Answered step by step

Verified Expert Solution

Question

1 Approved Answer

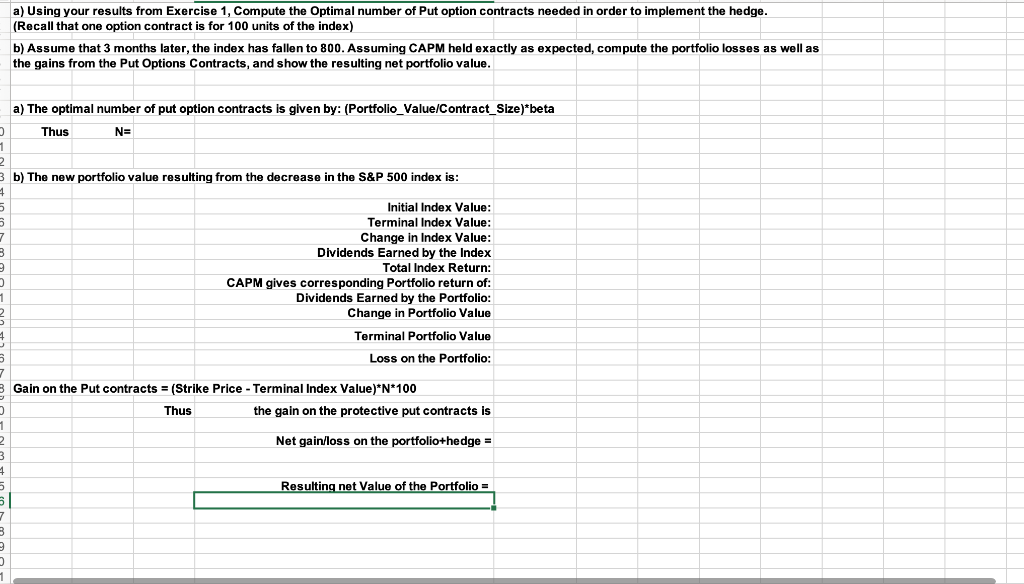

a) Using your results from Exercise 1, Compute the optimal number of Put option contracts needed in order to implement the hedge. (Recall that one

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Corporate Finance

Authors: Stephen A Ross, Randolph W Westerfield, Bradford D Jordan

7th Edition

0073134295, 9780073134291