Answered step by step

Verified Expert Solution

Question

1 Approved Answer

This is the question. This is the case. These are accounting standards. First picture is the question, next two are case study. Read the case

This is the question.

This is the case.

These are accounting standards.

First picture is the question, next two are case study. Read the case study and answer the question. I need it ASAP.

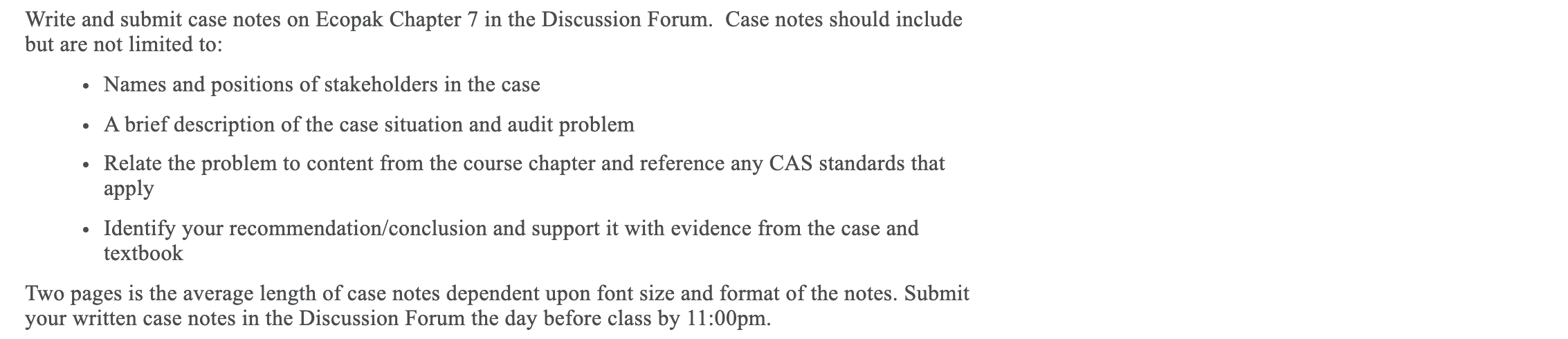

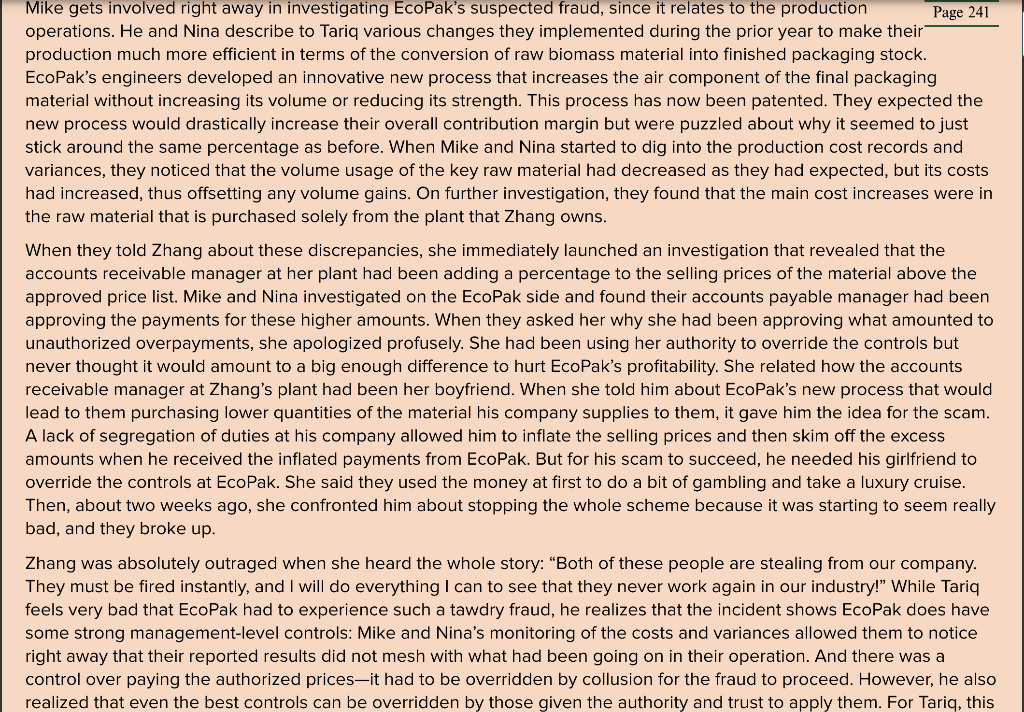

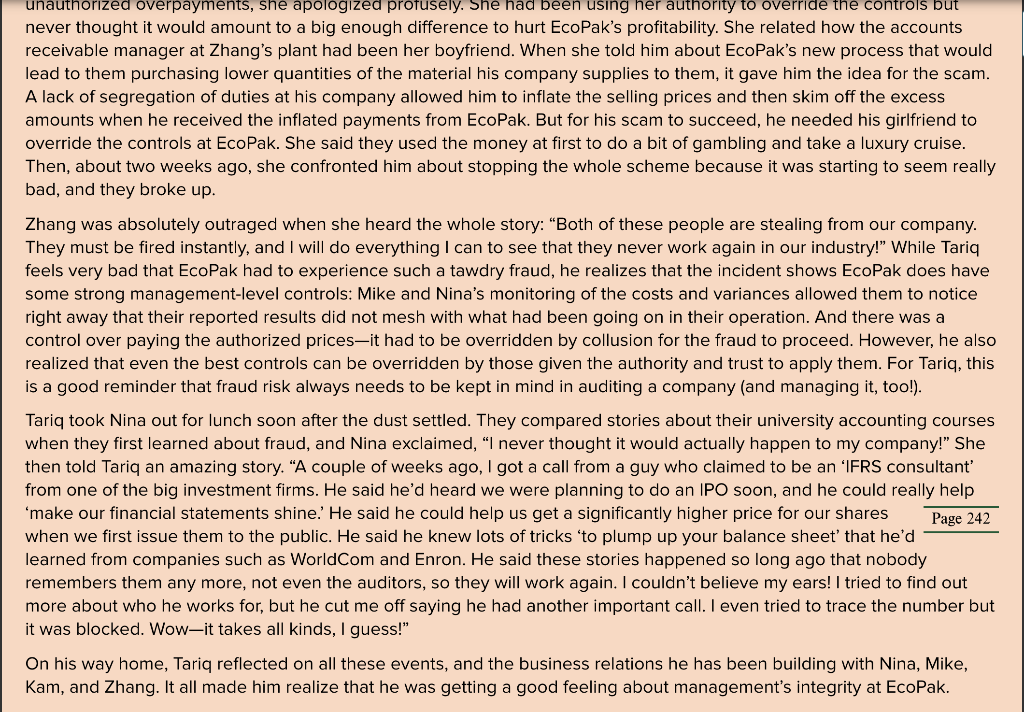

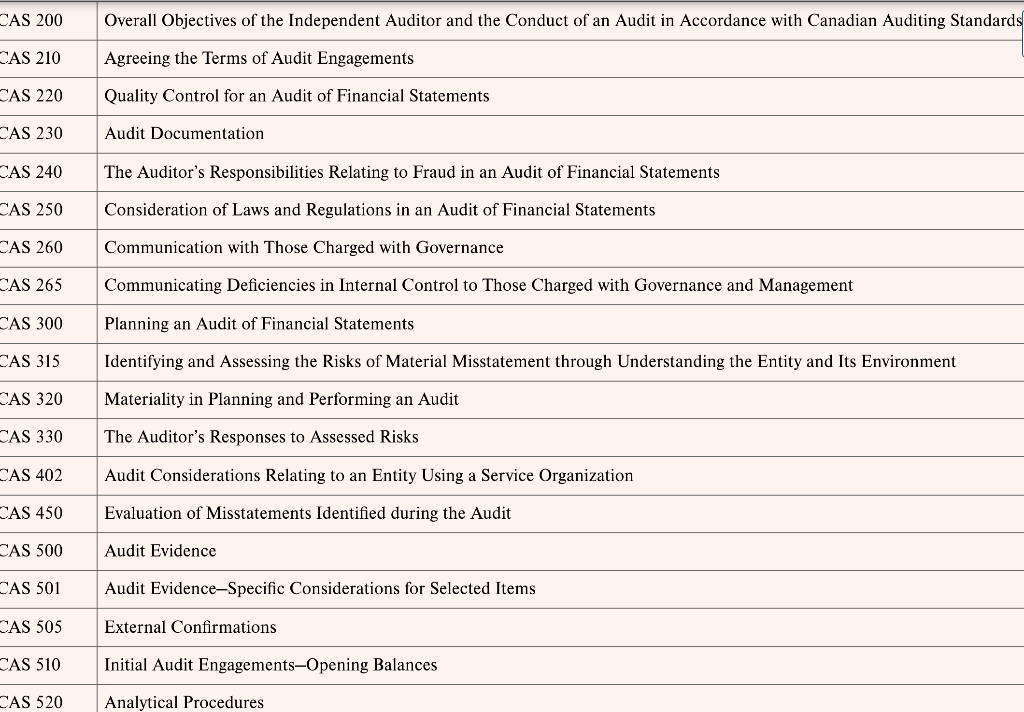

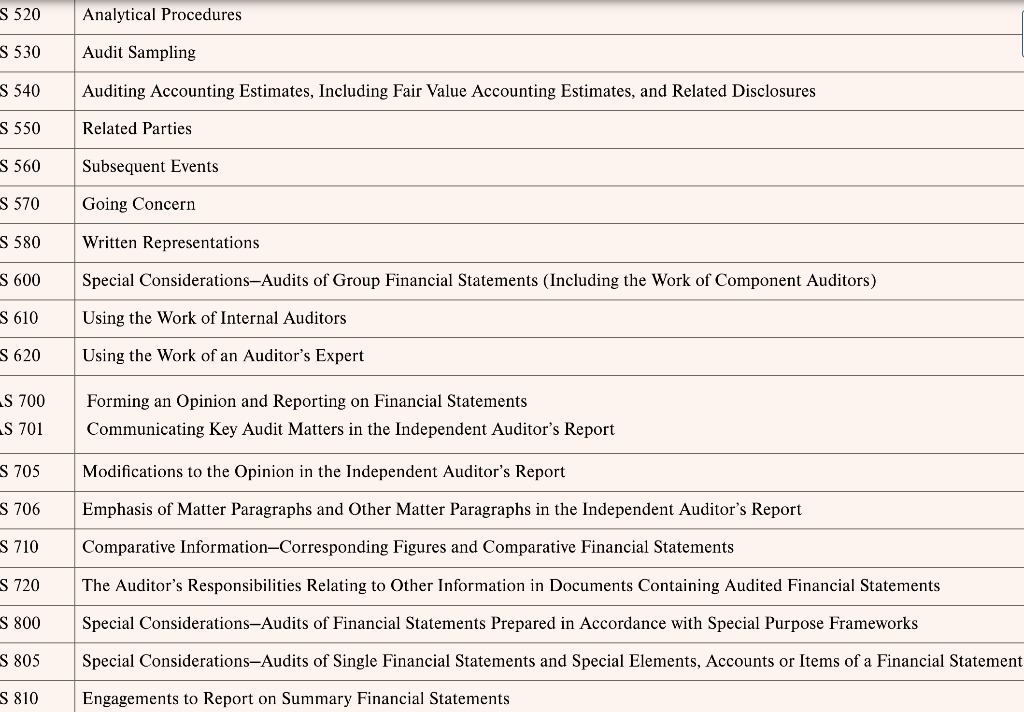

. Write and submit case notes on Ecopak Chapter 7 in the Discussion Forum. Case notes should include but are not limited to: Names and positions of stakeholders in the case A brief description of the case situation and audit problem Relate the problem to content from the course chapter and reference any CAS standards that apply Identify your recommendation/conclusion and support it with evidence from the case and textbook . Two pages is the average length of case notes dependent upon font size and format of the notes. Submit your written case notes in the Discussion Forum the day before class by 11:00pm. Mike gets involved right away in investigating EcoPak's suspected fraud, since it relates to the production Page 241 operations. He and Nina describe to Tariq various changes they implemented during the prior year to make their production much more efficient in terms of the conversion of raw biomass material into finished packaging stock. EcoPak's engineers developed an innovative new process that increases the air component of the final packaging material without increasing its volume or reducing its strength. This process has now been patented. They expected the new process would drastically increase their overall contribution margin but were puzzled about why it seemed to just stick around the same percentage as before. When Mike and Nina started to dig into the production cost records and variances, they noticed that the volume usage of the key raw material had decreased as they had expected, but its costs had increased, thus offsetting any volume gains. On further investigation, they found that the main cost increases were in the raw material that is purchased solely from the plant that Zhang owns. When they told Zhang about these discrepancies, she immediately launched an investigation that revealed that the accounts receivable manager at her plant had been adding a percentage to the selling prices of the material above the approved price list. Mike and Nina investigated on the EcoPak side and found their accounts payable manager had been approving the payments for these higher amounts. When they asked her why she had been approving what amounted to unauthorized overpayments, she apologized profusely. She had been using her authority to override the controls but never thought it would amount to a big enough difference to hurt EcoPak's profitability. She related how the accounts receivable manager at Zhang's plant had been her boyfriend. When she told him about EcoPak's new process that would lead to them purchasing lower quantities of the material his company supplies to them, it gave him the idea for the scam. A lack of segregation of duties at his company allowed him to inflate the selling prices and then skim off the excess amounts when he received the inflated payments from EcoPak. But for his scam to succeed, he needed his girlfriend to override the controls at EcoPak. She said they used the money at first to do a bit of gambling and take a luxury cruise. Then, about two weeks ago, she confronted him about stopping the whole scheme because it was starting to seem really bad, and they broke up. Zhang was absolutely outraged when she heard the whole story: "Both of these people are stealing from our company. They must be fired instantly, and I will do everything I can to see that they never work again in our industry!" While Tariq feels very bad that EcoPak had to experience such a tawdry fraud, he realizes that the incident shows EcoPak does have some