Question

Today is February 8, 2021, and GameStop Corp.' stock is trading for USD 59.04 in the spot market, down from USD 469.4194 on January 29,

A) Calculate the implied volatility for each option and describe the pattern that you observe. Is this pattern surprising to you? Does it contravene the law of one price in the option market? Please, discuss briefly.

B) Calculate the delta, gamma, vega, theta, and rho of each option. Present your results in a neat table displaying each Greek in a separate column.

C) Assume that you are short 10 contracts of each call option contract and long 10 contracts of each put option and calculate the Greeks of your portfolio.

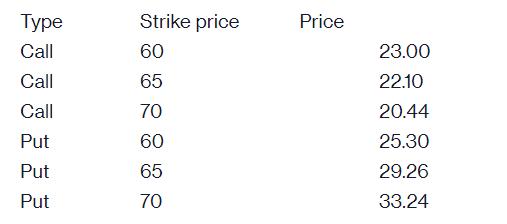

Type Call Call Call Put Put Put Strike price 60 65 70 60 65 70 Price 23.00 22.10 20.44 25.30 29.26 33.24

Step by Step Solution

3.48 Rating (168 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance A Focused Approach

Authors: Michael C. Ehrhardt, Eugene F. Brigham

4th Edition

1439078084, 978-1439078082