Question: The T-Bill's return is 2%. The Index A and Index B have the expected returns of 10% and 15% and the standard deviation of

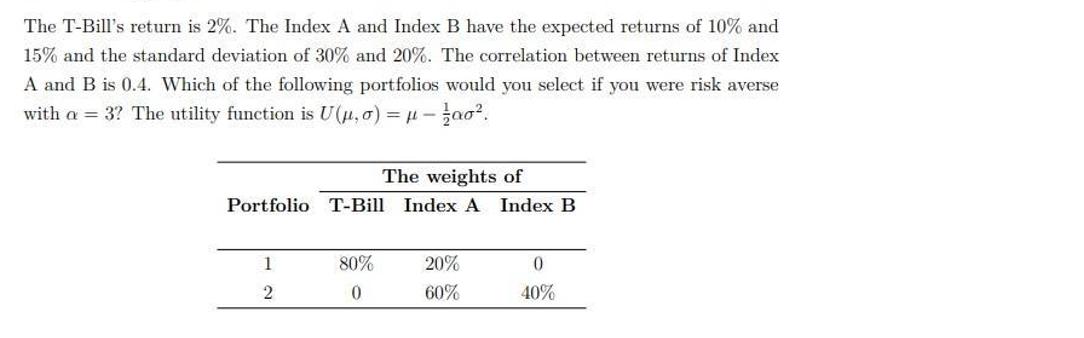

The T-Bill's return is 2%. The Index A and Index B have the expected returns of 10% and 15% and the standard deviation of 30% and 20%. The correlation between returns of Index A and B is 0.4. Which of the following portfolios would you select if you were risk averse with a = 3? The utility function is U(u,0) = -ao. The weights of Portfolio T-Bill Index A Index B 1 2 80% 0 20% 60% 0 40%

Step by Step Solution

★★★★★

3.41 Rating (157 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Expected return of Portfolio Standard deviation of Portfolio 120 30 ... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock