Answered step by step

Verified Expert Solution

Question

1 Approved Answer

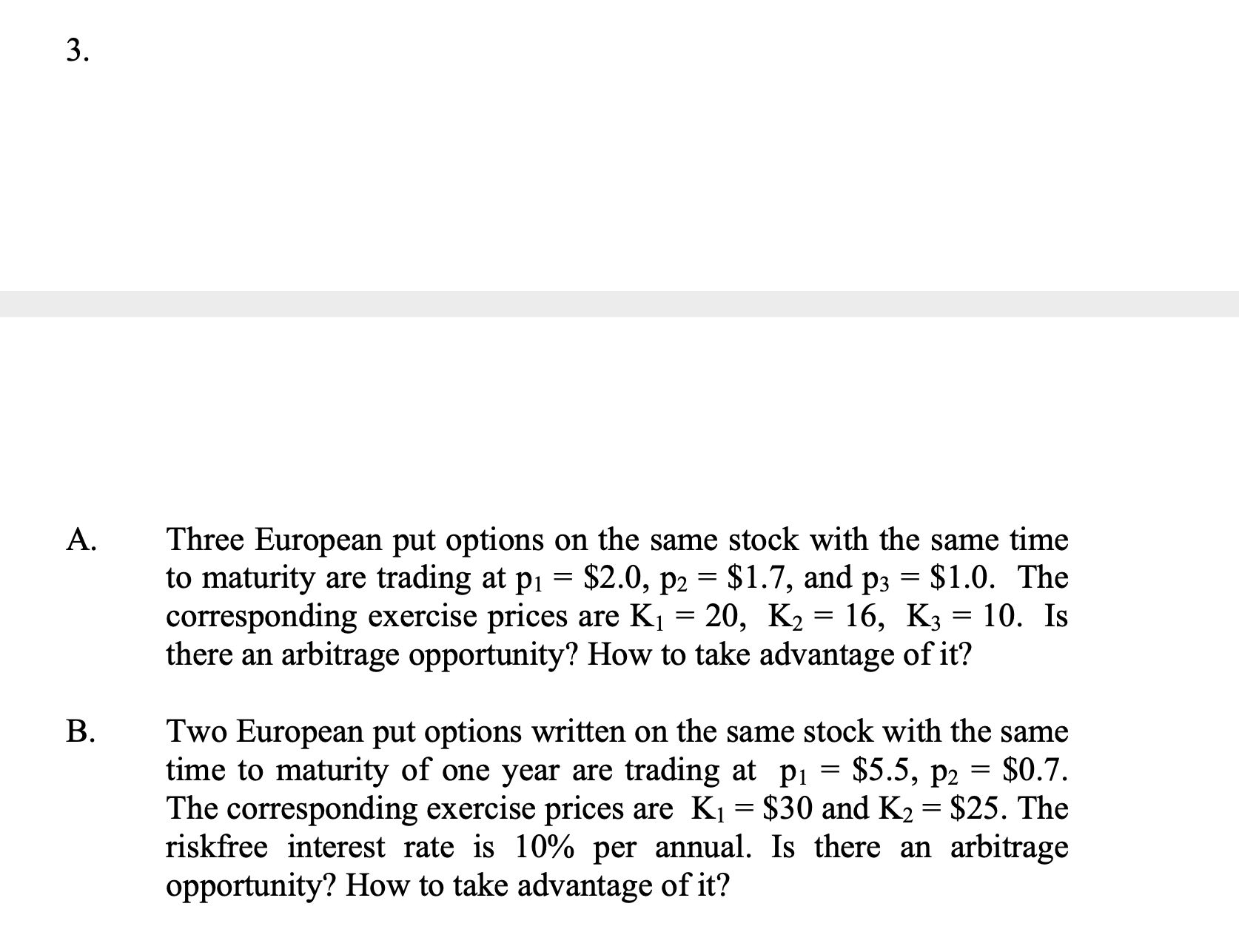

This was all the information that was provided to me. 3 . A. Three European put options on the same stock with the same time

This was all the information that was provided to me.

3 . A. Three European put options on the same stock with the same time to maturity are trading at P1 = $2.0, p2 = $1.7, and p3 = $1.0. The corresponding exercise prices are K1 = 20, K2 = 16, K3 = 10. Is there an arbitrage opportunity? How to take advantage of it? B. Two European put options written on the same stock with the same time to maturity of one year are trading at pi = $5.5, P2 = $0.7. The corresponding exercise prices are Ki = $30 and K2 = $25. The riskfree interest rate is 10% per annual. Is there an arbitrage opportunity? How to take advantage of it? 3 . A. Three European put options on the same stock with the same time to maturity are trading at P1 = $2.0, p2 = $1.7, and p3 = $1.0. The corresponding exercise prices are K1 = 20, K2 = 16, K3 = 10. Is there an arbitrage opportunity? How to take advantage of it? B. Two European put options written on the same stock with the same time to maturity of one year are trading at pi = $5.5, P2 = $0.7. The corresponding exercise prices are Ki = $30 and K2 = $25. The riskfree interest rate is 10% per annual. Is there an arbitrage opportunity? How to take advantage of itStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Organizational Behavior Improving Performance And Commitment In The Workplace

Authors: Jason Colquitt

8th Edition

126412435X, 9781264124350