strong management-level controls: Mike and Nina's monitoring of the costs and variances allowed them to notice right away that their reported results did not mesh with what had been going on in their operation. And there was a control over paying the authorized pricesit had to be overridden by collusion for the fraud to proceed. However, he also realized that even the best controls can be overridden by those given the authority and trust to apply them. For Tariq, this unauthorized overpayments, she apologized profusely. She had been using her authority to override the controls but never thought it would amount to a big enough difference to hurt EcoPak's profitability. She related how the accounts receivable manager at Zhang's plant had been her boyfriend. When she told him about EcoPak's new process that would lead to them purchasing lower quantities of the material his company supplies to them, it gave him the idea for the scam. A lack of segregation of duties at his company allowed him to inflate the selling prices and then skim off the excess amounts when he received the inflated payments from EcoPak. But for his scam to succeed, he needed his girlfriend to override the controls at EcoPak. She said they used the money at first to do a bit of gambling and take a luxury cruise. Then, about two weeks ago, she confronted him about stopping the whole scheme because it was starting to seem really bad, and they broke up. Zhang was absolutely outraged when she heard the whole story: "Both of these people are stealing from our company. They must be fired instantly, and I will do everything I can to see that they never work again in our industry!" While Tariq feels very bad that EcoPak had to experience such a tawdry fraud, he realizes that the incident shows EcoPak does have some strong management-level controls: Mike and Nina's monitoring of the costs and variances allowed them to notice right away that their reported results did not mesh with what had been going on in their operation. And there was a control over paying the authorized pricesit