Answered step by step

Verified Expert Solution

Question

1 Approved Answer

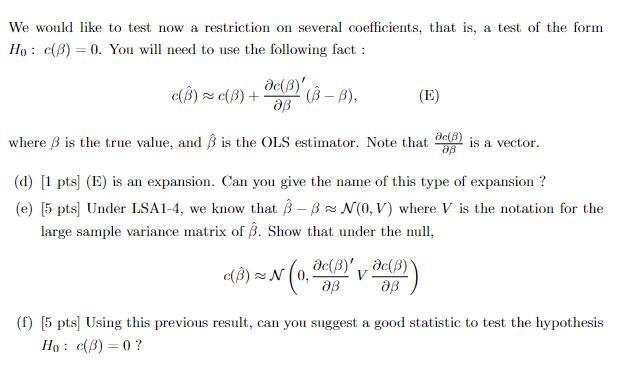

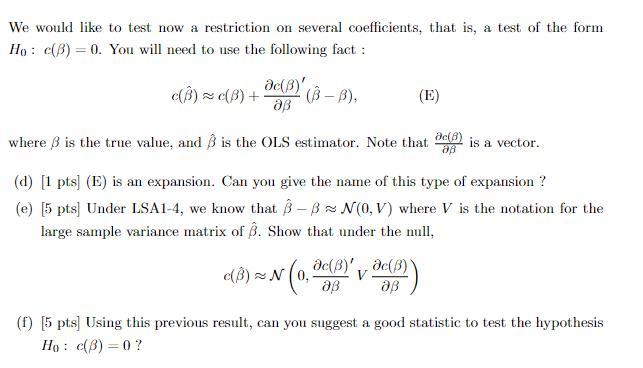

6. [25 pts] Exercise Consider the linear regression with three regressors Yi=1X1i+2X2i+3X3i+ui=Xi+ui, where =123 and Xi=X1iX2iX3i (a) [3 pts] You would like to test whether

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Management A Strategic Emphasis

Authors: Edward Blocher, David Stout, Paul Juras, Gary Cokins

7th edition

77733770, 978-0077733773