MBC had no cash to cover the new GTDs of respondents and conclude that there was no consideration for said GTDs. Petitioner having failed to overcome the presumption that the ordinary course of business was followed, this Court nds that the 28 new GTDs were deposited "in the usual course of business" of MBC. As liquidator of GMA Bank, PDIC has access to all documents relative to the bank's business and transactions, including pertinent bank records of the alleged loan and payment-throughdeposit transactions between respondents and GMA Bank. It should have presented credible documents that GMA Bank did not, in fact, receive any amount for the opening of respondents' savings account to justify denial of their claim for deposit insurance. Too, PDIC. did not, as it could not, deny that the passbook submitted by respondents is an authentic and legitimate document. The opening of the said savings account enjoys the presumption that the same was opened in the ordinary course of business, hence, must be paid. All told, the Court of Appeals did not err in directing PDIC to pay respondents' claim for deposit insurance relative to SA No. 5199- 020878-5. SO ORDERED.\" Very truly yours, LIBRA . BUENA Divis'o Clerk of CourtgftahL 74

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance