Answered step by step

Verified Expert Solution

Question

1 Approved Answer

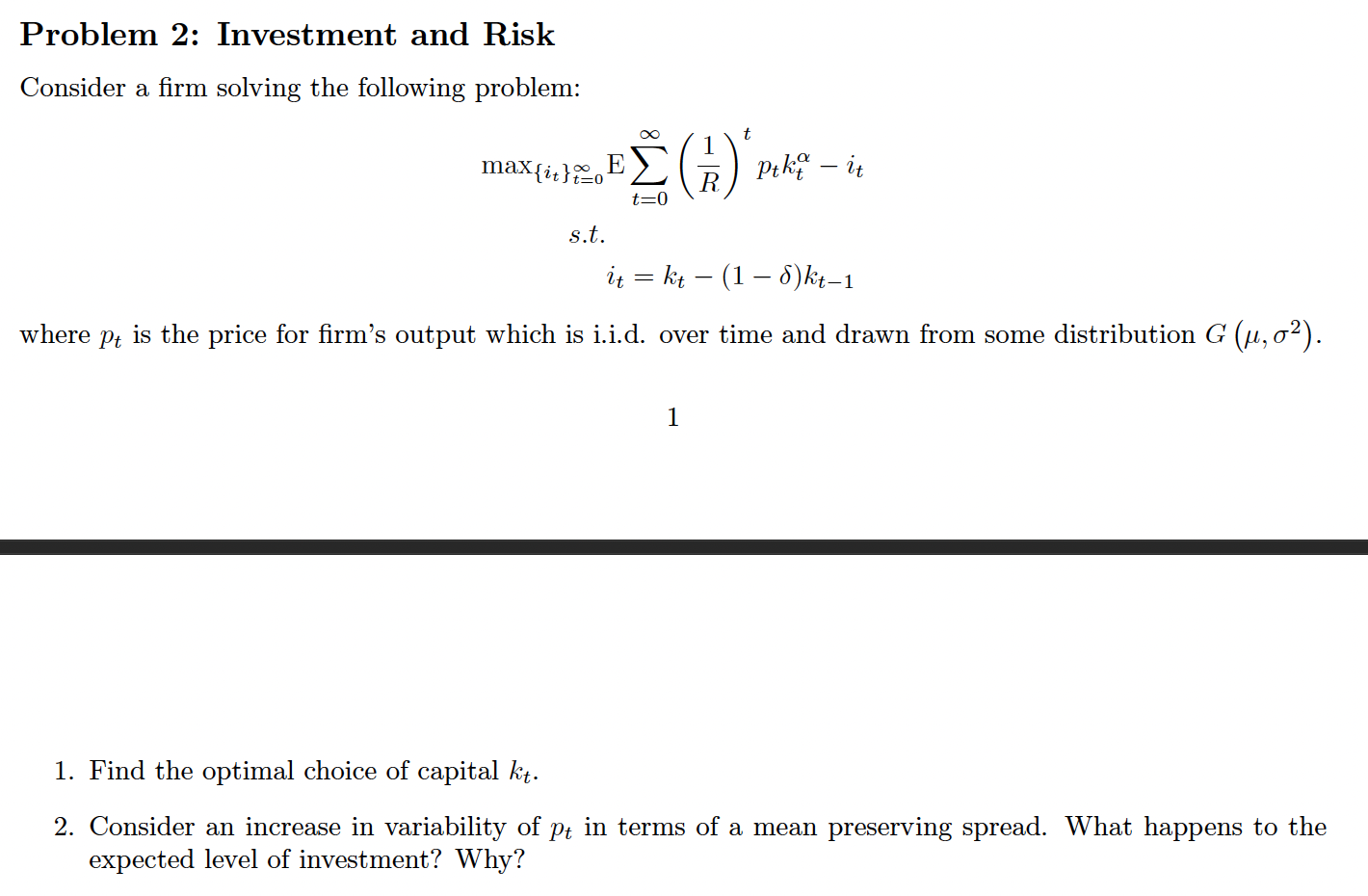

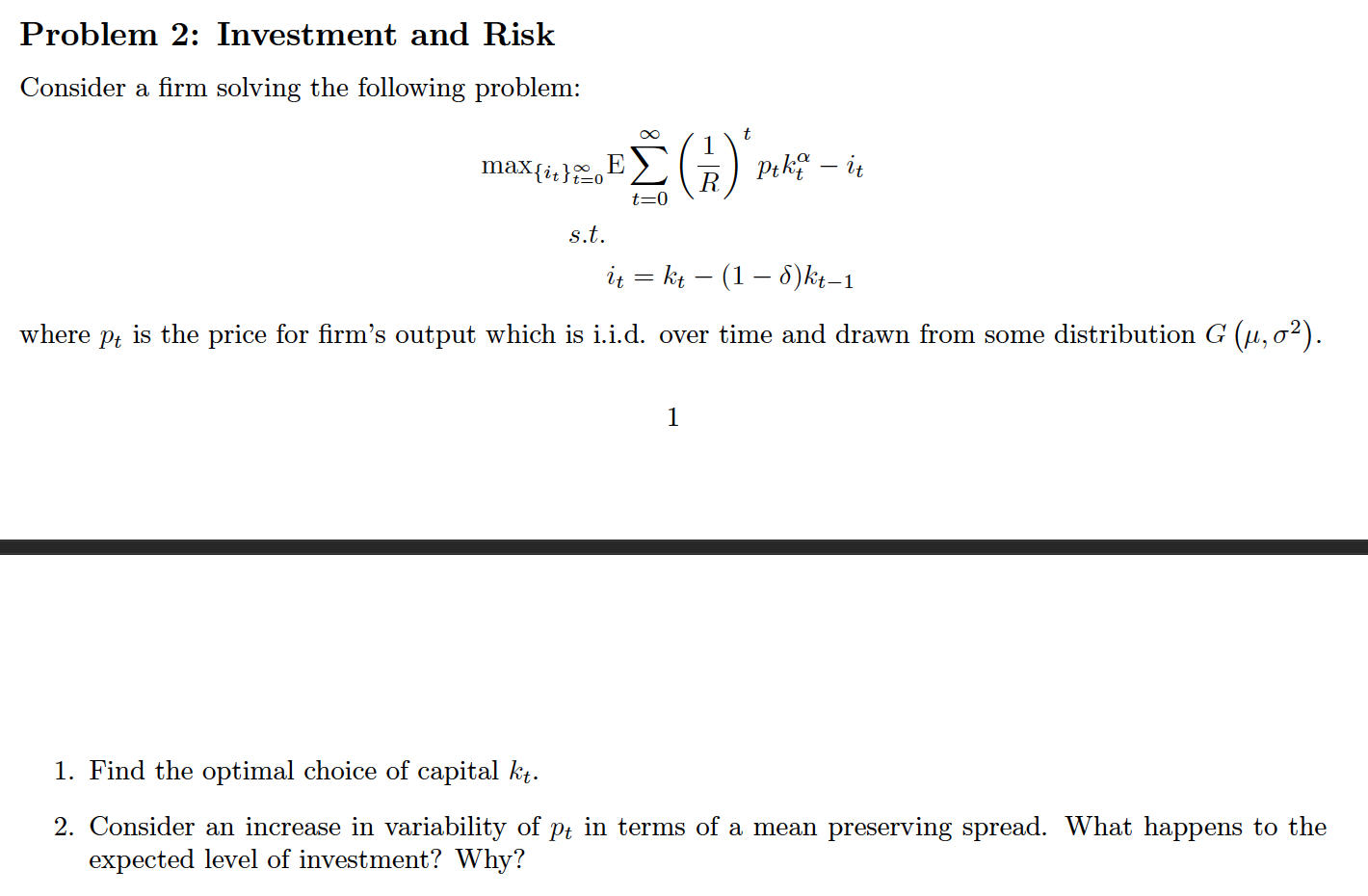

Problem 2: Investment and Risk Consider a firm solving the following problem: max{it}t=0Et=0(R1)tptktits.t.it=kt(1)kt1 where pt is the price for firm's output which is i.i.d. over

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Carl S. Warren, Jim Reeve, Jonathan Duchac

14th edition

1305088433, 978-1305088436