had to be overridden by collusion for the fraud to proceed. However, he also realized that even the best controls can be overridden by those given the authority and trust to apply them. For Tariq, this is a good reminder that fraud risk always needs to be kept in mind in auditing a company (and managing it, too!). Tariq took Nina out for lunch soon after the dust settled. They compared stories about their university accounting courses when they first learned about fraud, and Nina exclaimed, I never thought it would actually happen to my company!" She then told Tariq an amazing story. A couple of weeks ago, I got a call from a guy who claimed to be an IFRS consultant from one of the big investment firms. He said he'd heard we were planning to do an IPO soon, and he could really help 'make our financial statements shine.' He said he could help us get a significantly higher price for our shares Page 242 when we first issue them to the public. He said he knew lots of tricks 'to plump up your balance sheet' that he'd learned from companies such as WorldCom and Enron. He said these stories happened so long ago that nobody remembers them any more, not even the auditors, so they will work again. I couldn't believe my ears! I tried to find out more about who he works for, but he cut me off saying he had another important call. I even tried to trace the number but it was blocked. Wow-it takes all kinds, I guess!" On his way home, Tariq reflected on all these events, and the business relations he has been building with Nina, Mike, Kam, and Zhang. It all made him realize that he was getting a good feeling about management's integrity at EcoPak. CAS 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with Canadian Auditing Standards CAS 210 Agreeing the Terms of Audit Engagements CAS 220 Quality Control for an Audit of Financial Statements CAS 230 Audit Documentation CAS 240 The Auditor's Responsibilities Relating to Fraud in an Audit of Financial Statements CAS 250 Consideration of Laws and Regulations in an Audit of Financial Statements SAS 260 