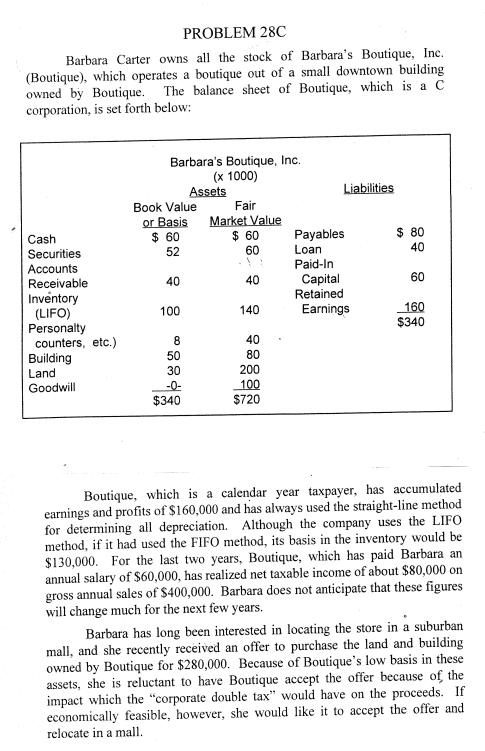

PROBLEM 28C Barbara Carter owns all the stock of Barbara's Boutique, Inc. (Boutique), which operates a boutique out of a small downtown building owned by Boutique. The balance sheet of Boutique, which is a C corporation, is set forth below: 60 Cash Securities Accounts Receivable Inventory (LIFO) Personalty counters, etc.) Building Land Goodwill Barbara's Boutique, Inc. (* 1000) Assets Liabilities Book Value Fair or Basis Market Value $ 60 $ 60 Payables $ 80 52 Loan 40 Paid-In 40 40 Capital 60 Retained 100 140 Earnings 160 $340 8 40 50 80 30 200 -O- 100 $340 $720 Boutique, which is a calendar year taxpayer, has accumulated earnings and profits of $160,000 and has always used the straight-line method for determining all depreciation. Although the company uses the LIFO method, if it had used the FIFO method, its basis in the inventory would be $130,000. For the last two years, Boutique, which has paid Barbara an annual salary of $60,000, has realized net taxable income of about $80,000 on gross annual sales of $400,000. Barbara does not anticipate that these figures will change much for the next few years. Barbara has long been interested in locating the store in a suburban mall, and she recently received an offer to purchase the land and building owned by Boutique for $280,000. Because of Boutique's low basis in these assets, she is reluctant to have Boutique accept the offer because of the impact which the "corporate double tax" would have on the proceeds. If economically feasible, however, she would like it to accept the offer and relocate in a mall Barbara informs you that her brother, Paul, who is a third-year law student, suggested that she cause Boutique to: (1) elect Scorporation status effective at the beginning of the next calendar year; (2) defer the sale until that year; (3) distribute the proceeds of the sale to Barbara in the year of sale; and (4) revoke the corporation status effective for the next succeeding calendar year. As an alternative to items (3) and (4), Paul suggested that Barbara consider causing Boutique to: (1) sell the land and building for the purchaser's installment obligation, which would have a term of eleven years, have interest only payable during the first ten years, provide that the full amount of principal would be payable at the end of the eleventh year and would be secured by a mortgage on the land and building; (2) continue the S corporation status through the year in which the installment obligation is paid in full, distributing interest and principal payments to Barbara; and (3) revoke the corporation status effective for the year following the year in which the installment obligation is paid in full. Barbara would like your advice on the tax consequences of following Paul's suggestions. Case 28C Issues 1. What would be the amount of "double taxation on the sale of the building and land for $280,000 assuming the after-tax proceeds from that sale are distributed to Ms. Carter as a dividend? 2. What would be the income tax consequences if Ms. Carter implements the four-step plan A? 3. What would be the income tax consequences if Ms. Carter implements the plan B over ten plus years? 4. What alternative plan would you recommend to Ms. Carter? PROBLEM 28C Barbara Carter owns all the stock of Barbara's Boutique, Inc. (Boutique), which operates a boutique out of a small downtown building owned by Boutique. The balance sheet of Boutique, which is a C corporation, is set forth below: 60 Cash Securities Accounts Receivable Inventory (LIFO) Personalty counters, etc.) Building Land Goodwill Barbara's Boutique, Inc. (* 1000) Assets Liabilities Book Value Fair or Basis Market Value $ 60 $ 60 Payables $ 80 52 Loan 40 Paid-In 40 40 Capital 60 Retained 100 140 Earnings 160 $340 8 40 50 80 30 200 -O- 100 $340 $720 Boutique, which is a calendar year taxpayer, has accumulated earnings and profits of $160,000 and has always used the straight-line method for determining all depreciation. Although the company uses the LIFO method, if it had used the FIFO method, its basis in the inventory would be $130,000. For the last two years, Boutique, which has paid Barbara an annual salary of $60,000, has realized net taxable income of about $80,000 on gross annual sales of $400,000. Barbara does not anticipate that these figures will change much for the next few years. Barbara has long been interested in locating the store in a suburban mall, and she recently received an offer to purchase the land and building owned by Boutique for $280,000. Because of Boutique's low basis in these assets, she is reluctant to have Boutique accept the offer because of the impact which the "corporate double tax" would have on the proceeds. If economically feasible, however, she would like it to accept the offer and relocate in a mall Barbara informs you that her brother, Paul, who is a third-year law student, suggested that she cause Boutique to: (1) elect Scorporation status effective at the beginning of the next calendar year; (2) defer the sale until that year; (3) distribute the proceeds of the sale to Barbara in the year of sale; and (4) revoke the corporation status effective for the next succeeding calendar year. As an alternative to items (3) and (4), Paul suggested that Barbara consider causing Boutique to: (1) sell the land and building for the purchaser's installment obligation, which would have a term of eleven years, have interest only payable during the first ten years, provide that the full amount of principal would be payable at the end of the eleventh year and would be secured by a mortgage on the land and building; (2) continue the S corporation status through the year in which the installment obligation is paid in full, distributing interest and principal payments to Barbara; and (3) revoke the corporation status effective for the year following the year in which the installment obligation is paid in full. Barbara would like your advice on the tax consequences of following Paul's suggestions. Case 28C Issues 1. What would be the amount of "double taxation on the sale of the building and land for $280,000 assuming the after-tax proceeds from that sale are distributed to Ms. Carter as a dividend? 2. What would be the income tax consequences if Ms. Carter implements the four-step plan A? 3. What would be the income tax consequences if Ms. Carter implements the plan B over ten plus years? 4. What alternative plan would you recommend to Ms. Carter