Question: This request is for question P-35. Number 35 uses information from number 34, so it has been included in the pictures. Please only solve number

This request is for question P-35. Number 35 uses information from number 34, so it has been included in the pictures. Please only solve number 35 and NOT number 34. Thank you very much for your effort!

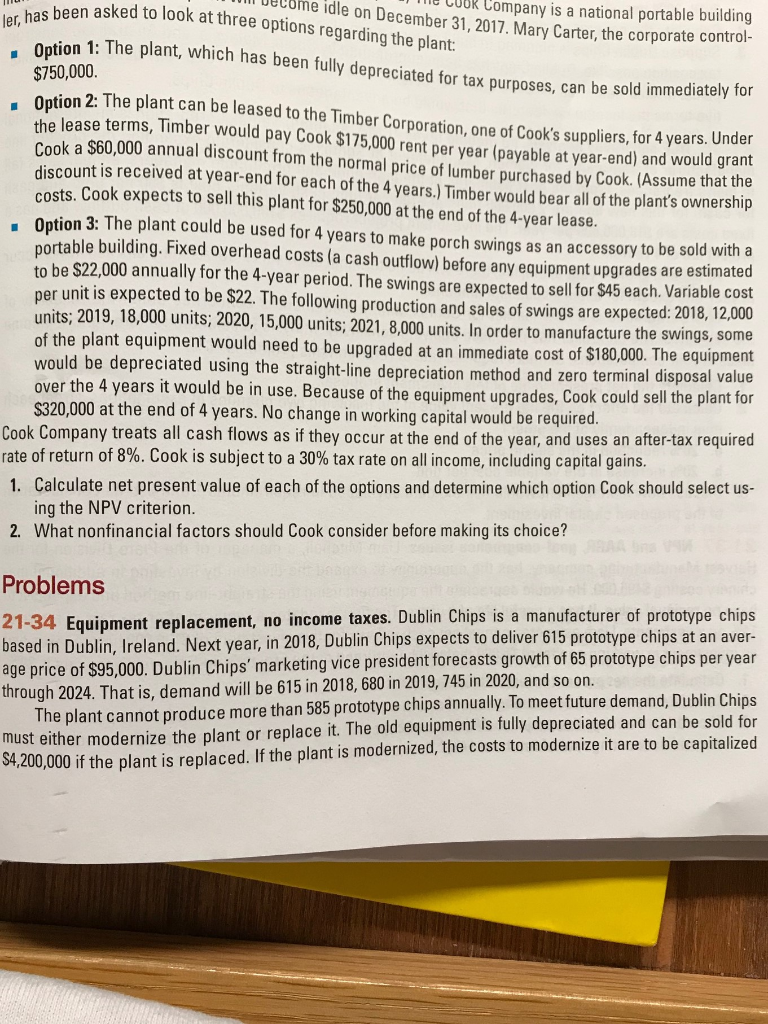

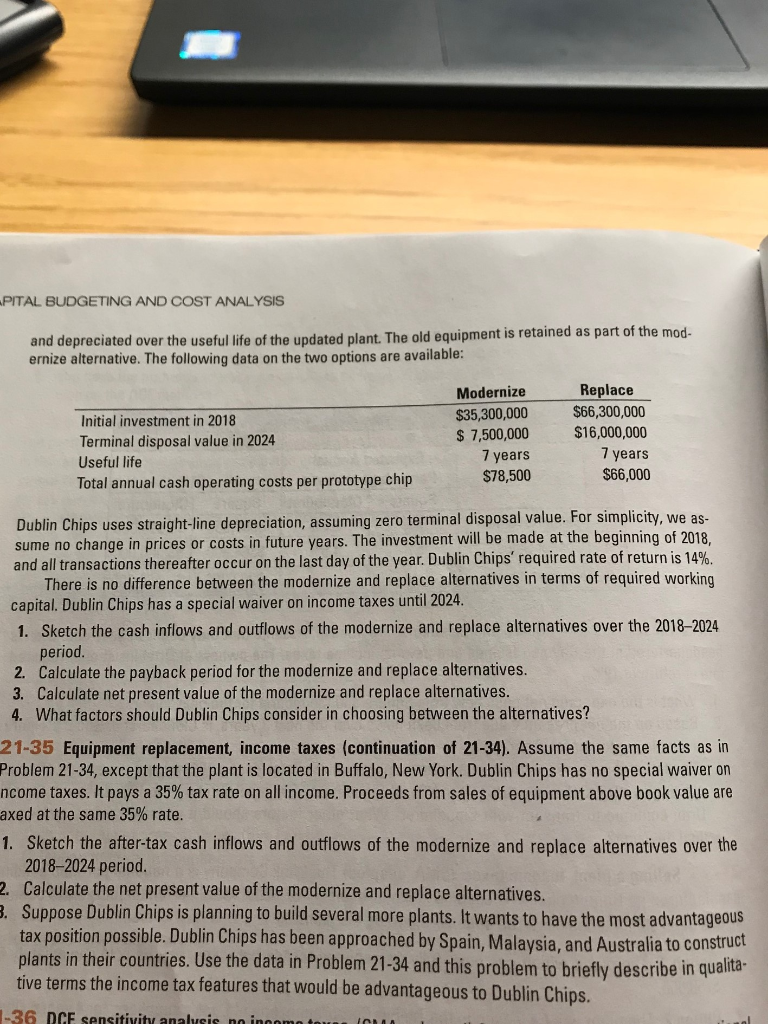

been asked to look at three options regarding the plant uetome idle on Dec CUOR Company is a national portable building , has ember 31, 2017. Mary Carter, the corporate control er Option 1: The plant, which has been fully depreciated for tax $750,000 Option 2: The plant can be leased to the Timber Con purposes, can be sold immediately for se terms, Timber would pay Cook $175,000 rent per year (payable poration, one of Cook's suppliers, for 4 years. Under at year-end) and would grant . (Assume that the Cook a $60,000 annual discount from the normal price of lumber purc discount is received at year-end for each of the 4 years.) Timber would bear all of the plant's ownership costs. Cook expects to sell this plant for $250,000 at the end of the 4-year lease Option 3: The plant could be used for 4 years to make porch swings as an accessory to be sold witha ortable building. Fixed overhead costs (a cash outfilow) before any equipment upgrades are estimated to be $22,000 annually for the 4-year period. The swings are expected to sell for $45 each. Variable cost per unit is expected to be $22. The following production and sales of swings are expected: 2018, 12,000 units; 2019, 18,000 units; 2020, 15,000 units; 2021, 8,000 units. In order to manufacture the swings, some of the plant equipment would need to be upgraded at an immediate cost of $180,000. The equipm would be depreciated using the straight-line depreciation method and zero term over the 4 years it w hased by Cook inal disposal value ould be in use. Because of the equipment upgrades, Cook could sell the plant for 0 at the end of 4 years. No change in working capital would be required Cook Company treats all cash flows as if they occur at the end of the year, and uses an after-tax required rate of return of 8%. Cook is subject to a 30% tax rate on all income, including capital gains Calculate net present value of each of the options and determine which option Cook should select us ing the NPV criterion 1. 2. What nonfinancial factors should Cook consider before making its choi Problems 21-34 Equipment replacement, no income taxes. Dublin Chips is a manufacturer of prototype chips based in Dublin, Ireland. Next year, in 2018, Dublin Chips expects to deliver 615 prototype chips at an aver ge price of $95,000. Dublin Chips' marketing vice president forecasts growth of 65 prototype chip through 2024. That is, demand will be 615 in 2018, 680 in 2019, 745 in 2020, and so on s per year for The plant cannot produce more than 585 prototype chips annually. To meet future demand, Dublin Chips must either modernize the plant or replace it. The old equipment is fully depreciated and can be sold 200,000 if the plant is replaced. If the plant is modernized, the costs to modernize it are to be capitalized PITAL BUDGETING AND COST ANALYSIS of the mod- and depreciated over the useful life of the updated plant. The old equipment is retained as part ernize alternative. The following data on the two options are available Modernize $35,300,000 Replace $66,300,000 Initial investment in 