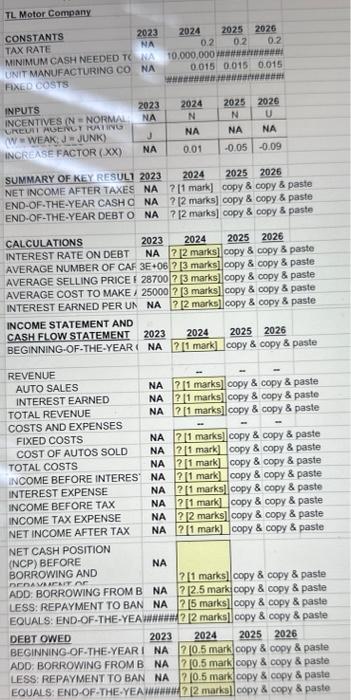

TL. Motor Compamy BEGINNING-OF-THE-YEAR ( NA ?[1 mark] copy \& copy \& paste \begin{tabular}{|c|c|c|c|c|} \hline REVENUE & & - & - & - \\ \hline AUTO SALES & NA & ?. [1 marks] & Lopy 8 & copy \& paste \\ \hline INTEREST EARNED & NA & ? [1 marks] & copy 8 & copy \& paste \\ \hline TOTAL REVENUE & NA & ? [1 marks] & copy \& & copy \& paste \\ \hline COSTS AND EXPENSES & & - & - & - \\ \hline FIXED COSTS & NA & ? [1 marks] & floor copy& & copy \& paste \\ \hline COST OF AUTOS SOLD & NA & ?] [1 mark] & copy8 & copy \& paste \\ \hline TOTAL COSTS & NA & ?[1 mark]. & copy 8 & \& copy \& paste \\ \hline INCOME BEFORE INTERES & NA & ? [1 mark] & copy \& & paste \\ \hline INTEREST EXPENSE & NA & ? [1 marks] & copy 8 & copy \& paste \\ \hline BEFORE TAX & NA & ?[1 mark] & copy \& & \& copy \& paste \\ \hline INCOME TA & NA & ? [2 marks] & copy 8 & paste \\ \hline NET INCOM & NA & ? [1 mark] & ]cop & paste \\ \hline \begin{tabular}{l} NET CASH POSITION \\ (NCP) BEFORE \\ BORROWING AND \\ nERA UNENT Ar \end{tabular} & NA & ? [1 marks] & 1 copy 8 & paste \\ \hline ADD: BORROWING FROM B & NA & ?[2.5mark & jcopy \& & 8 copy \& paste \\ \hline 8: REPAYMENT TO BAN & NA & ? [5 marks] & 1copy8 & 3 copy \& paste \\ \hline LS: END-OF-THE-YEA & & ?[2 & 1copy& & © \\ \hline DEBT OWED & 2023 & 2024 & 2025 & 2026 \\ \hline BEGINNING-OF-THE-YEARI & NA & 210.5mark & copy 8 & \& copy \& paste \\ \hline ADD: BORROWING FROM B & NA & ?[0.5mark & copy 8 & & copy \& paste \\ \hline LESS: REPAYMENT TO BAN & NA & ?[0.5mark & copy 8 & 8. copy \& paste \\ \hline EOUALS: END-OF-THE-YEAI & & ks] & 1copy8 & 8 copy \& paste \\ \hline \end{tabular} Refer to Table 1. Write the Fxeel formula for each cell marked with "? in column C sach that formula could be copied and pasted into columns D and E. using Microsoft Excel without further editing. There is no need to explicitly write the Excel formula for cells marked with "Copy \& paste". I abel each formula clearly with cell reference position. TI. Motor Company has been successfully making autos and trucks for more than 100 years in the United States (U.S.). and was one of the dominant car companies in the U.S. automobile industry. Recent years, however, have been very difficult for TI. Indeed, they have been difficult years for all automobile companies. The automobile industry is now a highly competitive business globally. Twenty years ago, TL competed against only two other auto companies in the domestic market, but there are now a dozen large foreign auto companies to compete against. The emerging Chinese electric automobile companies that are subsidized by the Chinese government have very cheap labour costs. Competition from the Chinese electric vehicles is expected to drive down the selling price of all types of autos, and TL's sales and profit margins would be reduced dramatically in future. TL, currently, has very high debts as it owes USS30 billion at the end of year 2023 (cell B52), and interest expense is high. In the last two years, TL has just about broken even - net income after tax has been close to zero. TL's management is considering dissolving the company if large profits cannot be made in the next three years (2024 to 2026) before govemment policy makers allow Chinese electric car models to be sold massively in the U.S. TL's management reasons that TL's better models could be sold to other car companies and the proceeds distributed to the shareholders. This would be better than a slow march to bankruptcy, resulting in shareholders getting nothing. In year 2023, TL's management would like to forecast its financial situation such as the net income, debt owed and cash flow for the next three years (2024 - 2026) based on 2023 's data so that TL's management can decide what to do next. You are asked to help TL's management