Answered step by step

Verified Expert Solution

Question

1 Approved Answer

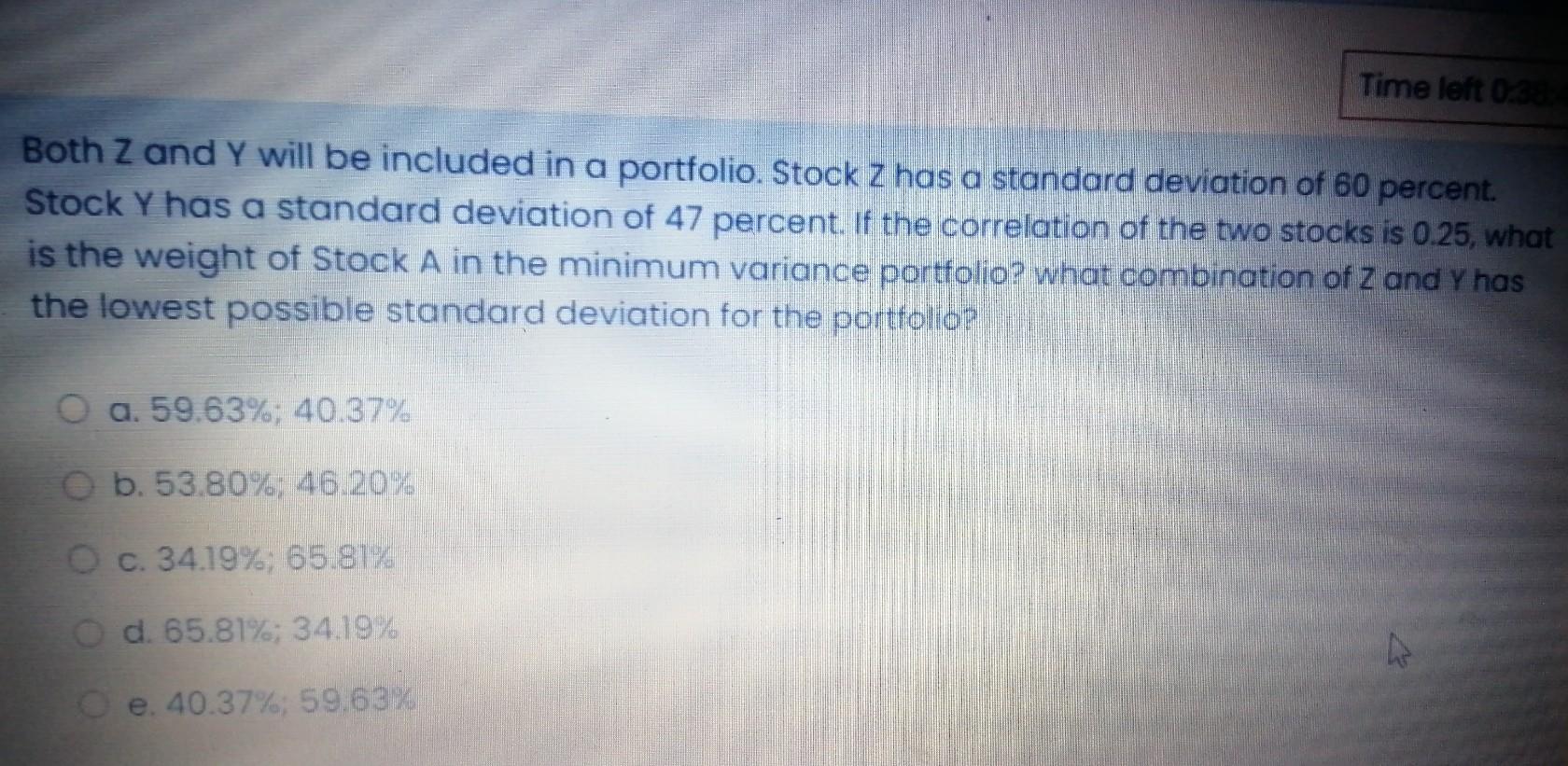

Time left 02 Both Z and Y will be included in a portfolio. Stock Z has a standard deviation of 60 percent. Stock Y has

Time left 02 Both Z and Y will be included in a portfolio. Stock Z has a standard deviation of 60 percent. Stock Y has a standard deviation of 47 percent. If the correlation of the two stocks is 0.25, what is the weight of Stock A in the minimum variance portfolio? what combination of Z and Y has the lowest possible standard deviation for the portfolio? O a. 59.63%; 40.37%. O b. 53.80%; 46.20% O c. 34.19%; 65.81% O d. 65.81%; 34.19% O e. 40.37%; 59.63%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Information Technology Auditing

Authors: James A. Hall

4th edition

1133949886, 978-1305445154, 1305445155, 978-1133949886