Answered step by step

Verified Expert Solution

Question

1 Approved Answer

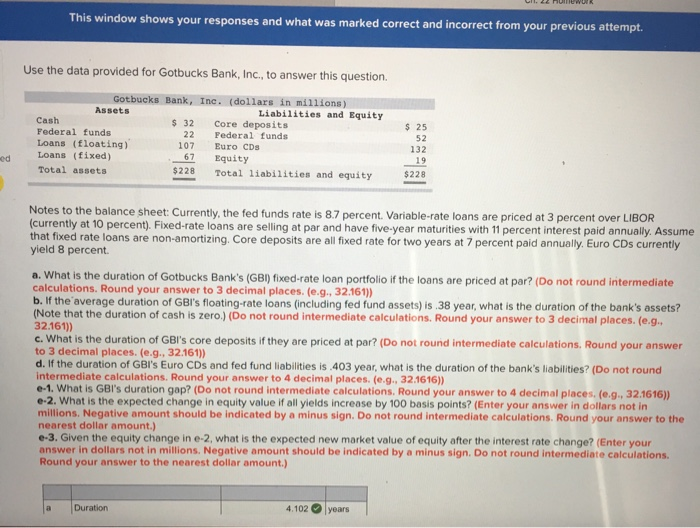

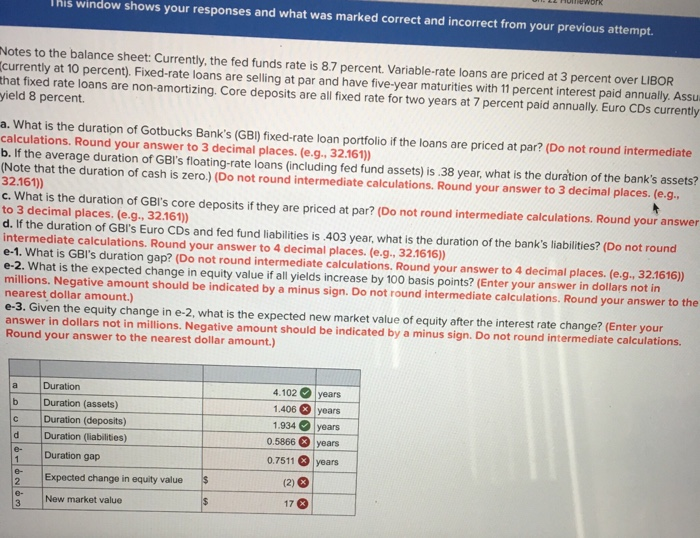

This window shows your responses and what was marked correct and incorrect from your previous attempt. Use the data provided for Gotbucks Bank, Inc., to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Algorithmic Finance A Companion To Data Science

Authors: Christopher Hian-ann Ting

1st Edition

9811238308, 978-9811238307