and write Excel formulas in cells C19 to C52 to do these forecasts by performing a what-if analysis using Microsoft Excel. Most automobile industry executives also think there is an oversupply of autos and trucks relative to consumer demand. When supply exceeds demand, there will be downward pressure on selling price, and this forces TL's management to introduce two kinds of "incentive" programs: cash-back and special loyy rate financing. Cash-back incenile meins offering discounts on the listed price of a car, for cxample offering USS80wo off a USS30,000 car. Special low-rate financing meains lending moncy to car buyers at below-bank interest rates. TL. may offer a cumbinition of both kinds of incentive programs, Incentives are assumed a permanent ficature of automobile marketing; and there are two levels of incentives (row 10): - Normal (N) - if competition is not fierce such that incentives are expected to be at normal levels. - LP(U) - if competition is intense such that aggressive incentives (that means high price discounts and/or very low interest rate financing) are expected. Levels of incentives can vary from year to year. If incentives level is expected to be N for year 2024,N for year 2025 and U for year 2026 , then the pattem NNU would be entered in cells Cl10 to E10. TL has its own finance unit whose activity has been lending money to car buyers. This division borrows money at low interest rates in credit markets or from the company's bankers. and can make profits when lending this money to car buyers at higher interest rates. For example, the finance unit borrows money at 5% interest rate from its bank and then make loans to car buyers at 6% to 8% interest rate, thus TL makes money in the form of interest earned on car loans to car buyers. However, in periods of aggressive incentives with low-rate financing being offered to car buyers, TL's finance unit loses money because it lends money at a rate less than the rate TL borrows at. TL's finance unit also handles general corporate borrowings as well. For example, TL may want to borrow US $100 million to build a new manufacturing plant, then it would negotiate with the company's bankers to borrow money, or it would go to Wall Street to sell bonds to raise money. All bond issuers are rated by independent credit analysis agencies. The ratings are intended as a measure of how likely a company is to pay off existing debts (interest and principle). A poor rating would reduce investor confidence and would mean that TL would have to borrow money at higher interest rates. A high rating would increase investor confidence in TL and means TL can borrow money at lower interest rates. Thus, credit agency rating greatly affects interest rates in the bond market, and it has two values for TL (cell B11): - Weak (W) - if competition is fierce, and TL is in great debt such that the rating is not expected to improve in the near future. - Junk (J) - this is the lowest rating in the bond market if TL worsens nearly to default and requires government bailout. The credit agency rating entered in cell B1I applies to all three forecast years 2024 Calculations (rows 19 to 24 ) are described below: - Interest rate on debt (row 20): If the credit agency rating is weak (W) in the next three years, the interest rate paid on debt owed will be 5% in each of the next three years. If the rating is junk-bond (J) status, the interest rate will be 10% in each of the next three years. - Average number of car units sold (row 21): The average number of car units sold in a year is based on the prior year's sales units and the unit car sales increase factor (see row 12). - Average selling price per unit (row 22): If the level of incentives is expected to be normal (N) in a year, then TL can be expected to raise the average unit selling price per unit 1.5% over