Question: (3) Review Note 5 required you to test the operating effectiveness of an internal control (ensuring appropriate approval of write-offs). To which financial statement assertion

(3) Review Note 5 required you to test the operating effectiveness of an internal control (ensuring appropriate approval of

write-offs). To which financial statement assertion does this internal control relate most closely? Based on the evidence

you gathered, and considering the Audit Risk Model, would you recommend that your audit team revise the audit

plan? If so, which risks in the Audit Risk Model would change and how (increase/decrease)? How might you respond

to the changes in these risk(s)?

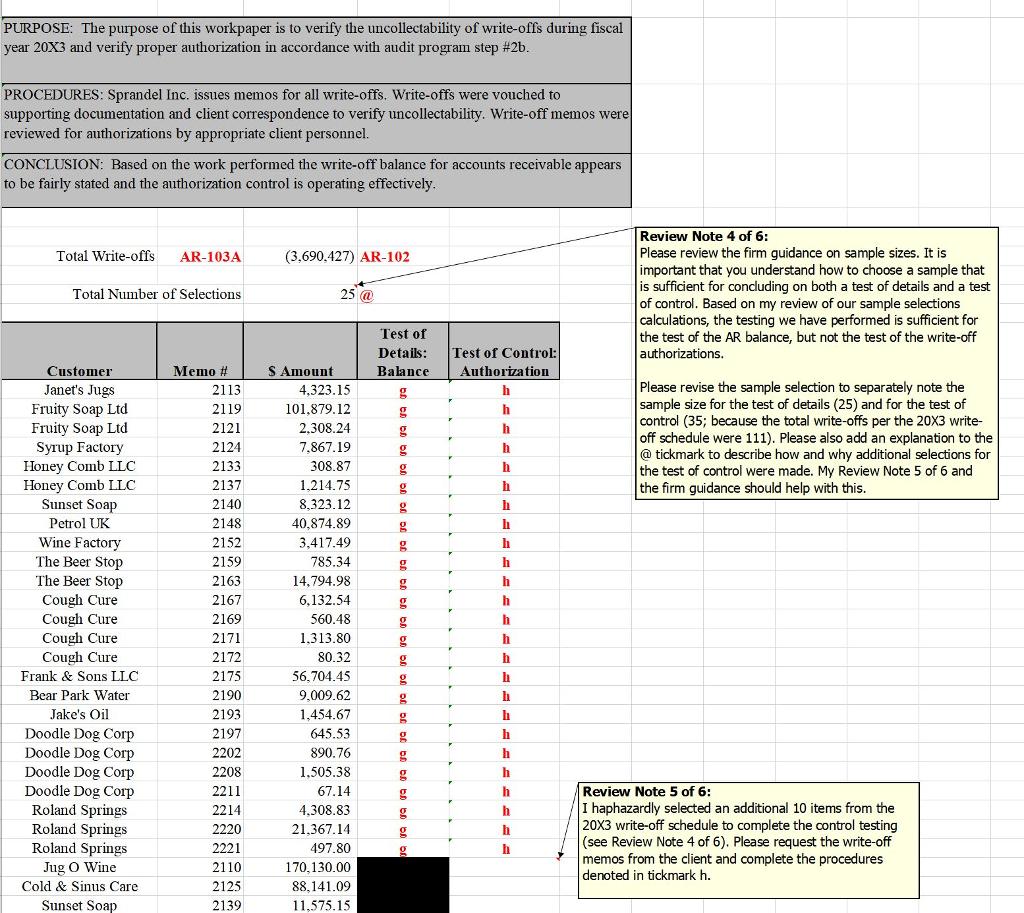

Review Note 5 of 6:

I haphazardly selected an additional 10 items from the 20X3 write-off schedule to complete the control testing (see Review Note 4 of 6). Please request the write-off memos from the client and complete the procedures denoted in tickmark h.