Communication with Those Charged with Governance CAS 265 Communicating Deficiencies in Internal Control to Those Charged with Governance and Management SAS 300 Planning an Audit of Financial Statements CAS 315 Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment CAS 320 Materiality in Planning and Performing an Audit SAS 330 The Auditor's Responses to Assessed Risks CAS 402 Audit Considerations Relating to an Entity Using a Service Organization CAS 450 Evaluation of Misstatements Identified during the Audit SAS 500 Audit Evidence CAS 501 Audit Evidence-Specific Considerations for Selected Items CAS 505 External Confirmations CAS 510 Initial Audit Engagements-Opening Balances CAS 520 Analytical Procedures S 520 Analytical Procedures S 530 Audit Sampling S 540 Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures S 550 Related Parties S 560 Subsequent Events S 570 Going Concern S 580 Written Representations S 600 Special Considerations-Audits of Group Financial Statements (Including the work of Component Auditors) S 610 Using the work of Internal Auditors S 620 Using the work of an Auditor's Expert S 700 S 701 Forming an Opinion and Reporting on Financial Statements Communicating Key Audit Matters in the Independent Auditor's Report S 705 Modifications to the Opinion in the Independent Auditor's Report S 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor's Report S 710 Comparative Information-Corresponding Figures and Comparative Financial Statements S 720 The Auditor's Responsibilities Relating to Other Information in Documents Containing Audited Financial Statements S 800 Special Considerations-Audits of Financial Statements Prepared in Accordance with Special Purpose Frameworks S 805 Special Considerations-Audits of Single Financial Statements and Special Elements, Accounts or Items of a Financial Statement S 810 Engagements to Report on Summary Financial StatementsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting And Finance An Introduction

Authors: Eddie McLaney, Peter Atrill

10th Edition

1292312262, 978-1292312262