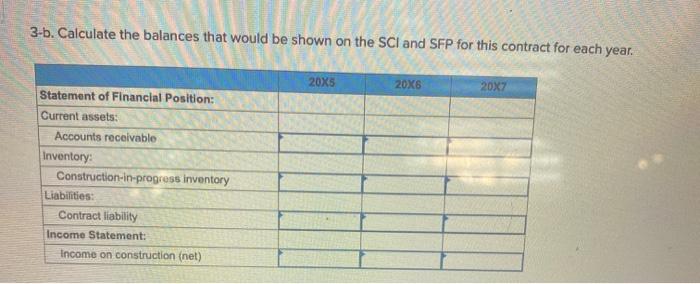

Thrasher Construction Co. was contracted to construct a building for $1,055,000. The building is owned by the customer throughout the contract period. The contract provides for progress payments. Thrasher's accounting year ends 31 December. Work began under the contract on 1 July 20X5, and was completed on 30 September 20X7, Construction activities are summarized below by year 20x5 Construction cost incurred during the year, 194,400; estimated costs to complete, $680,400; progress billing during the year, $165,000; and collections, $151,200. 2006 Construction costs incurred during the year, $486,000) estimated costs to complete, $205,200: progress billing during the year, $412,900; and collections, $410,400. 20x7 Construction costs incurred during the year, $211,000. Because the contract completed, the remaining balance was billed and later collected in full per the contract. Required: 1. Prepare Thrasher's journal entries to record these events. Assume that percentage of completion is measured by the ratio of costs incurred to date divided by total estimated construction costs. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Do not round Intermediate calculations. Round your final answers to the nearest whole dollar) 5 nces View transaction list Journal entry worksheet > Record the construction costs incurred. Date General Journal Dobit Credit 205 Contract costs 2. Provide the balances that would be shown on the SCI and SFP for this contract for each year. (Do not round intermediate calculations. Round your final answers to the nearest whole dollar.) 20x5 20X6 20x7 Statement of Financial Position: Current assets: Accounts receivable Contract annet Income Statement: Income on construction (net) 3-a. Now assume that the building is owned by Thrasher throughout the construction period and title is transferred to the customer only once the building is fully constructed. Prepare the journal entries required to record the events from 20x5 to 20x7.0f no entry is required for a transaction/event, select "No journal entry required" in the first account field.) View transaction ist Journal entry worksheet 2 Record the construction costs incurred. Note: Enter debits before credits Date General Journal Debut Credit 20x5 Record entry Clear entry View general Journal View transaction list Journal entry worksheet 2 5 > Record the construction costs incurred. Note: Enter debits before credits Date 20x7 General Journal Debit Credit Record entry Clear entry View gene journal 3-b. Calculate the balances that would be shown on the SCI and SFP for this contract for each year. 20X5 20X6 20X7 Statement of Financial Position: Current assets: Accounts receivable Inventory: Construction-in-progress inventory Liabilities: Contract liability Income Statement: Income on construction (net)