the prior year's price. However, if the level of incentives is expected to be up (U) in a year, the average unit selling price per umit in a year will be 5% less than the prior year's selling price. - Direct cost to make a car unit (row 23): The anerage direct cost to make an automobile in a ycur is based on the prior year's direct cost to make a car unit, and on the unit manuficturing cost reduction factor. Interest eamed per car unit sold (row 24): Majority of car buyers will finance the purchase through TL's finance unit. Financing is a source of income (or loss) to TL. If the incentives are normal in a year, TL can expect to make on average about US\$200 in interest revenue on a unit sold. However, if incentives are up, only about USS25 in interest revenue is eamod per unit sold, on average. Income \& Cash Flow Statements (rows 26 to 41) are described below: - Cash at the beginning of a year (row 27); this is the cash at the end of previous year. - Revenue from auto sales (row 30): This is based on the average number of car units sold in that year and on the average selling price per car unit in that year- - Revenue from interest eamed (row 31): This is based on the average number of car units sold in that year and on the interest eamed per car unit sold in that year. - Total revenue (row 32 ): This is the total revenue from auto sales and interest eamed. - Fixed costs (row 34): Fixed costs do not vary much with the number of autos sold, and they include research-and-development costs, advertising and promotion costs and other general administrative costs. - Total direct costs of autos sold (row 35): This is based on the average number of car units sold in that year and on the average cost to make a car unit in that year: - Total costs (row 36): This is the total of the direct costs and fixed costs in that year: - Income before interest and tax (row 37): Before considering tax and interest expense, this is the difference between total revenue and total costs. - Interest expense (row 38): This is a simple interest based on the year's interest rate and the debt owed at the beginning of that year. - Income before tax (row 39): Before considering tax, but after considering interest expense, this is the difference between income before interest and tax, and interest expense. - Income tax expense (row 40): This is zero if income before tax is zero or less: otherwise, apply the tax rate for the year to the income before tax. Net income after tax (row 41): This is the difference between income before tax and income tax expense. - Net Cash Position (NCP) (row 43): NCP at the end of a year equals the cash beginning of a year, plus the year's net income, assuming that there are no receivables or payables. Assume that TL's bankers will lend enough money (row 44) at the end of a ycar to get to TL's minimum cash target (see row 5). If the NCP is less than the minimum cash at the end of a year, TL must borrow enough to reach the minimum cash target. Borrowings increase cash on hand, of course. - If the NCP is more than the minimum cash and there is outstanding debt from previous year(s), then some or all of the debt should be repaid, but not to take your company below the minimum cash level (row 45). - Cash at the end of the year equals the NCP, plus any borrowings and less any repayments (row 46 ). Debt Owed (rows 48 to 52 ) is described below: - The amount of US\$20 billion (cell B52) is already owed to bankers and bondholders at the end of 2023 . - Debt owed at the beginning of a year equals the debt owed at the end of previous year. - Amounts borrowed and repaid that have been calculated before can be echoed to this section. - The amount owed at the end of a year equals to the debt owed at the beginning of the year plus any borrowings, and less any repayments. Table 1: 'NA'= Not Applicable, meaning