Answered step by step

Verified Expert Solution

Question

1 Approved Answer

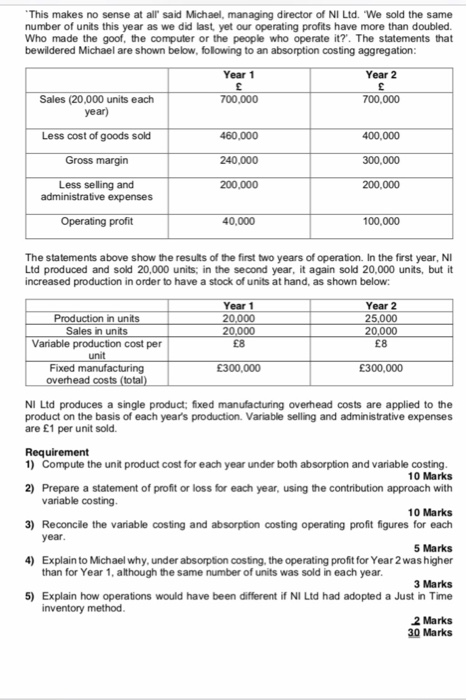

This makes no sense at all said Michael, managing director of NI Ltd. We sold the same number of units this year as we did

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Plant Auditing A Powerful Tool For Improving Metallurgical Plant Performance

Authors: Deepak Malhotra

1st Edition

0873354125, 978-0873354127