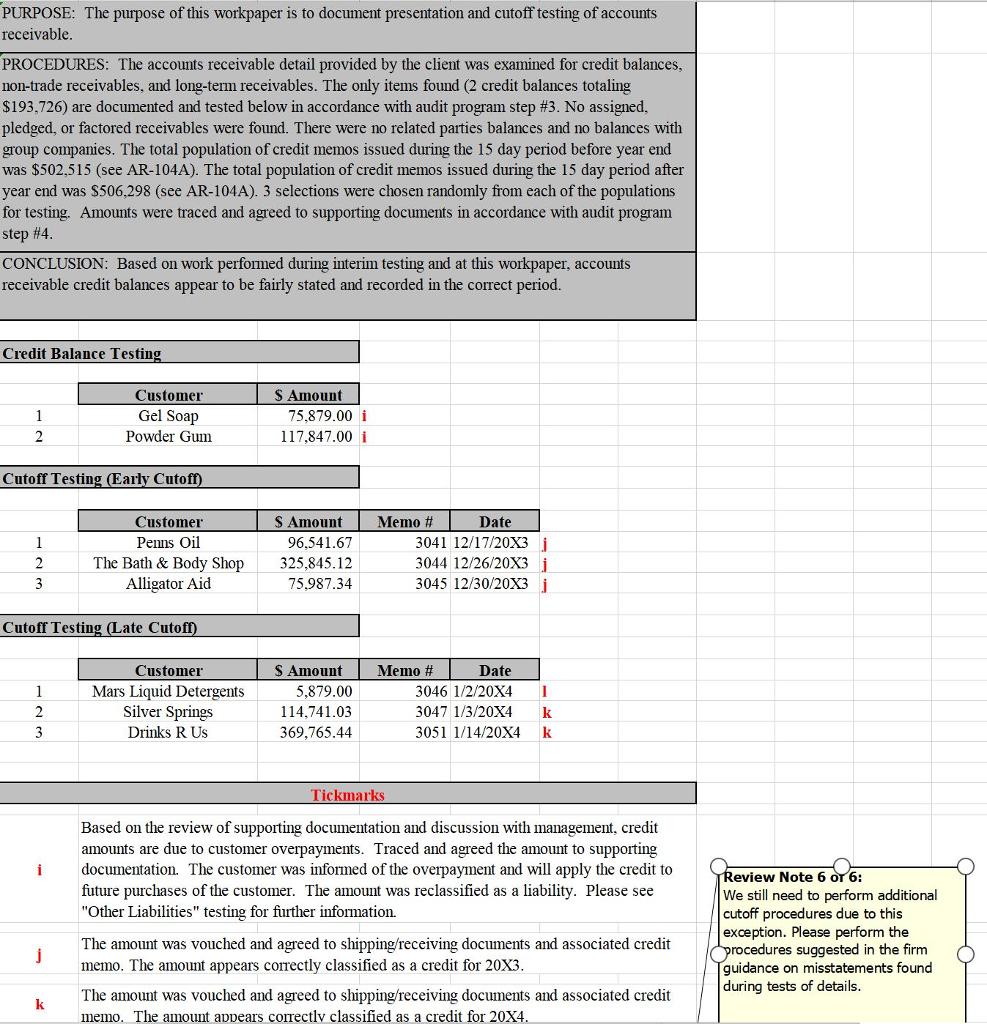

(4) Review Note 6 related to an exception found during cutoff testing and the required additional procedures to be

performed. Based on this exception and the additional procedures you performed, discuss the implications. Consider

the following in your discussion:

a. which financial statement assertion this audit work most closely relates to,

b. the total dollar amount of the exception(s) based on the testing performed,

c. the effect of the exception(s) on the accounts receivable balance (understatement or overstatement) in the current

year (12/31/20X3) and next year (i.e., 12/31/20X4) if not adjusted, and

d. the appropriate auditor response to the exception(s).

Review Note 6 of 6:

We still need to perform additional cutoff procedures due to this exception. Please perform the procedures suggested in the firm guidance on misstatements found during tests of details.

(5) Using PCAOB AS 1215, paragraphs 8 and 12, describe the auditor's responsibilities for documenting information

related to significant findings or issues inconsistent with the auditor's conclusions and three factors that would indicate

a finding or issue is significant. Would you deem any of the issues/exceptions that you noted during your audit work to

be significant?

PURPOSE: The purpose of this workpaper is to verify the uncollectability of write-offs during fiscal year 20X3 and verify proper authorization in accordance with audit program step #2b. PROCEDURES: Sprandel Inc. issues memos for all write-offs. Write-offs were vouched to supporting documentation and client correspondence to verify uncollectability. Write-off memos were reviewed for authorizations by appropriate client personnel. CONCLUSION: Based on the work performed the write-off balance for accounts receivable appears to be fairly stated and the authorization control is operating effectively. Total Write-offs Total Number of Selections Customer Janet's Jugs Fruity Soap Ltd Fruity Soap Ltd Syrup Factory Honey Comb LLC Honey Comb LLC Sunset Soap Petrol UK Wine Factory The Beer Stop The Beer Stop Cough Cure Cough Cure Cough Cure Cough Cure Frank & Sons LLC Bear Park Water Jake's Oil Doodle Dog Corp Doodle Dog Corp Doodle Dog Corp Doodle Dog Corp AR-103A Roland Springs Roland Springs Roland Springs Jug O Wine Cold & Sinus Care Sunset Soap Memo # 2113 2119 2121 2124 2133 2137 2140 2148 2152 2159 2163 2167 2169 2171 2172 2175 2190 2193 2197 2202 2208 2211 2214 2220 2221 2110 2125 2139 (3,690,427) AR-102 $ Amount 25 @ 4,323.15 101,879.12 2,308.24 7,867.19 308.87 1,214.75 8,323.12 40,874.89 3,417.49 785.34 14,794.98 6,132.54 560.48 1,313.80 80.32 56,704.45 9,009.62 1,454.67 645.53 890.76 1,505.38 67.14 4.308.83 21,367.14 497.80 170,130.00 88,141.09 11.575.15 Test of Details: Balance g g g g g g g g g g g g g g g g g g g g g g g 9 Test of Control: Authorization h h h F F F Y Y F K Y 7 F h h h h h h h h h h h h h h h h h h h h h h Review Note 4 of 6: Please review the firm guidance on sample sizes. It is important that you understand how to choose a sample that is sufficient for concluding on both a test of details and a test of control. Based on my review of our sample selections calculations, the testing we have performed is sufficient for the test of the AR balance, but not the test of the write-off authorizations. Please revise the sample selection to separately note the sample size for the test of details (25) and for the test of control (35; because the total write-offs per the 20X3 write- off schedule were 111). Please also add an explanation to the @tickmark to describe how and why additional selections for the test of control were made. My Review Note 5 of 6 and the firm guidance should help with this. Review Note 5 of 6: I haphazardly selected an additional 10 items from the 20X3 write-off schedule to complete the control testing (see Review Note 4 of 6). Please request the write-off memos from the client and complete the procedures denoted in tickmark h.

Step by Step Solution

3.51 Rating (154 Votes )

There are 3 Steps involved in it

PURPOSE The purpose of this workpaper is to verify the uncollectability of writeoffs during fiscal year 20X3 and verify proper authorization in accordance with audit program step 2b PROCEDURES Sprande... View full answer

Get step-by-step solutions from verified subject matter experts