Answered step by step

Verified Expert Solution

Question

1 Approved Answer

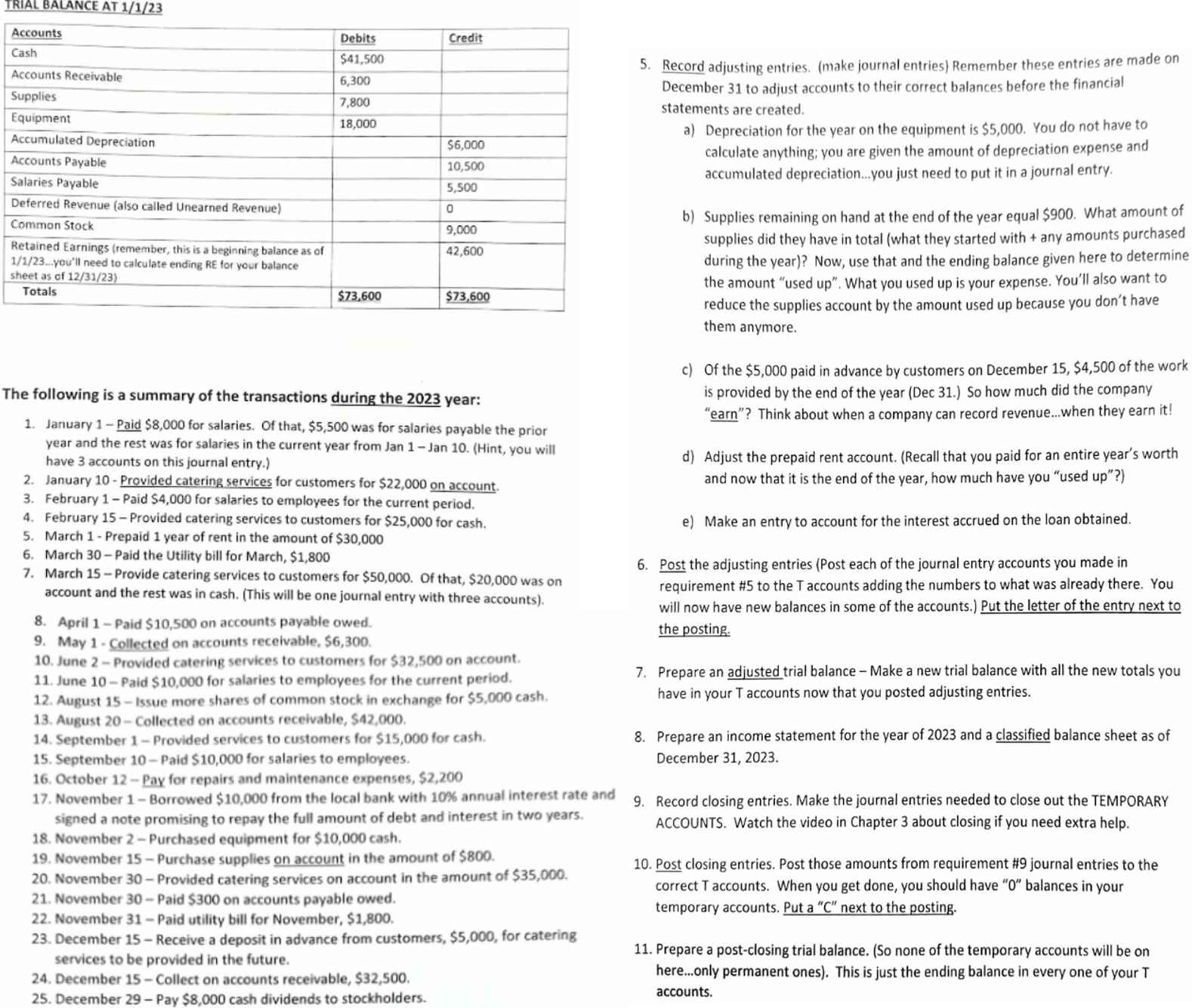

TRIAL BALANCE AT 1 / 1 / 2 3 ( Look at picture for chart ) The following is a summary of the transactions during

TRIAL BALANCE AT

Look at picture for chart

The following is a summary of the transactions during the year:

January Paid $ for salaries. Of that, $ was for salaries payable the prior year and the rest was for salaries in the current year from Jan Jan Hint you will have accounts on this journal entry.

January Provided catering services for customers for $ on account.

February Paid $ for salaries to employees for the current period.

February Provided catering services to customers for $ for cash.

March Prepaid year of rent in the amount of $

March Paid the Utility bill for March, $

March Provide catering services to customers for $ Of that, $ was on account and the rest was in cash. This will be one journal entry with three accounts

April Paid $ on accounts payable owed.

May Collected on accounts receivable, $

June Provided catering services to customers for $ on account.

June Paid $ for salaries to employees for the current period.

August Issue more shares of common stock in exchange for $ cash.

August Collected on accounts receivable, $

September Provided services to customers for $ for cash.

September Paid $ for salaries to employees.

October Pax for repairs and maintenance expenses, $

November Borrowed $ from the local bank with annual interest rate and signed a note promising to repay the full amount of debt and interest in two years.

November Purchased equipment for $ cash.

November Purchase supplies on account in the amount of $

November Provided catering services on account in the amount of $

November Paid $ on accounts payable owed.

November Paid utility bill for November, $

December Receive a deposit in advance from customers, $ for catering

services to be provided in the future.

December Collect on accounts receivable, $

December Pay $ cash dividends to stockholders.

Record adjusting entries make journal entries Remember these entries are made on December to adjust accounts to their correct balances before the financial

statements are created.

a Depreciation for the year on the equipment is $ You do not have to calculate anything; you are given the amount of depreciation expense and accumulated depreciation...you just need to put it in a journal entry.

b Supplies remaining on hand at the end of the year equal $ What amount of supplies did they have in total what they started with any amounts purchased during the year? Now, use that and the ending balance given here to determine the amount "used up What you used up is your expense. You'll also want to reduce the supplies account by the amount used up because you don't have them anymore.

c of the $ paid in advance by customers on December $ of the work is provided by the end of the year Dec So how much did the company "earn"? Think about when a company can record revenue...when they earn it

d Adjust the prepaid rent account. Recall that you paid for an entire year's worth and now that it is the end of the year, how much have you "used up

e Make an entry to account for the interest accrued on the loan obtained.

Post the adjusting entries Post each of the journal entry accounts you made in

requirement # to the T accounts adding the numbers to what was already there. You will now have new balances in some of the accounts. Put the letter of the entry next to the posting

Prepare an adjusted trial balanceMake a new trial balance with all the new totals you have in your T accounts now that you posted adjusting entries.

Prepare an income statement for the year of and a classified balance sheet as of December

Record closing entries. Make the journal entries needed to close out the TEMPORARY ACCOUNTS. Watch the video in Chapter about closing if you need extra help.

Post closing entries. Post those amounts from requirement journal entries to the correct T accounts. When you get done, you should have balances in your temporary accounts. Put a C next to the posting

Prepare a postclosing trial balance. So none of the temporary accounts will be on here...only permanent ones This is just the ending balance in every one of your T accounts.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Michael J. Jones

1st Edition

0470058986, 978-0470058985