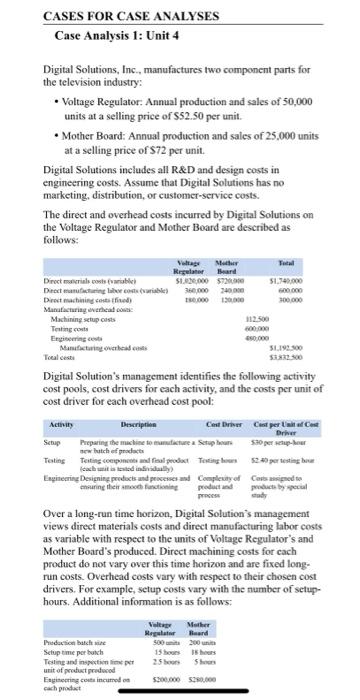

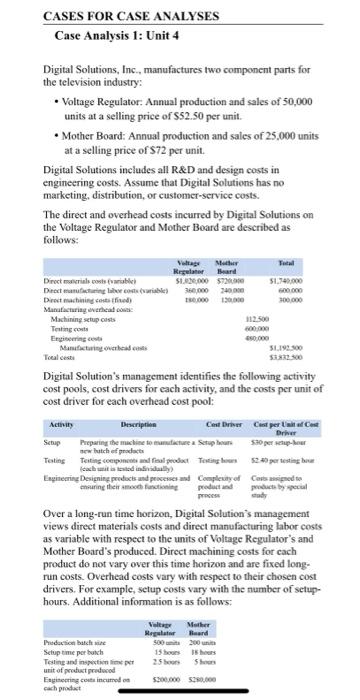

CASES FOR CASE ANALYSES Case Analysis 1: Unit 4 Digital Solutions, Inc., manufactures two component parts for the television industry: Voltage Regulator: Annual production and sales of 50,000 units at a selling price of 532.50 per unit. Mother Board: Annual production and sales of 25.000 units at a selling price of S72 per unit. Digital Solutions includes all R&D and design costs in engineering costs. Assume that Digital Solutions has no marketing, distribution, or customer-service costs. The direct and overhead costs incurred by Digital Solutions on the Voltage Regulator and Mother Board are described as follows: Repeater Brand Directions will 51.000 5720 51.745.000 Deelting laine est vible) 360,000 340.000 Direct machining coststed) Mustacturing verhale Machining setup Testing costs Engineering cente 650.000 Manufacturing 5093 Tocalceste Digital Solution's management identifies the following activity cost pools, cost drivers for each activity, and the costs per unit of cost driver for each overhead cost pool: Activity Cest Driver Cost per Case Driver Setup Preparing the machine to manicure Setup 50 per per w lutch of products Testing Teting compete fal product Tertingos caci ested in all Engineering Designing products and processes and Complety of Casiged to muring their moth functioning product and products by special Over a long-run time horizon, Digital Solution's management views direct materials costs and direct manufacturing labor costs as variable with respect to the units of Voltage Regulator's and Mother Board's produced. Direct machining costs for cach product do not vary over this time horizon and are fixed long- run costs. Overhead costs vary with respect to their chosen cost drivers. For example, setup costs vary with the number of setup- hours. Additional information is as follows: Voltage Mehr 500 units 200 units 15 hours Pedactice batch Setup time perbuch Testing and inspectie unit of product produced Engineering concurred cach prodat CASES FOR CASE ANALYSES Case Analysis 1: Unit 4 Digital Solutions, Inc., manufactures two component parts for the television industry: Voltage Regulator: Annual production and sales of 50,000 units at a selling price of 532.50 per unit. Mother Board: Annual production and sales of 25.000 units at a selling price of S72 per unit. Digital Solutions includes all R&D and design costs in engineering costs. Assume that Digital Solutions has no marketing, distribution, or customer-service costs. The direct and overhead costs incurred by Digital Solutions on the Voltage Regulator and Mother Board are described as follows: Repeater Brand Directions will 51.000 5720 51.745.000 Deelting laine est vible) 360,000 340.000 Direct machining coststed) Mustacturing verhale Machining setup Testing costs Engineering cente 650.000 Manufacturing 5093 Tocalceste Digital Solution's management identifies the following activity cost pools, cost drivers for each activity, and the costs per unit of cost driver for each overhead cost pool: Activity Cest Driver Cost per Case Driver Setup Preparing the machine to manicure Setup 50 per per w lutch of products Testing Teting compete fal product Tertingos caci ested in all Engineering Designing products and processes and Complety of Casiged to muring their moth functioning product and products by special Over a long-run time horizon, Digital Solution's management views direct materials costs and direct manufacturing labor costs as variable with respect to the units of Voltage Regulator's and Mother Board's produced. Direct machining costs for cach product do not vary over this time horizon and are fixed long- run costs. Overhead costs vary with respect to their chosen cost drivers. For example, setup costs vary with the number of setup- hours. Additional information is as follows: Voltage Mehr 500 units 200 units 15 hours Pedactice batch Setup time perbuch Testing and inspectie unit of product produced Engineering concurred cach prodat