Answered step by step

Verified Expert Solution

Question

1 Approved Answer

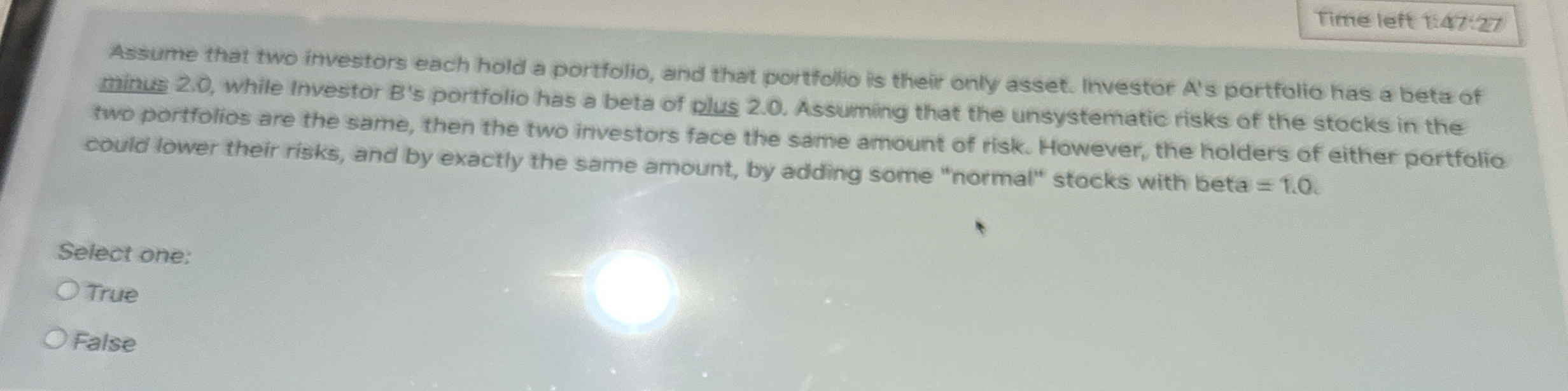

Time left 1 : 4 7 : 2 7 Assume that two investors each hold a portfolio, and that portfolio is their only asset. Investor

Time left ::

Assume that two investors each hold a portfolio, and that portfolio is their only asset. Investor As portfolio has a beta of minus while Investor Bs portfolio has a beta of plus Assuming that the unsystematic risks of the stocks in the two portfolios are the same, then the two investors face the same amount of risk. However, the holders of either portfolio could lower their risks, and by exactly the same amount, by adding some "normal" stoeks with beta

Select one:

True

False

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Valuing Mining Companies A Guide To The Assessment And Evaluation Of Assets Performance And Prospects

Authors: Charles Kernot

1st Edition

1855734354,1782420096