no entry is required in the cell. \begin{tabular}{|c|c|c|c|c|c|} \hline & A & B & C & D & E \\ \hline \multicolumn{6}{|c|}{1 IL MotorCompany } \\ \hline 32 & CONSTANTS & 2023 & & 2025 & 2006 \\ \hline 4 & TAXRATE & NA & 02 & 0.20.2 & 02 \\ \hline 5 & MINIMUM CASH NEEOEDD TO START NEXT YEAR & NA & 10000000 & 10000000 & 10000000 \\ \hline 6 & UNIT MANUFACTURING COST REDUCTION FACTOR & NA & 0.015 & 0.015 & 0.015 \\ \hline 7 & FIXED COSTS & & 700000000 & 7000000000 & 700000000 \\ \hline 8 & & & & & \\ \hline 9 & IPPUTS & 2023 & 2024 & 2025 & 2025 \\ \hline 10 & INCENTIVES ( N= NORMAL; U=UP) & NA & N & N & U \\ \hline 11 & CREDIT AGENCY RATING ( W= WEAK; J=JUNK) & j & NA & NA & NA \\ \hline 12 & UNT CAR SALES INCREASE FACTOR (XX) & NA & 0.01 & .005 & -009 \\ \hline 13 & & & & & \\ \hline 14 & SUMMARY OF KEY RESULTS & 2023 & 2024 & 2025 & 2026 \\ \hline 15 & NET WCOME AFTERTAVES & NA & = CA1 & =041 & =E41 \\ \hline 16 & END-OF-THE-YEAR CASH ONHAND & NA & =C46 & =046 & =E46 \\ \hline 17 & END-OF-THE-YEAR DEBT OWED & NA & =C52 & =052 & =E52 \\ \hline 18 & & & & & \\ \hline 19 & CALCULATIONS & 2023 & 2024 & 2025 & 2026 \\ \hline 20 & INTEREST RATE ONDEBT & NA & ? [2 marks] & copy \& paste & copy \& paste \\ \hline 21 & AVERAGE NUMBER OF CAR UNITS SOLD & 3125000 & ? [3 marks] & copy \& paste & copy \& paste \\ \hline 22 & AVERAGE SELLING PRICE PER UNIT & 28700 & ?[3 marks] & copy \& paste & copy \& paste \\ \hline 23 & AVERAGE COST TO MAKE A CARUNIT & 25000 & ?[3 marks] & copy \& paste & copy \& paste \\ \hline 24 & INTEREST EARNED PER UNIT SOLD & NA & ?[2 marks] & copy \& paste & copy \& paste \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|} \hline A & B & C & 0 & E \\ \hline \begin{tabular}{l} INCOUE STATEMENT AND \\ 26 CASH FLOW STAIEIENT \end{tabular} & 2023 & 2024 & 2025 & 2026 \\ \hline 27 BEGNNNGOF-THE-YEAR CASH ON HAND & NA & ?[1 makk] & copy& paste & copy \& paste \\ \hline & & & & \\ \hline 29 REVENUE & & - & - & - \\ \hline 30 AUTOSALES & NA & ?[1 marks } & copy \& paste o & cooy \& pasie \\ \hline 31 INTERESTEARNED & NA & ?[1 marks] & copy \& paste c & copy \& paste \\ \hline 32 TOTAL REVENUE & NA & ?[1 marks] & copy \& pasie o & copy \& paste \\ \hline 33 COSTS AND EXPENSES & & - & -. & - \\ \hline 34. FIXED COSTS & NA & ?[1 marks] & copy \& paste o & copy \& paste \\ \hline 35 COST OF AUTOS SOLD & NA & ?[1 mark] & copy \& paste c & copy \& paste \\ \hline 36 TOTAL COSTS & NA & ?[1 mark] & copy \& paste c & cooy \& paste \\ \hline 37 INCOME BEFORE INTERESTAND TAX & NA & ?[1 mark] & cooy \& paste c & copy \& paste \\ \hline 38 INTEREST EXPENSE & NA & ? [1 marks] & copy \& pasie c & copy \& paste \\ \hline 39 INCONE BEFORE TAX & NA & ?[1 mark ] & copy \& paste c & cooy \& paste \\ \hline 40 INCONE TAX EXPENSE & NA & ?[2 marks] & copy \& paste c & copy \& paste \\ \hline 41 NET INCOME AFTER TAX & NA & ?[1 mark] & copy \& paste c & cooy \& paste \\ \hline \begin{tabular}{l} NET CASH POSTITON (NCP) BEFORE \\ BORROWING AND REPAYNENT OF \\ 43 DEBT (BEG OF YR CASH + NET INCOME) \end{tabular} & NA & ?[1 marks ] & copy \& paste c & copy \& paste \\ \hline 44 ADD: BORROWING FROM BANK & NA & ? [2.5marks] & copy \& paste c & copy \& paste \\ \hline 45 LESS: REPAYMENT TO BANK & NA & ?[5 marks ] & copy \& paste c & copy \& paste \\ \hline 46 EQUALS: END-OF-THE-YEAR CASH ONHAND & 10000000 & ?[2 marks] & copy \& paste & copy \& paste \\ \hline 48 DEBT OWED & 2023 & 2024 & 2025 & 2026 \\ \hline 49 BEGINNNG-OF-THE-YEARDEBT OWED & NA & ?[0.5 mark ] & copy& paste & copy \& paste \\ \hline 50 ADD: BORROWING FROM BANK & NA & ?[0.5 mark ] & copy \& paste c & copy \& paste \\ \hline 51 LESS: REPAYMENT TO BANK & NA & ?[0.5 mark] & copy \& paste & copy \& paste \\ \hline 52 EQUALS: END-OF-THE-YEARDEBT OWED & 30000000000 & ? [2 marks] & copy \& paste & copy \& paste \\ \hline \end{tabular}