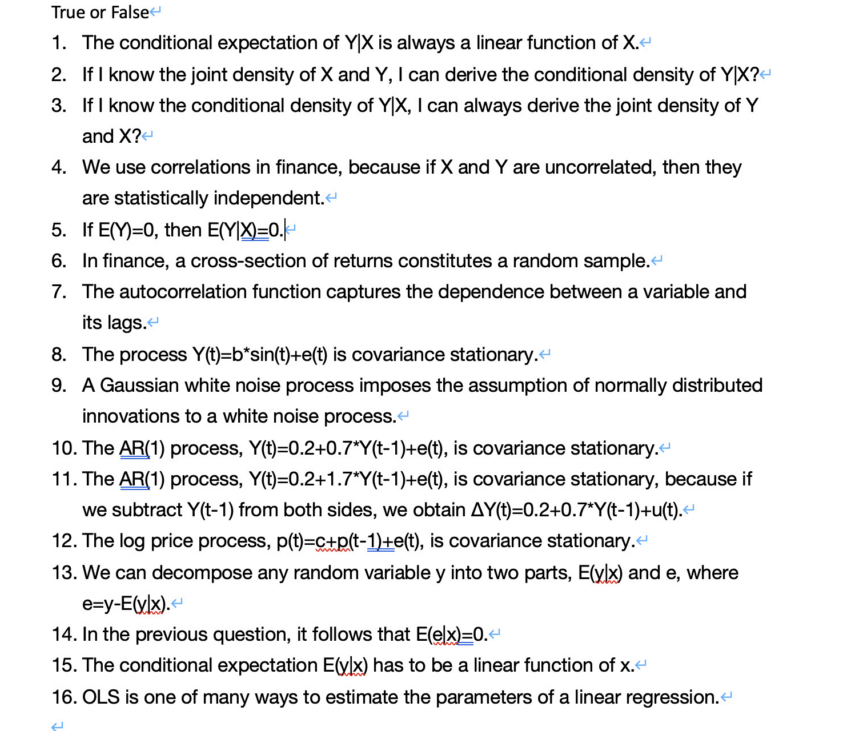

True or False 1. The conditional expectation of Y|X is always a linear function of X. 2. If I know the joint density of X and Y, I can derive the conditional density of YIX?- 3. If I know the conditional density of Y|X, I can always derive the joint density of Y and X?- 4. We use correlations in finance, because if X and Y are uncorrelated, then they are statistically independent. 5. If E(Y)=0, then E(YX)=0.- 6. In finance, a cross-section of returns constitutes a random sample. 7. The autocorrelation function captures the dependence between a variable and its lags. 8. The process Y(t)=b*sin(t)+e(t) is covariance stationary. 9. A Gaussian white noise process imposes the assumption of normally distributed innovations to a white noise process. 10. The AR(1) process, Y(t)=0.2+0.7*Y(t-1)+e(t), is covariance stationary. 11. The AR(1) process, Y(t)=0.2+1.7*Y(t-1)+e(t), is covariance stationary, because if we subtract Y(t-1) from both sides, we obtain AY(t)=0.2+0.7*Y(t-1)+u(t). 12. The log price process, p(t)=c+p(t-1)+e(t), is covariance stationary. 13. We can decompose any random variable y into two parts, E(ylx) and e, where e=y-E(y|x). 14. In the previous question, it follows that E(elx)=0. 15. The conditional expectation Elxlx) has to be a linear function of x. 16. OLS is one of many ways to estimate the parameters of a linear regression. True or False 1. The conditional expectation of Y|X is always a linear function of X. 2. If I know the joint density of X and Y, I can derive the conditional density of YIX?- 3. If I know the conditional density of Y|X, I can always derive the joint density of Y and X?- 4. We use correlations in finance, because if X and Y are uncorrelated, then they are statistically independent. 5. If E(Y)=0, then E(YX)=0.- 6. In finance, a cross-section of returns constitutes a random sample. 7. The autocorrelation function captures the dependence between a variable and its lags. 8. The process Y(t)=b*sin(t)+e(t) is covariance stationary. 9. A Gaussian white noise process imposes the assumption of normally distributed innovations to a white noise process. 10. The AR(1) process, Y(t)=0.2+0.7*Y(t-1)+e(t), is covariance stationary. 11. The AR(1) process, Y(t)=0.2+1.7*Y(t-1)+e(t), is covariance stationary, because if we subtract Y(t-1) from both sides, we obtain AY(t)=0.2+0.7*Y(t-1)+u(t). 12. The log price process, p(t)=c+p(t-1)+e(t), is covariance stationary. 13. We can decompose any random variable y into two parts, E(ylx) and e, where e=y-E(y|x). 14. In the previous question, it follows that E(elx)=0. 15. The conditional expectation Elxlx) has to be a linear function of x. 16. OLS is one of many ways to estimate the parameters of a linear regression