2018 Terminal disposal value in 2024 Useful life Total annual cash operating costs per prototype chip S 7,500,000 $16,000,00 7 years 7 years $78,500 $66,000 Dublin Chips uses straight-line depreciation, assuming zero terminal disposal value. For simplicity, we as sume no change in prices or costs in future years. The investment will be made at the beginning of 2018, and all transactions thereafter occur on the last day of the year. Dublin Chips' required rate of return is 14% There is no difference between the modernize and replace alternatives in terms of required working capital. Dublin Chips has a special waiver on income taxes until 2024 1. Sketch the cash inflows and outflows of the modernize and replace alternatives over the 2018-2024 period. 2. Calculate the payback period for the modernize and replace alternatives. 3. Calculate net present value of the modernize and replace alternatives. 4. What factors should Dublin Chips consider in choosing between the alternatives? 21-35 Equipment replacement, income taxes (continuation of 21-34). Assume the same facts as in Problem 21-34, except that the plant is located in Buffalo, New York. Dublin Chips has no special waiver on ncome taxes. It pays a 35% tax rate on all income. Proceeds from sales of equipment above book value are axed at the same 35% rate 1. Sketch the after-tax cash inflows and outflows of the modernize and replace alternatives over the 2018-2024 period 2. Calculate the net present value of the modernize and replace alternatives. . Suppose Dublin Chips is planning to build several more plants. It wants to have the most advantageous tax position possible. Dublin Chips has been approached by Spain, Malaysia, and Australia to construct plants in their countries. Use the data in Problem 21-34 and this problem to briefly describe in qualita- tive terms the income tax features that would be advantageous to Dublin Chips. -36 DCE sensitivity analusis no in been asked to look at three options regarding the plant uetome idle on Dec CUOR Company is a national portable building , has ember 31, 2017. Mary Carter, the corporate control er Option 1: The plant, which has been fully depreciated for tax $750,000 Option 2: The plant can be leased to the Timber Con purposes, can be sold immediately for se terms, Timber would pay Cook $175,000 rent per year (payable poration, one of Cook's suppliers, for 4 years. Under at year-end) and would grant . (Assume that the Cook a $60,000 annual discount from the normal price of lumber purc discount is received at year-end for each of the 4 years.) Timber would bear all of the plant's ownership costs. Cook expects to sell this plant for $250,000 at the end of the 4-year lease Option 3: The plant could be used for 4 years to make porch swings as an accessory to be sold witha ortable building. Fixed overhead costs (a cash outfilow) before any equipment upgrades are estimated to be $22,000 annually for the 4-year period. The swings are expected to sell for $45 each. Variable cost per unit is expected to be $22. The following production and sales of swings are expected: 2018, 12,000 units; 2019, 18,000 units; 2020, 15,000 units; 2021, 8,000 units. In order to manufacture the swings, some of the plant equipment would need to be upgraded at an immediate cost of $180,000. The equipm would be depreciated using the straight-line depreciation method and zero term over the 4 years it w hased by Cook inal disposal value ould be in use. Because of the equipment upgrades, Cook could sell the plant for 0 at the end of 4 years. No change in working capital would be required Cook Company treats all cash flows as if they occur at the end of the year, and uses an after-tax required rate of return of 8%. Cook is subject to a 30% tax rate on all income, including capital gains Calculate net present value of each of the options and determine which option Cook should select us ing the NPV criterion 1. 