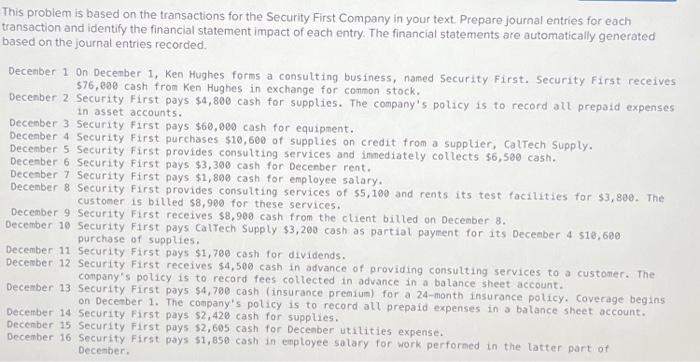

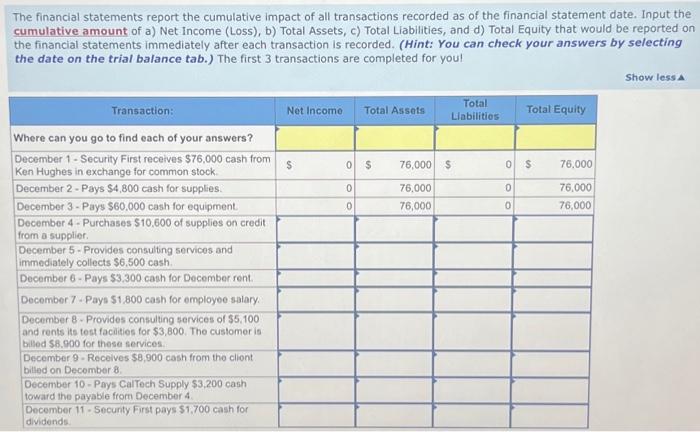

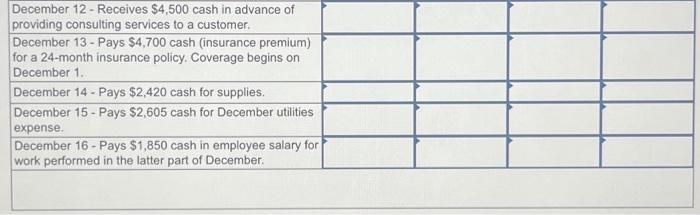

This problem is based on the transactions for the Security First Company in your text. Prepare journal entries for each transaction and identify the financial statement impact of each entry. The financial statements are automatically generated based on the journal entries recorded. December 1 On Decenber 1, Ken Hughes forms a consulting business, named Security First. Security First receives $76,000 cash from Ken Hughes in exchange for common stock. Decenber 2 Security First pays $4,800 cash for supplies. The company's policy is to record all prepaid expenses in asset accounts. Decenber 3 Security First pays $60,000 cash for equipment. Decenber 4 Security First purchases $10,600 of supplies on credit trom a supplier, CalTech Supply. December 5 Security First provides consulting services and innediately collects $6,500 cash. Decenber 6 Security First pays $3,300 cash for Decenber rent. Deceaber 7 Security First pays $1,800 cash for employee salary. December 8 Security First provides consulting services of $5,100 and rents its test facilities for $3,800. The customer is billed $8,900 for these services. Decenber 9 Security First receives $8,900 cash from the client billed on December 8 . December 10 Security First pays CalTech Supply $3,200 cash as partial payment for its December 4$10,600 purchase of supplies. December 11 Security First pays $1,700 cash for dividends. December 12 Security First receives $4,500 cash in advance of providing consulting services to a customer. The company's policy is to recard fees collected in advance in a balance sheet account. Decenber 13 Security First pays $4,700 cash (insurance prealun) for a 24 -month insurance policy. Coverage begins on Decenber 1. The company's policy is to record atl prepaid expenses in a batance sheet account. Decenber 14 Security First pays $2,420 cash for supplies. Decenber 15 Security First pays $2,605 cash for Decenber utitities expense. Decenber 16 Security First pays \$1,850 cash in employee salary for work performed in the latter part of Decenter. The financial statements report the cumulative impact of all transactions recorded as of the financial statement date. Input the cumulative amount of a) Net Income (Loss), b) Total Assets, c) Total Liabilities, and d) Total Equity that would be reported on the financial statements immediately after each transaction is recorded. (Hint: You can check your answers by selecting the date on the trial balance tab.) The first 3 transactions are completed for you! December 12 - Receives $4,500 cash in advance of providing consulting services to a customer. December 13 - Pays $4,700 cash (insurance premium) for a 24-month insurance policy. Coverage begins on December 1. December 14 - Pays $2,420 cash for supplies. December 15 - Pays $2,605 cash for December utilities expense. December 16 - Pays $1,850 cash in employee salary for work performed in the latter part of December