Answered step by step

Verified Expert Solution

Question

1 Approved Answer

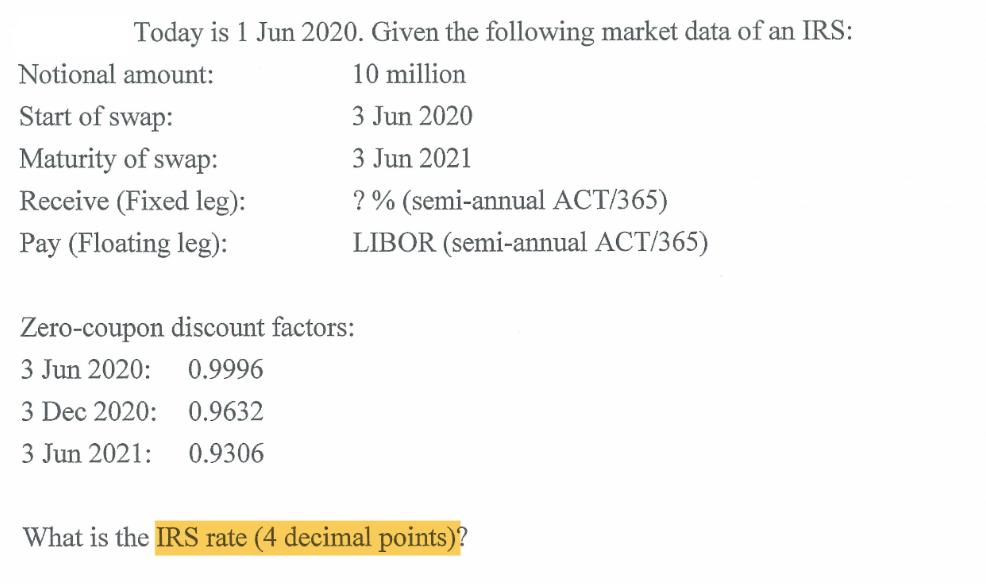

Today is 1 Jun 2020. Given the following market data of an IRS: 10 million 3 Jun 2020 3 Jun 2021 ? % (semi-annual

Today is 1 Jun 2020. Given the following market data of an IRS: 10 million 3 Jun 2020 3 Jun 2021 ? % (semi-annual ACT/365) LIBOR (semi-annual ACT/365) Notional amount: Start of swap: Maturity of swap: Receive (Fixed leg): Pay (Floating leg): Zero-coupon discount factors: 3 Jun 2020: 0.9996 0.9632 0.9306 3 Dec 2020: 3 Jun 2021: What is the IRS rate (4 decimal points)?

Step by Step Solution

★★★★★

3.48 Rating (145 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the IRS Interest Rate Swap rate we will assume that the present value of the fixed leg is equal to the present value of the floating leg ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Corporate Finance

Authors: Laurence Booth, Sean Cleary

3rd Edition

978-1118300763, 1118300769