2. What nonfinancial factors should Cook consider before making its choi Problems 21-34 Equipment replacement, no income taxes. Dublin Chips is a manufacturer of prototype chips based in Dublin, Ireland. Next year, in 2018, Dublin Chips expects to deliver 615 prototype chips at an aver ge price of $95,000. Dublin Chips' marketing vice president forecasts growth of 65 prototype chip through 2024. That is, demand will be 615 in 2018, 680 in 2019, 745 in 2020, and so on s per year for The plant cannot produce more than 585 prototype chips annually. To meet future demand, Dublin Chips must either modernize the plant or replace it. The old equipment is fully depreciated and can be sold 200,000 if the plant is replaced. If the plant is modernized, the costs to modernize it are to be capitalized PITAL BUDGETING AND COST ANALYSIS of the mod- and depreciated over the useful life of the updated plant. The old equipment is retained as part ernize alternative. The following data on the two options are available Modernize $35,300,000 Replace $66,300,000 Initial investment in 2018 Terminal disposal value in 2024 Useful life Total annual cash operating costs per prototype chip S 7,500,000 $16,000,00 7 years 7 years $78,500 $66,000 Dublin Chips uses straight-line depreciation, assuming zero terminal disposal value. For simplicity, we as sume no change in prices or costs in future years. The investment will be made at the beginning of 2018, and all transactions thereafter occur on the last day of the year. Dublin Chips' required rate of return is 14% There is no difference between the modernize and replace alternatives in terms of required working capital. Dublin Chips has a special waiver on income taxes until 2024 1. Sketch the cash inflows and outflows of the modernize and replace alternatives over the 2018-2024 period. 2. Calculate the payback period for the modernize and replace alternatives. 3. Calculate net present value of the modernize and replace alternatives. 4. What factors should Dublin Chips consider in choosing between the alternatives? 21-35 Equipment replacement, income taxes (continuation of 21-34). Assume the same facts as in Problem 21-34, except that the plant is located in Buffalo, New York. Dublin Chips has no special waiver on ncome taxes. It pays a 35% tax rate on all income. Proceeds from sales of equipment above book value are axed at the same 35% rate 1. Sketch the after-tax cash inflows and outflows of the modernize and replace alternatives over the 2018-2024 period 2. Calculate the net present value of the modernize and replace alternatives. . Suppose Dublin Chips is planning to build several more plants. It wants to have the most advantageous tax position possible. Dublin Chips has been approached by Spain, Malaysia, and Australia to construct plants in their countries. Use the data in Problem 21-34 and this problem to briefly describe in qualita- tive terms the income tax features that would be advantageous to Dublin Chips. -36 DCE sensitivity analusis no in

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts