Question

This next question is about floating rate bonds and it tests your ability to value a series of cash flows in a situation you havent

This next question is about floating rate bonds and it tests your ability to value a series of cash flows in a situation you havent seen before. The question might take you a little longer than the 7 marks suggest, because you need to think carefully. The actual work uses basic valuation methods you have used before.

As noted in lecture, floating-rate bonds have coupons that adjust right after each coupon payment to reflect the current interest rate, but once the coupon is set, it does not change until

(immediately) after the next coupon payment. This has the effect, that the bond reverts to par value right after each coupon payment.

To make sure you are clear about the timing of cash flows, note how they work. If a floating rate bond makes coupon payments twice a year on 31 March and 30 September, on 31 March 2022 the coupon rate is set for the next 6 months say 2% - and on 30 September 2022 you receive the 2% coupon and the next coupon for 30 September 2022 to 31 March 2023 is set at the new (floating) rate say 2.5%. And so on and so forth.

In Australia, floating rates are often tied to the Bank-Bill-Swap Rate (BBSW). The floating rate will be the BBSW rate plus an interest rate spread. Both the BBSW rates and the interest rate spread are calculated using simple interest. If you see a 6-month rate of 6% and a spread of 0.5%. This means the periodic rate, the time to the next coupon or face-value payment, for 6 months is actually (6%+0.5%)*6/12=3.25%. A 5-month rate of 7% translates to a periodic rate for 5 months of (7%+0.5%)5/12=3.125% .

a. What was the annualised interest rate on the floating-rate semi-annual bond 2-months ago?

b. What is the dollar amount of the next semi-annual coupon payment per $100,000 of face value?

c. What is the total cash flow at the next coupon payment if you were to sell the bond immediately after the next coupon payment? (Add together the coupon and the revenue from the sale)

d. What is todays annualised interest rate on the floating-rate semi-annual bond?

e. Whats the value of the bond today?

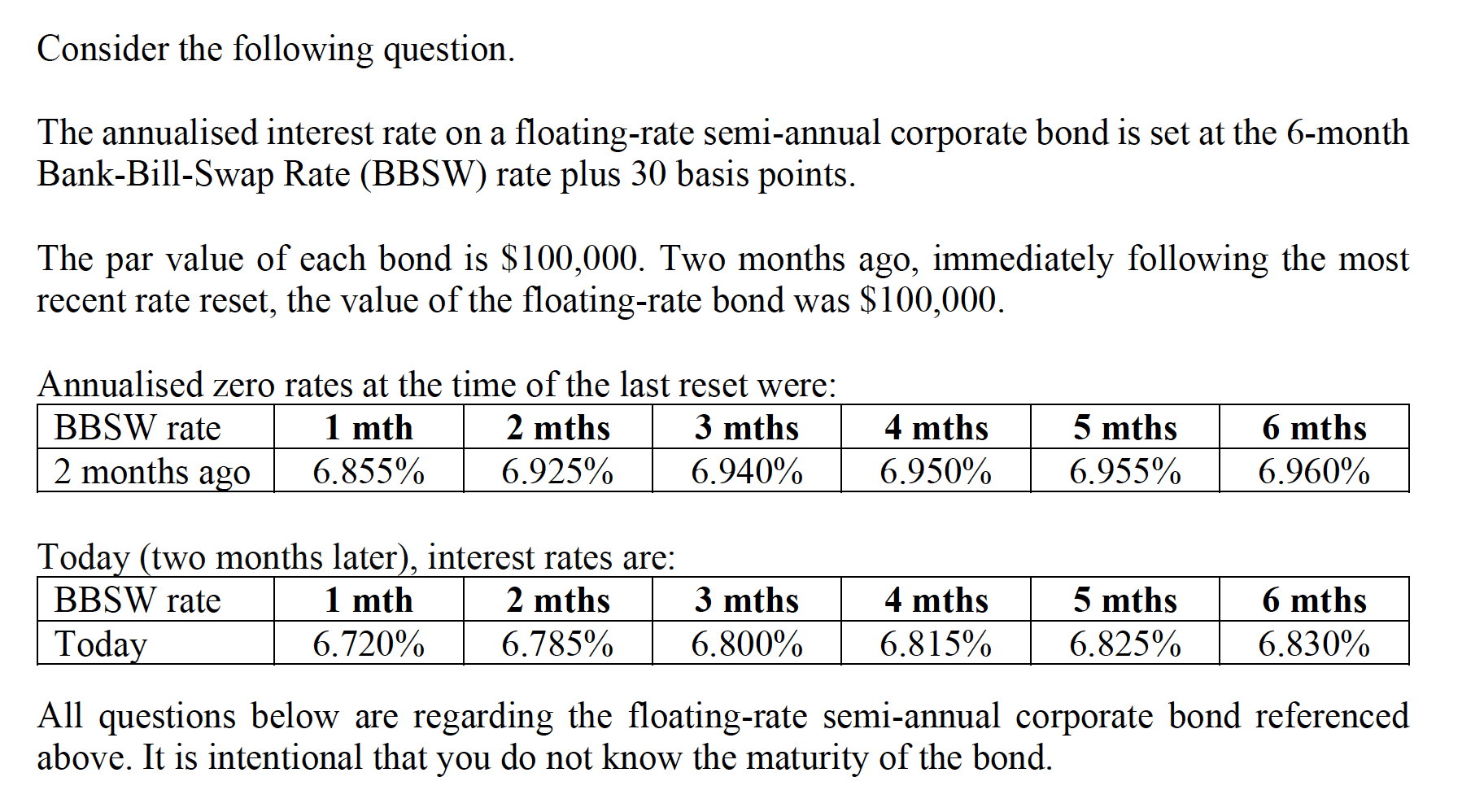

Consider the following question. The annualised interest rate on a floating-rate semi-annual corporate bond is set at the 6-month Bank-Bill-Swap Rate (BBSW) rate plus 30 basis points. The par value of each bond is $100,000. Two months ago, immediately following the most recent rate reset, the value of the floating-rate bond was $100,000. Annualised zero rates at the time of the last reset were: Today (two months later), interest rates are: All questions below are regarding the floating-rate semi-annual corporate bond referenced above. It is intentional that you do not know the maturity of the bond. Consider the following question. The annualised interest rate on a floating-rate semi-annual corporate bond is set at the 6-month Bank-Bill-Swap Rate (BBSW) rate plus 30 basis points. The par value of each bond is $100,000. Two months ago, immediately following the most recent rate reset, the value of the floating-rate bond was $100,000. Annualised zero rates at the time of the last reset were: Today (two months later), interest rates are: All questions below are regarding the floating-rate semi-annual corporate bond referenced above. It is intentional that you do not know the maturity of the bondStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational Finance

Authors: Kirt C. Butler

3rd Edition

0324177453, 978-0324177459